Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

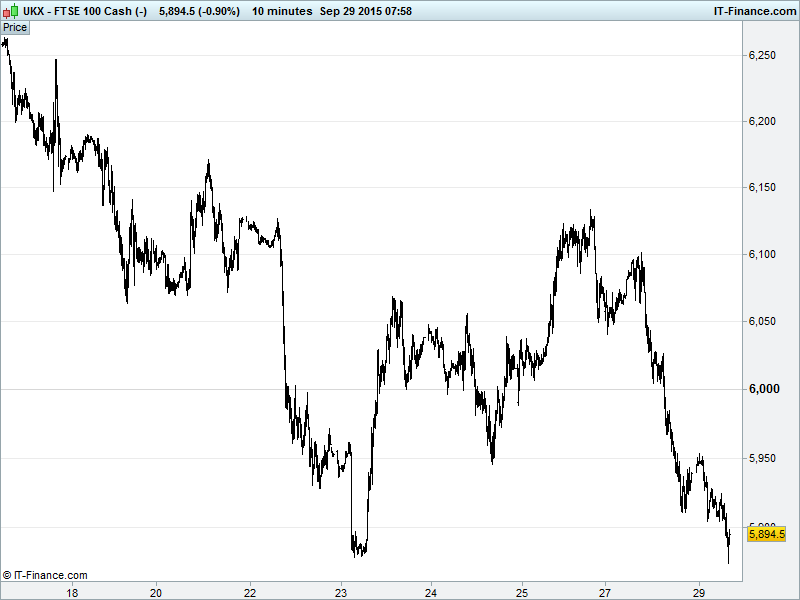

UK 100 Index called to open -60pts at 5900 with share prices adding to yesterday’s heavy losses following an overnight bounce failing to overcome 5950. While we are holding the 5900 level, it’s only just, and there is a strong chance that September lows 5879 are revisited and, if current pressure persists, the 2015 lows of 5770 posted in August can’t be discounted. Updated watch levels: Bullish 5960, Bearish 5870.

The negative opening call comes after yesterday’s 2-3% losses in Europe and the US spilled over into Asia overnight, where the retreat was even sharper (down 3-4%) as resources-focused names suffered from the ‘Glencore rout’ and intensification of widespread/long-held commodity price concerns from a slowing China and global supply glut.

Australia’s ASX is held back by its mining contingent although the sector’s long-running woes mean that the once synonymous sector accounts for less than 14% of the benchmark, down from a third in 2008 to its the lowest level since 2002.

In Hong Kong, Chinese stocks are facing their worst quarter since 1998 amid a commodities sell-off and growth uncertainty for the world’s second largest economy. Note a Nikkei report that China’s GDP may just be 5% in Q2 versus the 7% official figure, which is adding to the China weakness story hanging over markets.

Monetary policy wise, while we all fret about the Fed raising rates by a measly quarter point sometime in the next 6 months, note the Reserve Bank of India cutting its key rate by 50bp (the fourth cut this year), more than expected due to weaker growth forecasts. Voila the differing prospects the world over with US rate rise prep in the face of QE and rate cuts elsewhere.

On the geopolitical front, speeches by Obama and Putin at the UN yesterday highlighted the difficulties and strained relationships facing world leaders in coordinating efforts to calm things in the Middle East and Syria in particular.

US equity markets, like their global peers, amassed sizeable losses yesterday as the China-commodities conundrum worsened worldwide. Fed chatter continues in overdrive with Charles Evans warning against a premature US interest rate hike - premature being ‘in the current climate’ of ongoing low inflation. He sees mid-2016 as more appropriate (since inflation will, of course, be at target by then…) unless inflation somehow explodes upwards in the near future. #likely.

Like all good commentators, Evans put forward his suggestion for normalisation, ‘The Evans Plan’ of 3 x 25bp increases by end 2016 while covering himself by suggesting QE as the alternative. Dudley still supportive of a rate hike before the end of 2015 while Williams echoed that while adding that arguments for ‘patience’ (is patience making its way back into the Fed dictionary?) still currently outweigh those for normalisation.

With global markets increasingly fragile amid loudening cries of equity overvaluations, irresponsible borrowing and a looming catastrophe (to quote Carl Icahn), perhaps higher interest rates are what’s needed to take things down a peg or two, since the alternative may be a drop of considerably more pegs!

In focus today we have Eurozone Confidence figures which are expected to be pretty much unchanged in September. UK CBI Sales are seen improving at, while Germany shows deflationary Consumer Price Inflation (following worse than expected import price contraction this morning). In the afternoon, US House Prices are seen having rebounded gently in July, although US Consumer Confidence may have given up some ground, in contrast to last Friday’s Uni of Michigan rebound.

A weak outlook for oil amid a global supply glut has been weighing on oil prices this week. WTI ($44) dipped below $45 while Brent currently at $47 ahead of weekly US inventory data that is expected to indicate a drop in supply, this seemingly taking a back seat to more pressing issues. With key consumer China due to take a week off, we’d expect low trade volume and growth concerns to balance or outweigh bullish stockpile readings from the US.

Gold ($1144) held its biggest drop in 4 weeks on a cautiously hawkish yet balanced US Federal Reserve, with safe haven demand surprisingly muted amid a global markets slump. Mind you, fixed income markets expectant of higher US rates will be keeping the Dollar flying and gold out of favour with foreign investors.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Euromoney buys 10% interest in Zanbato

- Hammerson JV buys loan portfolio secured against Dublin property

- 3I Infrastructure says on track to deliver FY dividend

- Panmure Gordon posts H1 pretax loss of £0.2m

- Staffline Group to acquire Milestone Operations

- Boohoo first half profit up 39%

- Gulf Marine Services says GMS Scirocco awarded contract

- Wolseley lowers H1 forecast, buys back shares, raises dividend

- Quindell says received "notice of intended claim" from a law firm