This report is not a personal recommendation and does not take into account your personal circumstances or appetite for risk.

21 September 2015

Oil off 6-year lows: BP & Shell primed for rebound?

[vc_row][vc_column width="1/2"][vc_column_text col_class="style4"]

Is the Oil & Gas business set to enter a new paradigm?

Recent reports about the future of the UK’s North Sea oil & gas fields has raised alarm, compounding already present worries about the industry at large. A low oil price that doesn’t appear too keen to move higher any time soon, lower demand from an apparently slowing China and competition in the form of Shaleand its potential to bring energy self-sufficiency ever closer to the US and UK have conspired to open up a war on multiple fronts.

Stubborn oil producers are now fighting to maintain their share of the global market, but with crude prices where they are the fight will almost certainly fail to produce any winners. There’s little point in things carrying on the way they are and the competitors know it. The question is who will back down first?

One of the reasons we’re in this situation is the sheer bloody mindedness of two of the major oil producers: OPEC and the USA. While OPEC has been pumping record amounts of crude into the market for some time, hoping to squeeze out global rivals, its main competitor – the US – has remained resilient and while OPEC’s so-called ‘fragile five’ will likely continue to produce at current prices, there’s only so far you can go without paying wages before workers start taking action. We’re unlikely to see $100/barrel oil any time soon but the current state of affairs in the Oil and Gas sector cannot continue, and there are two ways in which it could correct.[/vc_column_text][vc_column_text col_class="style2"]

The acrimonious way or the amicable way?

A destructive scenario whereby Saudi Arabia simply allows the fragile five to fail could impact total OPEC output to the tune of up to 30% (the contribution of Saudi Arabia itself), and this would keep prices well above the $30s.[/vc_column_text][/vc_column][vc_column width="1/2"][vc_column_text col_class="style3"]Alternatively, Saudi Arabia stops worrying about market shareand lets prices find their natural equilibrium via supply and demand – less output, less market share, higher prices. Amicable or acrimonious, the oil price should find somebuoyancy, but the amicable way leaves Saudi Arabia with just that little bit more control – which is really what this whole thing is about.

North Sea Exodus

Industry body UK Oil & Gas said in a recent report that capital investment in North Sea exploration and production couldhalve in the next two years. We think this could be just the tip of the iceberg – already we’re seeing oil majors exiting, unwilling to put up with higher costs, and this is leaving fewer, smallercompanies to shoulder the burden. It’s only a matter of time before the rest give up too and the effect of that on UK supply is clear. If it’s not completely clear, know that the UK derives over a third of its energy from North Sea oil.[/vc_column_text][vc_column_text col_class="style5"]

How have the UK’s Oilers been doing amid all this?

They’ve been under pressure - as expected in the current circumstances. It’s the smaller E&P stocks that have, perhaps unsurprisingly, suffered the most while the oil equipment and services subsector has outperformed with plenty of oil being pumped up, transported and refined the world over. Integrated oil & gas majors sit in between, tugged one way by E&P and the other by downstream activities, yet their dividend yields make them potentially attractive investments. Note Cairn Energy (CNE)outperforming its subsector while Hunting (HTG) is underperforming its own.[/vc_column_text][/vc_column][/vc_row]

[vc_row][vc_column width="1/2"][vc_column_text col_class="style1"]But has oil got further to fall? Unlikely in our view. Is it set for any kind of recovery? Perhaps not to where it was in the summer of 2014, but even if US Light Crude does sink into the $30s we’d expect that to be a brief move while the outlook for Brent Crude, given the depletion of and increasing extraction costs in theNorth Sea fields, could keep its price well above $40.[/vc_column_text][vc_column_text col_class="style2"]

Facts

The oil majors are still reporting billions in profits, despite the price of crude oil being down by almost 60%. Since helping the UK 100 to all-time highs in April they have announced major restructuring programmes to cut costs. If they are still making profits in these supposed ‘bad’ times, how might they fare withlower costs when the oil price recovers? Surely things can only get better from here. The important question is: how long will it take?

Income seekers are surely going to be eyeing many of these shares at current, heavily discounted levels. Buying pressure drives prices higher, while we’ve seen oil prices move by 5% or more on many occasions, each time causing Oil & Gas stocks to move considerably. While we wouldn’t expect any of the UK Index oil companies to regain their boom-time highs in the current conditions, there’s still plenty of scope for 5%, 10%, even 15% upside. A conservative outlook of 5% capital gains plus 7% income yield makes for a potentially pretty good return for a year’s investment.[/vc_column_text][vc_column_text col_class="style3"]

Capital gains or income?

Many investors look solely for capital gains – buying a stock expecting the price to rise with a view to selling at a profit. However the longer term investor may also look for a good dividend yieldthat can both offset losses if the share price falls and even bring a profit if the share price remains flat. While a full recovery in the oil price might see the biggest fallers in this class regain prior highs, the more likely scenario is that the oil price moves in a range between $40 and $50 for the foreseeable future, as markets plough their way through burgeoning global stockpiles. The investor can therefore make an informed decision based on his / her appetite for risk.[/vc_column_text][/vc_column][vc_column width="1/2"][vc_column_text]

UK 100 Integrated Oil & Gas

BP (BP)

Price change since April UK Index highs: -36%[/vc_column_text][vc_column_text col_class="style7"]

BP. closing prices, weekly

[/vc_column_text][vc_column_text col_class="style1"]Will the price bounce up towards 400p or will it fall beneath lows of 300p?

Projected dividend yield: 7.7% (14 Sept)

Broker Consensus: 30% Buy, 53% Hold, 18% Sell

Most Bullish: Barclays, overweight, Target 600p, +78% (21 Aug)

Consensus: Target 420p, +24% (14 Sept)

Most Bearish: Day by Day, sell, TP 297p, -12% (7 Sept)

NB: All pricing and consensus data from Bloomberg on 14 Sept; Consensus breakdown available on request [/vc_column_text][/vc_column][/vc_row]

[vc_row][vc_column width="1/2"][vc_column_text col_class="style1"]

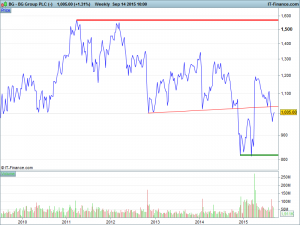

BG Group (BG.)

Price change since April UK Index highs: -14%[/vc_column_text][vc_column_text col_class="style7"]

BG. closing prices, weekly

[/vc_column_text][vc_column_text col_class="style2"]Will the price rally towards 1500p or will it fall towards lows of800p?

[/vc_column_text][vc_column_text col_class="style2"]Will the price rally towards 1500p or will it fall towards lows of800p?

Projected dividend yield: 1.9% (14 Sept)

Broker Consensus: 55% Buy, 35% Hold, 10% Sell

Most Bullish: Tudor Pickering & Co., buy, Target 1500p, +50%

Consensus: Target 1218p, +22%

Most Bearish: Day by Day, sell, Target 776p, -23%

NB: All pricing and consensus data from Bloomberg on 16 Sept; Consensus breakdown available on request [/vc_column_text][/vc_column][vc_column width="1/2"][vc_column_text col_class="style1"]

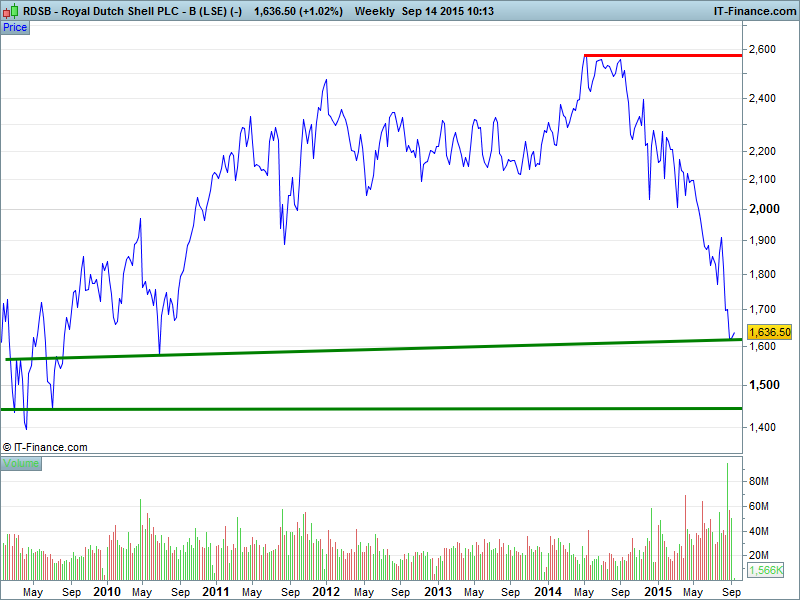

Royal Dutch Shell (RDSb)

Price change since April UK Index highs: -22%[/vc_column_text][vc_column_text col_class="style7"]

RDSb closing prices, weekly

[/vc_column_text][vc_column_text col_class="style3"]Will the price rally towards 2600p or will it fall towards lows of1400p?

[/vc_column_text][vc_column_text col_class="style3"]Will the price rally towards 2600p or will it fall towards lows of1400p?

Projected dividend yield: 7.5% (14 Sept)

Broker Consensus: 56% Buy, 33% Hold, 11% Sell

Most Bullish: Barclays, overweight, Target 2850p, +75%

Consensus: Target 2152p, +32%

Most Bearish: Natixis, neutral, Target 1690p, +4%

NB: All pricing and consensus data from Bloomberg on 14 Sept; Consensus breakdown available on request

[/vc_column_text][/vc_column][/vc_row]

This research is produced by Accendo Markets Limited.

Research produced and disseminated by Accendo Markets is classified as non-independent research,

and is therefore a marketing communication. This investment research has not been prepared in accordance

with legal requirements designed to promote its independence and it is not subject to the prohibition on

dealing ahead of the dissemination of investment research. This research does not constitute a personal

recommendation or offer to enter into a transaction or an investment, and is produced and distributed for information purposes only.

Accendo Markets considers opinions and information contained within the research to be valid when published,

and gives no warranty as to the investments referred to in this material. The income from the investments referred to may go down as well as up,

and investors may realise losses on investments. The past performance of a particular investment is not necessarily a guide to its future performance.

Prepared by Michael van Dulken, Head of Research