Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

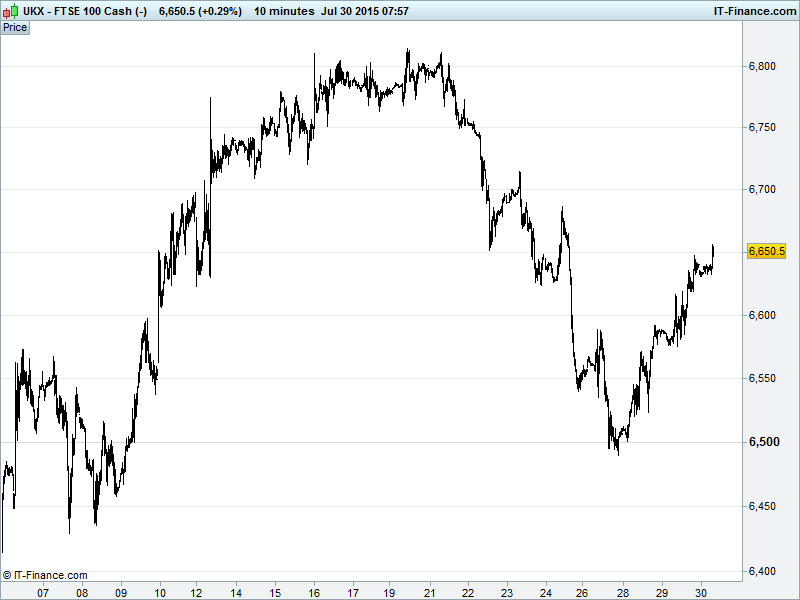

UK 100 Index called to open +20pts at 6650 with the rebound from 6500 lows having broken above 1-week falling highs and retraced 50% of the declines from 6815 early last week. Trendline of rising lows offers support around 6630 while test of 6650 as we write bodes well for recovery towards 6815 July highs. Updated watch levels: Bullish 6660, Bearish 6625.

The positive opening call comes as Asian stocks follow their US counterparts higher - extending their bounce - after the US Federal Reserve said it was closer to a rate hike this year thanks to an improving labour market, keeping the door open for a September hike even if inflation remains sub-target and additional data points or external factors (Greece, China) could see it hold off until year-end.

A bounce by oil on higher US inventories and potential Saudi production cuts is also helping along with a stronger USD Index (set for biggest monthly gain since March) following the Fed update and better than expected earnings reports (Facebook, Hitachi, NTT Docomo), although Samsung did miss forecasts on disappointing Galaxy sales.

US stocks closed higher for a second day helped by the positive economic assessment by the Fed, the bounce in the oil price and on the whole decent earnings reports.

Japan’s Nikkei higher thanks to weaker JPY and industrial production data beating expectations. Australia’s ASX higher, led by miners and commodity price strength and despite Building Approvals plunging, with the data cooling fears of an overheated property market. Note Chinese bourses mixed as intervention continues to prop up a burst equity bubble.

While things might seem quiet on the Greek front, with final bailout negotiations only just getting started, note PM Tsipras facing new challenges from Syriza hardliners over the third bailout which could see him lose parliamentary majority although he vows not to be blackmailed. A tech glitch has also resulted in the Athens stock exchange remaining closed through next week.

In focus today – German Unemployment at 8.55am Eurozone Confidence and Business Climate indicators at 10am, German Consumer Price Inflation at 1pm and then US jobless claims and GDP updates at 1.30pm. Results from a plethora of US corporates including Amgen (AMGN), Colgate Palmolive (COL), Fiat-Chrysler (FCAU), P&G (PG) and Marriot International.

Oil saw renewed strength yesterday which could trim is biggest monthly loss this year following an unexpected drawdown in US stockpiles and reports that Saudi Arabic will reduce production which gave renewed hope of a rebalancing of the global supply/demand dynamic. Note US Light Crude broke >$48 to test $49.5 while Brent broke >$53.7 to test $54.5.

Gold looks set for its worst month since 2013 with the Fed outlook and resulting stronger USD (albeit with a 12hr delay) seeing it fall back to test $1085 having been sideways around $1095 for 3 days. Are we headed back to recent 5.5yr lows of $1077? Safehaven far from safe?

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- RBS reports modest rise in Q2 profit after restructuring charge

- Lloyds sells 2.6 bln stg of Irish loans to Goldman, CarVal, BoI group

- BT on track for full year due to broadband, pay – TV demand

- Henderson H1 underlying profit rises 29 pct, plans share buyback

- Schroders H1 pretax profit up 24 pct to 290.3 mln

- Weir Group's first half profit falls 40 pct hurt by slump in oil

- Rolls – Royce first – half profit slumps, guidance unchanged

- BAE Systems says on track to meet guidance if it secures new orders

- Centrica to sell some upstream, wind assets to shift focus on supply, services

- Xchanging CEO Lever to retire at end of 2015

- Moneysupermarket.com nudges up expectations after strong H1

- Shell Q2 CCS earnings $3.4 bln

- Inchcape posts 6 pct rise in first half profit

- Bodycote H1 operating profit 32.1 mln stg vs 54.2 mln stg

- Smith & Nephew says on track after 6 pct rise in H1 trading profit

- Kaz Minerals on track to hit copper target output, cuts forecast for gold

- Merlin Entertainments posts flat first half profit

- Thomas Cook says Tunisia attack, Greece concern to hit year profit

- AstraZeneca beats profit forecasts, helped by external deals

- Laird's H1 statutory pretax profit up 35 pct

- Amec Foster Wheeler wins clean air technology contract in Mexico

- Rentokil on track to deliver full-year expectations

- Babcock sees slowdown in defence revenue