Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

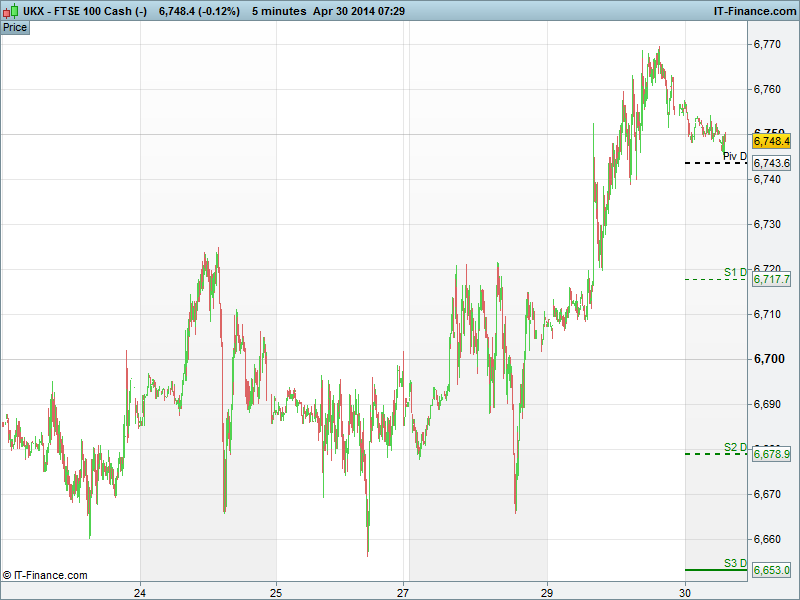

The UK 100 is set to open down by 4pts at 6750pts after a solid 1% or 70pts yesterday saw the index top its highest level in seven weeks.

Contributors to yesterdays' rally included BP (BP.L) up 2.90% at 502.6p, after reporting Q1 profits had come in slightly ahead of forecasts and announced an 8.3% increase to the dividend to 9.75 cents. Banking stocks did their bit to help push the UK Index higher. Royal Bank of Scotland (RBS.L) recorded the most notable gain of the sector up 1.93% at 301.2p, followed by HSBC (HSBA.L) up 1.70%, Lloyds Banking Group (LLOY.L) positive by 1.20% and Barclays (BARC.L) up 0.5%.

Do not forget LLOY reports Q1 earnings tomorrow and RBS on Friday.

Deutsche Bank (DBK.G) the driver behind the banking advance as Europe's largest investment bank beat profit estimates on improved trading revenue. Shares closed 2.18% higher. Fresnillo (FRES.L) finished the session down 1.74%, the price of gold fell as tensions appeared to ease in Ukraine. The biggest turnaround was witnessed in the share price of Shire (SHP.L) closing down 0.70% having been positive by 6.30% earlier in the session on talk US peer Allergan Inc would become the latest US company to swoop for a UK counterpart following the Pfizer/AstraZeneca talks. Allergan Inc later revealed it was also exploring other options.

US Markets registered gains of 0.5% or more on stronger earnings and a recovery in internet shares. Yahoo! Inc (YHOO) and TripAdvisor Inc (TRIP) recorded gains of some 5% whilst earnings from Merck & Co (MRK) and Sprint Corp (S) saw respective share price gains of 3.60% and 11%. After the bell Twitter (TWTR) and eBay (EBAY) delivered their latest trading statements. Twitter failed to register the monthly user numbers the market had expected (255m vs 257m) and was punished in after-hours trading to the tune of 10.4%. eBay, whilst beating Q1 earnings, fell 4.10% in after-market trading, the gloss wiped from its earnings with a lacklustre outlook.

The Dow Jones closed 86pts or 0.53% higher at 16,535pts. The NASDAQ recorded the strongest advance in US indices up 0.72% thanks to the advance in internet/tech stocks.

Asian markets experienced shallow gains or losses in a mixed trading session. The big non-event came with the latest Bank of Japan statement. The current stimulus strategy is to be maintained, some optimists were hoping for an expansion to the current plan.

Results today: British American Tobacco (BATS.L) Q1 revenue +2% at constant FX, cigarette volume from units down 1%, on track for another good year, says emerging markets volumes are increasing. Next (NXT.L) Q1 sales rose 10.8% (8.6% expected) raises full year guidance, FY sales rising to 9.5%, pretax profit £750-790m, raises share buyback limit to £64, says Q1 showed above average sales growth. Standard Life (SL.L) Assets under management (AUM) £247.8bn, Q1 fee revenue £374m, Q1 net inflows £2.4bn. Home Retail Group (HOME.L) Pretax profit £71.2m, full year dividend up 10% to 3.3p, assumes a subdued consumer environment. But sees signs of economic conditions improving. Royal Dutch Shell (RDSA.L & RDSB.L) Profit falls 3% to $7.3bn ($7.5bn last year) on lower oil and gas production of 3.25m boe/d. Ladbrokes (LAD.L) Q1 group profit £18.4m down from £37.4m last year. Sees increasing competition in the run up to the world cup.

In commodities, gold continued to trade lower for the third consecutive day, still below the $1300 handle on speculation that the Fed will reduce monetary stimulus during their two day policy meeting that ends today. Despite a lacklustre month so far, up 0.9% in April, the safe haven commodity has rallied 7.8% since the start of the year, as tensions in Ukraine continue. Silver followed suit, trading lower again and heading for a second monthly loss. With a raft of economic data due today including US ADP, and Chicago PMI, this will cause volatility in the metals. WTI meanwhile was trading at $100.35, heading for a second monthly decline amid speculation that crude inventories are at a 83-year high.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- NZ Business Confidence IN-LINE

- Aussie Private Sector Credit IN-LINE

- Japan Labor Cash Earnings BETTER

- Japan Annualized Housing Starts (MAR) BETTER

- Japan Annualized Housing Starts (YoY) WORSE

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- International Personal Finance Q1 pretax profit 12.7 mln stg

- Tullow Oil sells stakes in two UK gas fields to Faroe Petroleum

- Ultra Electronics says full year expectations remain unchanged

- Ladbrokes Q1 operating profit tumbles

- Heritage Oil reports rise in full-year profits after tax

- DS Smith says group performance been in line

- Unite Group says 73 pct of rooms reserved for 2014/2015 school year

- Shell earnings fall on refineries impairments

- Greggs Q1 like-for-like sales up 3.7 pct

- UK insurer Saga says planning to raise $927 mln in London float

- British American Tobacco posts lower revenue on forex hit

- Argos owner sees profits rise as turnaround push shows promise

- Antofagasta Q1 copper output falls due to plant maintenance

- Next ups profit guidance after strong quarter

- Devro appoints new chairman

- Standard life assets rise in first quarter

- Pub firm Greene King to meet FY market expectations

- Tug boat strike may halt BHP, Fortescue iron ore exports

- Ladbrokes Q1 profit tumbles, says to maintain dividend

- Nichols says on track after good start to 2014

- Kazakhmys Q1 copper output falls, focuses on lowering costs

- CSR first-quarter revenue falls 24 pct