Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

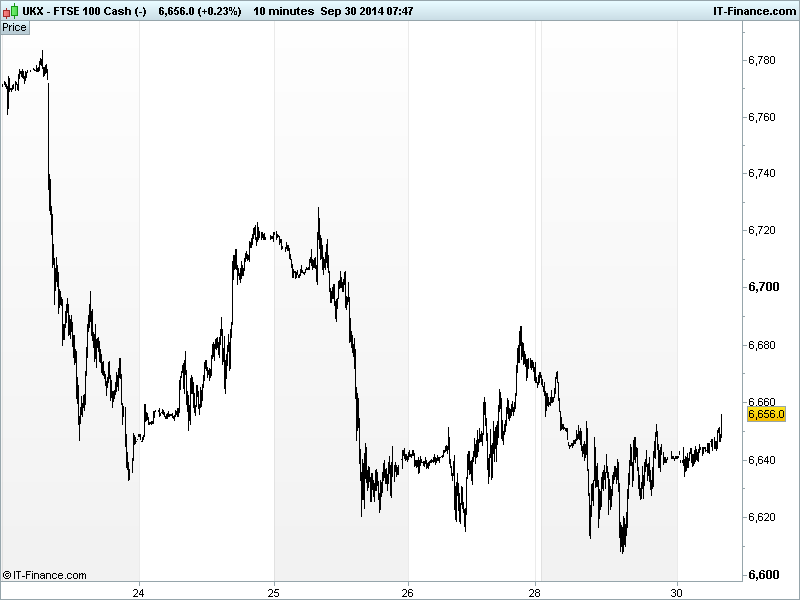

UK 100 called to open +5pts at 6655, extending the run of tepid opening calls, as traders remain cautious ahead of Friday’s US employment data and after China HSBC PMI Manufacturing missed estimates overnight reigniting fears of a slowing #2 economy and tensions remain in Hong Kong.

While US markets closed lower on poor Pending Home Sales data following decent Income and Spending prints bourses in Asia have maintained the negative Wall Street lead after the overnight China data with Hong Kong understandably under most pressure even if some UK-listed banks have announced reopening of certain branches. Australia normally hurt by bad China data is benefiting from a strong USD and weaker AUD and some bargaining hunting.

The HSBC China Manufacturing PMI fell to 50.2 which was worse than the flash reading of 50.5 in September, which was flat versus August, as the property slump weighs. Other major data overnight included a deterioration in the UK GFK Consumer Confidence (it went negative) while Japanese Retail trade, Unemployment and Housing starts improved but Industrial production worsened.

This morning we have seen slowing in the UK Nationwide House Price Index which will give rise to calls of a slowing market, a welcome development for BOE policy makers and potential home buyers but may be explained by the Scottish referendum timing and after a traditionally slower summer. German Retail Sales were strong in August.

In focus today we have a busy schedule with German unemployment seen broadly unchanged in September. UK Q2 GDP growth is expected to be confirmed, however, anything better could help with a relief rally.

Eurozone Unemployment will be looked to for any signs of improvement giving hope or deterioration putting more pressure on the ECB to act more decisively to help the region, something that Eurozone Consumer Price inflation could also do given the forecast for a fall in September adding to the fears of deflation.

In the afternoon, US S&P Case-Shiller House Prices are expected to have remained weak in July while the US Chicago PMI gives up a little ground (albeit from a strong level in August) but could be offset by a September improvement in US Consumer Confidence.

The UK 100 index remains in a downtrend from 19 September highs of 6900 and under pressure at 6650 having displayed difficulty in getting above the level again overnight. We continue to highlight the bearish possibility of more downside given the increase in concerns (growth, geopolitics, military action) over the last week. Bulls, however, will be hoping that the lack of progress from 6600-6650 will have given time for concerns to be baked in and the foundations set for a recovery rally.

In commodities, Gold has settled in a tight $1215-1220 range near 9-month lows as traders and investors alike continue to factor in the tricky mix of potentially higher US borrowing costs as the economy improves and a stronger USD makes the safehaven more expensive along with military action and expanding geopolitical concerns round the world.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK GFK Consumer Confidence Miss, deteriorated

- JP Retail Trade Beat, improved

- JP Industrial Production Miss, deteriorated

- CN HSBC Manufacturing PMI Miss, deteriorated

- JP Housing Beat, less weak

- UK Nationwide House Prices Miss, weaker

- DE Retail Sales Mixed

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Euromoney Institutional expects FY underlying revenue to rise 3 pct

- Saga like-for-like profit rises 14.9 pct

- KCom says first-half trading in line with expectations

- Next says profit will be hit if warm weather continues

- TalkTalk's Makin to step down as CFO in November

- AO World says trading in line, to open German website

- RBS says now expects to significantly outperform its previous guidance of £1 billion in total impairments

- Meggitt completes five-year bank refinancing

- Soco International starts returning cash to shareholders

- RBS says releases 800 mln pounds from provision pot

- Britain's Intertek hires new CEO from Inchcape

- Qinetiq Group says on track to meet annual guidance

- Amerisur Resources H1 pretax profit rises

- BSkyB invests in U.S. advert technology firm Sharethrough

- Bovis Homes says CFO Jonathan Hill to leave and join Saga

- Wolseley annual profit rises, raises dividend

- Sirius Minerals provides update on York Potash project approval process

- Interdealer broker ICAP says first-half revenue to fall 10 pct