Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

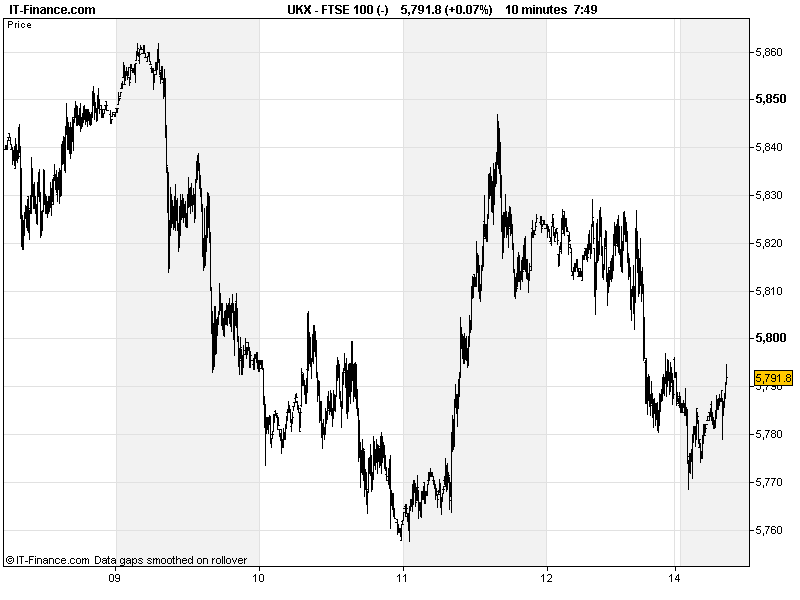

UK 100 called to open -5pts, despite a better than expected Chinese Trade Surplus print, in contrast to a forecast narrowing, thanks to a surprise boost in exports which flies in the face of china/Asia/global growth slowing worries.

Weakness this morning may, however, be explained by Chinese Consumer Inflation in-line, slowing from the prior month, and a worsening in Chinese Producer prices (so, those exports being sold for less - pricing pressure), although as we alluded to last week, such data could lead to assumptions policy makers will be pushed to intervene with more measures to boost the economy.

There is also the on-going uncertainty over the Eurozone (another summit this week) and potential worries that China’s Q3 GDP data disappoints on Thursday, along with Q3 earnings from failing to provide enough optimism to maintain the 3-4 month equity uptrend. JPMorgan and Wells Fargo may have done the usual consensus-beating charade, but the detail failing to inspire (buy on rumour, sell on fact?).

Other overnight data contributing to the downbeat start to the weak include the worsening in Japanese Industrial Production and Capacity Use, although a big improvement in UK House Prices and Aussie Motor Vehicle Sales offer a modicum of support, after the equity losses of the prior week on slowing global growth concerns.

US markets closed slightly lower, reversing course from gains following the consensus beating Uni of Michigan Consumer Confidence figure, with the Eurozone and more specifically the viability of the European Stability Mechanism (ESM) in terms of cash sufficiency for Spanish bailout request. Although this was countered to some extent by talk of a possible Greek bond buyback/debt extension.

The US Q3 earnings season steps up a gear today with JPMorgan and Wells Fargo providing the first updates for the all-important financial sector. This could provide a knock-on to the European banks which have already rallied strongly on the ECB and Fed pledge/intervention.

In FX and Commodities, GBP/USD and EUR/USD pulled back on risk aversion, with the stronger US dollar taking the price of Gold down another leg. GBP/EUR still in uptrend from Friday lows. In the Oil arena, the stronger dollar has ushered the price of US Crude back from Friday and last week’s highs. Brent Crude looks similar, although technically still in a uptrend fuelled by geopolitical worry drivers.

This week’s focus will remain on earnings season and most certainly the banks, with big names Citigroup (today), Goldman Sachs and State Street (tomorrow), Bank of America, Merrill Lynch and BNY Mellon (Wednesday).

In terms of macro data, today’s US Retail Sales likely of interest with growth seen slowing, along with Business Inventories (although wholesale inventories rose last week). Other data to watch for: German ZEW surveys, UK inflation, US industrial Production (Tues), UK Jobless, US Housing (Weds), UK Retail Sales and US Jobless (Thurs).

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Trade Balance Better

- China Exports Better

- China Imports In-line

- UK Rightmove House Prices Improved

- Aussie New Motor Vehicle Sales Improved

- Aussie Home Loans Better

- Aussie Investment Lending Another decline

- China Consumer Price Index In-line

- China Producer Price Index Worse

- Japan Industrial Production Continued decline

- Japan Capacity Utilisation Declined

- See Live Macro calendar for all details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Filtrona says third quarter performance in line with co's expectations

- RBS under pressure after collapse of branch sale

- Galliford Try secures 89 mln stg leisure contract

- Tullow Oil acquires stake in Maersk's Greenland licence

- International Ferro says ferrochrome output unaffected by lower UG2 supply

- SDL says language services keep Q3 broadly in line

- Great Portland sells Bishopsgate stake for 47 mln stg

- Fresnillo says on track to meet annual targets

- Aveva says makes good first-half progress

- Talvivaara says may not reach nickel production target

- McBride sees profit hit from contract manufacturing wind-down