Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

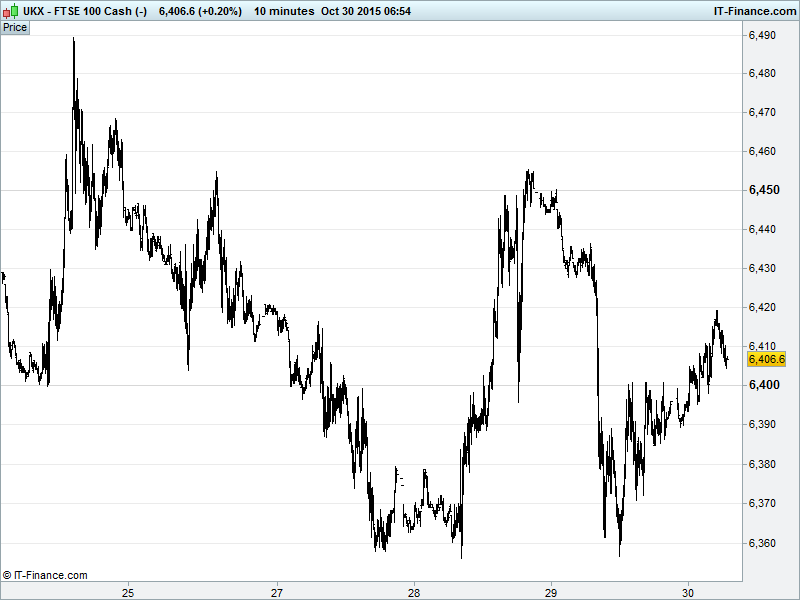

UK 100 Index called to open +10pts at 6405, still in an October uptrend but with falling highs since last Friday. This results in a narrowing pattern which keeps the index within the confines of a 4-week bearish rising wedge and could result in a reversal of the uptrend from end-September lows. Updated watch levels: Bullish 6440, Bearish 6370.

The positive open comes despite the Bank of Japan refraining from expanding stimulus despite overseas headwinds and stagnant inflation. Governor Kuroda has faith in modest economic progress having enough momentum to hit targets and thankfully left the door open for further easing.

The positive market response suggests markets happy with the status quo and especially the option for more QE later as well as the BoJ's confidence in a growth turnaround. Not dissimilar to the hawkish Fed statement mid-week seeing the positive outlook on growth outweighing the prospect of higher rates on the horizon. Markets still like cheap money, but may be coming round to a return to preference for actual growth.

After a weak European and US close, Asian stocks are mixed with Japan’s Nikkei the outperformer after the BoJ stayed pat on policy and the JPY pared its weekly rise versus peers. Australia’s ASX is the underperformer as commodities prices dropped. China flat despite yesterday’s end to the one-child policy which is sure to benefit consumer stocks, and possibly guarantee solid iPhone sales for generations.

Wall Street indices tracked lower yesterday as fickle investors continued to digest hawkish tones regarding a 2015 rate hike. At the same time US data came in mixed as usual, certainly not indicative of the kind of economic health the Fed is looking for. Interesting and perhaps refreshing that the BoJ overnight decided against further policy easing for now. Is it looking at things from a different angle? Have its peers' action done its work for it?

Corporates-wise, BG Group (BG.) compounded a murky few days for energy stocks with its posting of a sharp drop in Q3 earnings. For those who’ve been asleep for the past 15 months, that’s because of what’s commonly seen as low oil prices.

Int. Consolidated Airlines Group (IAG), on the other hand, looks to have benefitted handsomely from cheap fuel and higher customer demand with the conglomerate very kindly deciding to start paying dividends for the first time. Cheers IAG, you’re the best! Airline stocks to fly away for the weekend?

RBS continued the UK banking trend by posting decent Q3 financials (nearly £1bn in profits compared to forecasts of a £180mn loss), while setting aside nearly £1bn to pay for the several tubes of E45 cream it’ll need to soothe those heavily slapped wrists and as such returning the bank to break-even for the quarter.

Lastly, just before the European close yesterday (convenient) it was announced that Standard Chartered (STAN) has held talks with bankers on raising at least $4bn as UK regulators tighten scrutiny on lenders with exposure to emerging markets in a second round of stress tests. Not a great week for the European banks in general.

In focus today, on the last session of the week and month, we have Eurozone Consumer Price Inflation seen still flat suggestive of more ECB help being needed. In the afternoon, after yesterday’s lower GDP print, we have US personal Income and Spending seen steady, but inflation pressures still prevalent while Consumer Sentiment is likely unchanged.

‘Love it or hate it’ crude oil is sitting smack bang in the middle of its $40-$50 sideways trading range, pleasing consumers while hammering producers as highlighted above. Still plenty of scope for swing trades on US Light and Brent Crude with neither seeming keen on breaking out either way.

It’ll be interesting to see whether Gold can remain in a rising channel started back in August. The yellow metal is currently in correction mode with potential support at $1144, though a break below this would put us on the lookout for a bounce off $1126 or thereabouts to continue the 3-month trend.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- RBS announces profits of £1bn but warns conduct charges may be higher

- BG raises FY production guidance to 680 – 700 kboed

- IAG Q3 profit beats forecasts, upgrades 2015 guidance

- Elementis says expects FY EPS in line with market expectations

- Pets at Home says FY outlook broadly in line with market expectation

- Moneysupermarket.com says confident of meeting FY expectations

- Lookers sees FY results in line with market expectations

- Standard Chartered said to weigh $4bn capital rising