Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

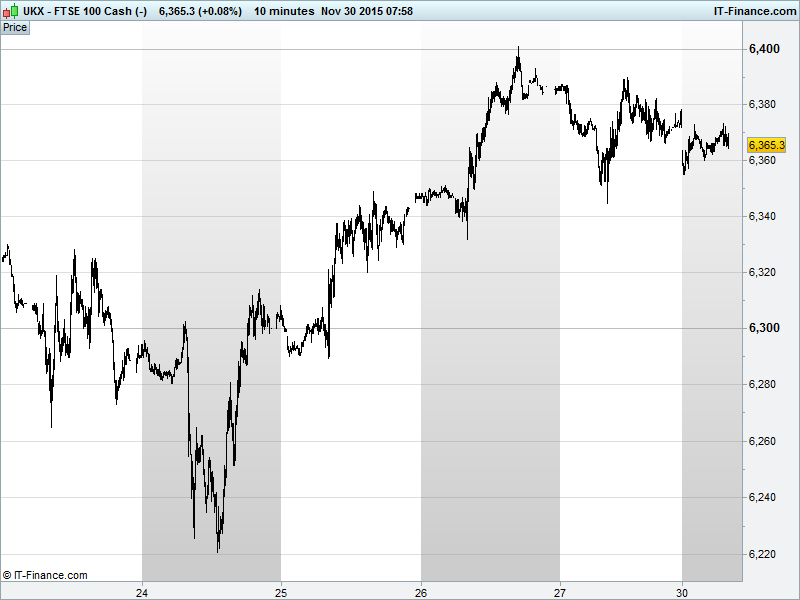

UK 100 Index called to open -10pts at 6365, close to the apex of a narrowing pattern which, as a continuation pattern, could result in a break-out to the upside, supported by us remaining above the 100-day MA. However, the narrowing pattern’s sequence of falling highs since Thursday’s brief revisit of 6400 maintains the 6-month trend of falling resistance which represents a significant hurdle to overcome in the short-term. Turning over again? Watch levels: Bullish 6380, Bearish 6350.

The negative opening call comes after a mixed session in Asia with Chinese equities ironically the outperformers after recovering from an sharp intra-day sell-off, the biggest in 3 months, extending Friday’s weakness as brokerages plunge on regulatory probes. Recovery, however, likely aided by expectations of yuan inclusion in the IMF basket this afternoon as well as hopes of further monetary stimulus.

The China recovery has, however, failed to help regional peers with Japan’s Nikkei still in the red with insurers, shipping and drug-makers leading the retreat, while Australia’s ASX is hindered by China and renewed weakness in the raw materials space as global growth and supply glut concerns see Copper retrace its recent rally, Gold make fresh almost 6yr lows and Iron Ore drops below $40

Geopolitics still lurking, along with Climate concerns, however, all eyes on the first instalment of central bank updates this week from the ECB which is seen delivering more easy policy, before the US jobs report on Friday tees us up for a potential Fed rate hike mid-month, thus crystallizing the first step in terms of a rate hike and major policy divergence.

In corporate world, AB Inbev (BUD)’s $100bn takeover of SABMiller (SAB) means it is considering the sale of the latter’s Peroni and Grolsch brands to help ensure regulatory clearance for what would be a monster tie-up within the beverages sector .

US markets closed mixed on Friday with light volume and a half-day’s trading having a muting effect. This week likely to see clear signs of an imminent Fed rate hike, while a lack thereof could signal yet another delay with economic activity and inflationary pressures still seen by many as too low to warrant one.

In focus today, we have UK Mortgage Approvals data seen showing continued strength in the UK property market, while an update in the Lloyds Barometer will provide an update on Business sentiment. German Consumer inflation is sure to remain close enough to breakeven to maintain calls for an expectations of more stimulus from the ECB this week. In the afternoon, while the Chicago PMI may give up some of its strength, US Pending Home Sales are seen rebounding, but Dallas Fed Manufacturing Activity is likely to remain depressed.

Saudi Arabia is due to be challenged by fellow OPEC members at this week’s meeting on its high production, market share protecting policy which is now seen by some of its OPEC allies as having been a failure. They will argue that it’s time to change tack in the face of the resilience of non-OPEC competition, while Saudi Arabia is unlikely to take their advice. Oil prices therefore likely to be under continued pressure going forward.

Gold is back around 6-year lows after its steepest monthly declines in 2.5 years as markets continue to price in a Fed rate hike and the US Dollar basket remains at record high levels.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Aberdeen Asset Mgt FY assets hit by emerging market outflows

- Clinigen starts managed access program for Ixazomib

- Playtech signs 5yr Sun bingo deal

- Ladbrokes notes merger target Coral's core earnings rise 1%

- IG Group Holdings Has Performed Well; 2Q Revenue Above 1Q