Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

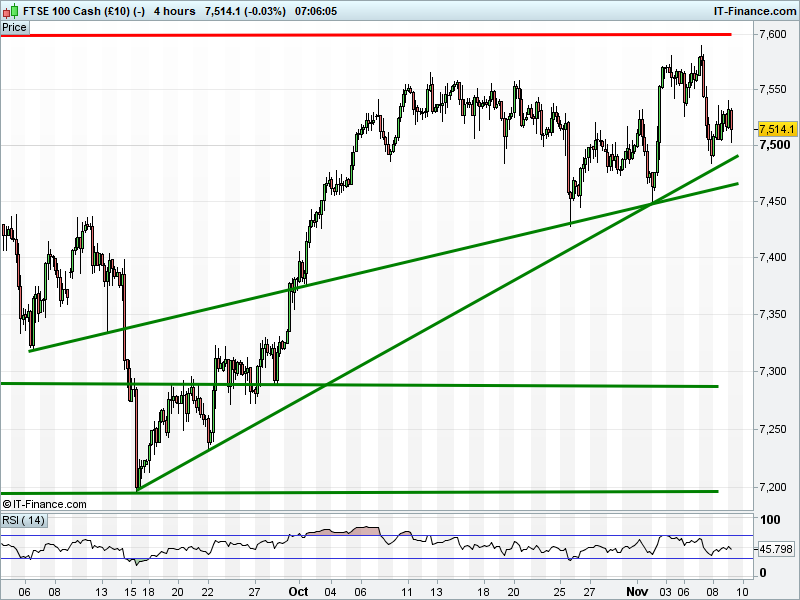

UK 100 Index called to open -15pts at 7510, back from overnight highs of 7540, suggesting continued appetite for upside tests, but holding above 7500 to maintain November’s trend of rising lows. Bulls need a break above 7520; bears a breach of 7500 rising support. Watch levels: Bullish 7520, Bearish 7500.

Calls for a negative start come in spite of an up day on Wall St (yes, with more records), and a largely positive session in Asian overnight where Japanese equities hit fresh 26 yr highs before closing lower. Note Brexit talks resume today while Trump continues an otherwise uneventful Asia trip, no more aggressive than usual.

Macro data overnight included more good news from China with consumer inflation accelerating and Producer Price inflation holding up. This, and a firm oil price, has helped UK Index Miners higher in Australia overnight, although metals prices are weaker. Closer to home, weaker than expected UK RICS House Price balance may weigh further on the UK Index housebuilders.

In Corporate news this morning: Sainsbury H1 results (underlying) look in-line with expectations, guidance maintained, cuts dividend. AstraZeneca Q3 revenues and core EPS beat, along with most drugs; upgrades profits guidance. Hikma continues to expect revenue and core operating profit broadly in line with 2016 due to FX impact; outstanding issues remain with generic advair.

Burberry aims to deliver high-single digit revenue growth and meaningful operating margin expansion, strong cash generation, progressive dividend policy and additional distributions. National Grid outlook unchanged, expects stronger H2. Informa & Rolls Royce both sees trading in-line with guidance. Inmarsat continues to invest in core capabilities, at expense of lower EBITDA margins; markets remain challenging and outlook difficult to predict.

All three major US indices posted fresh record closing highs on Wednesday, despite the continued underperformance from the Financial sector as the Republican tax reform faces further hurdles, with Consumer Staples leading markets higher. The Tech-focused Nasdaq returned to its recent run of outperformance, while the Dow Jones closed just above breakeven as Merck and Wal-mart led risers.

Crude Oil benchmarks have traded sideways overnight as traders digest a surprise build in US oil inventories whilst also assessing the potential for an extension to OPEC-led production cuts. A weaker US dollar overnight has helped both Brent and US indices to remain in touching distance of recent 2-year highs of $64.5 and $58, respectively.

Gold continues to test resistance at $1284 after the weaker US dollar (possible US tax reform delays) and rising geopolitical tensions (Saudi, Trump in Asia) overnight buoy demand. The Precious metal, having made a bullish test of the resistance level yesterday afternoon to trade as high as $1287, is back at the key resistance level. The greenback will remain a key driver of sentiment today after the US market open.

Another quiet day for macro data will see traders eyes focused on the sixth round of UK-EU Brexit negotiations in Brussels. The European side have called on the UK to offer a firm financial offer to pay outstanding obligations in order to put in place the framework for a transitional agreement before year end, however this is significantly ahead of the British timetable before even reaching the contentious issue that is the exit bill.

Concessions will need to be made on both sides; the UK to accelerate its process of determining a leaving price while inevitably the EU side may have to accept a figure lower than previously expected. It’s down to you, Messrs Davis and Barnier.

Aside from Brexit negotiations, a multitude of ECB speakers are scheduled to speak today. At 10am, Coeure delivers his ‘vision for Europe’ in Lyon, Mersch (1:15pm) discusses ‘turbulent times for European finance’, Constancio (1:45pm) is the keynote speaker at the Financial Regulatory Outlook conference in Rome, while renowned German hawk Weidmann speaks in Leipzig (6pm) before Lautenschlaeger (6:20pm) rounds things off in Washington at a joint IMF, BOE and HK Monetary Authority conference.

The only data releases of note today are US Weekly Jobless Claims (1:30pm), seen increasing marginally, and US Wholesale Inventories (3pm) seen confirmed unchanged at 0.3% in September.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.