Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

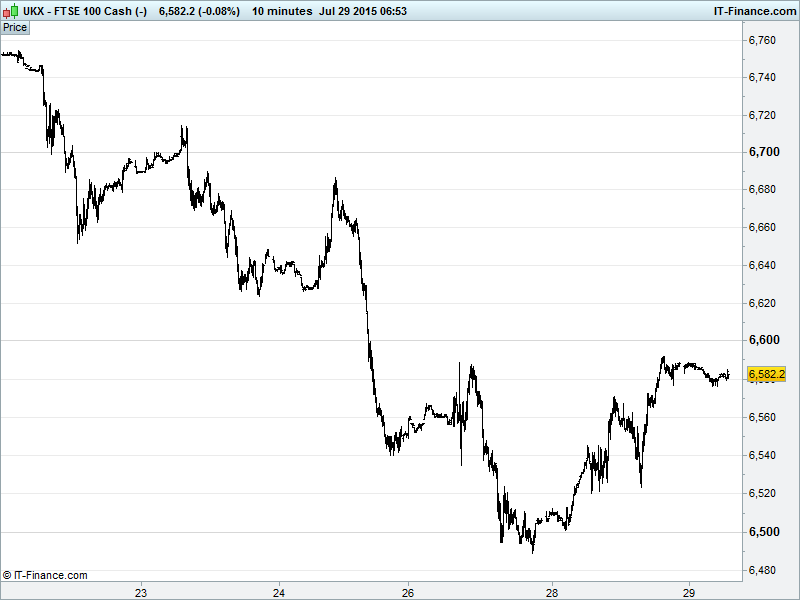

UK 100 Index called to open +35pts at 6590 with the bounce from 6500 support taking the index back above 6550 and to Monday’s highs overnight. Sideways since, we are now testing falling highs from 21 Jul highs with the next hurdle being 6600. Watch levels: Bullish 6605, Bearish 6545.

A positive opening call comes after a stable Asian session as typical apprehension sets in ahead of the latest US Federal Reserve monetary policy update and with China shares still under pressure despite stable/positive macro data. News that Greek stock market could reopen Thursday is adding to optimism on the latest bailout as negotiations with senior creditor representatives start today.

Investors on the one hand worried the US Fed will point to a September/Q3 rate hike and an imminent start to interest rate normalisation, but on the other hand hopeful ‘external events’ such as Greece and China allow it to hold off for longer (Q4/Q1). A glance at recent USD basket weakness suggests later rather than sooner, however, whatever the Fed says is likely to lead to market volatility given the importance of USD as a currency and Fed as a central bank post-crisis.

US markets closed 1% to the good, putting an end to their longest losing streak since January thanks to continued bargain hunting from recent lows, better than expected Q2 results from global growth barometers United Parcel Service (UPS) and Ford (F) and pharmaceutical giants Pfizer (PFE) and Merck (MRK) and a rally by Energy and Raw Material producers along with the bounce in Oil and Copper. Note Twitter (TWTR) results beat, but progress assessment and outlook soured sentiment.

A more chilled out China and late in the day gains on Wall St. set the tone for Asian bourses overnight amid assurances from the Chinese government that it would continue to stabilise the market (in its own special way, no doubt…). Shanghai composite is currently down 1% - nothing on the near 8% losses seen on Monday but still obviously under pressure.

Spooked (not to mention margined to the hilt) retail investors keen to follow the cues from the China Securities Finance Corp, widely believed to be already selling off the holdings it bought to shore up the market way ahead of a 4,500 target for the Shanghai Comp. that was set by the government on 4 July.

In what is essentially separate news from China, consumer confidence as a whole came in +1.9% in July bringing it back to last year’s levels just before housing market and economy worries surfaced. Most household finances led the increase (immune to stock market woes?) while those in tier one cities (more likely to be exposed to swinging equities) suffered a little.

Other equities in the region mixed with Japan’s Nikkei down but the Aussie ASX in the green following a temporary improvement in the commodities sphere that boosted Anglo-Australian mining stocks. Note we stress the word ‘temporary’ here with an impending US Fed policy statement more than likely to prolong the agony currently felt by those in basic materials.

In focus today aside from the Fed update this evening will be UK Consumer Borrowing and Mortgage Approvals data this morning, forecast stable and growing respectively. In the afternoon, watch out for US Pending Home Sales after yesterday’s weak S&P data and Friday’s New Home Sales plunge. On the results front results from Facebook (FBK) will be looked to after Twitter's disappointment, while Hilton (HLT) and Mastercard (MA) may offer signs on consumer and business confidence.

Oil prices remain pressured ahead of today’s US Fed policy meeting with expectations of an imminent US rate hike and results from oil majors showing drawdowns in production and capex cuts causing market indecision (evident in yesterday’s spinning top candle on the Brent Crude chart). Both Brent ($53) and US Light ($48) appear to be waiting around support for fresh drivers.

Gold ($1097) so far unable to breach resistance just below $1,100, although rising lows since 25 July could help it break that level today. More likely, though will be the prospect of US interest rates going higher in 2015 taking attention off the non-interest bearing safe haven in favour of US treasuries.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Barclays says to speed up cost costs, asset sales

- British American Tobacco first-half sales hurt by currency moves

- Capita sees organic growth accelerating in 2016

- WS Atkins maintains positive full year outlook

- Tullow remains in the red as weak oil prices eats into revenue

- Compass maintains positive revenue expectations

- Taylor Wimpey first half profit rises by a third

- National Express confident on 2015 after HY profit rises

- Lancashire Holdings H1 gross premiums written falls nearly 33%

- Pets at Home says FY outlook remains in line with market expectations

- Sky edges FY profit forecasts with record demand

- Antofagasta cuts annual copper output forecast on Antucoya project delay

- Brewin Dolphin Q3 funds, revenues hit by weak markets

- Rightmove says confident of delivering on its FY expectations

- Man Group gets H1 profits boost, but sees net outflows

- Telecity Group says trading in line, reiterates guidance

- Pub group M&B posts 0.8% rise in Q3 LFL sales

- 3I group realises £229mn from private equity assets

- Foxtons on track to meet FY expectations with stronger H2

- St. James's Place sees H1 profits dip but funds, cash rise

- Greggs edges up year guidance on strong first half

- Ocado to establish ADR programme in U.S.

- Quintain receives, recommends bid by private equity firm Lone Star

- Premier Farnell sees H1 adjusted operating profit about 10% lower

- British Land sells 39 Victoria Street office building for £144mn

- SSE agrees to buy 20% stake in Total's Shetland project