Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

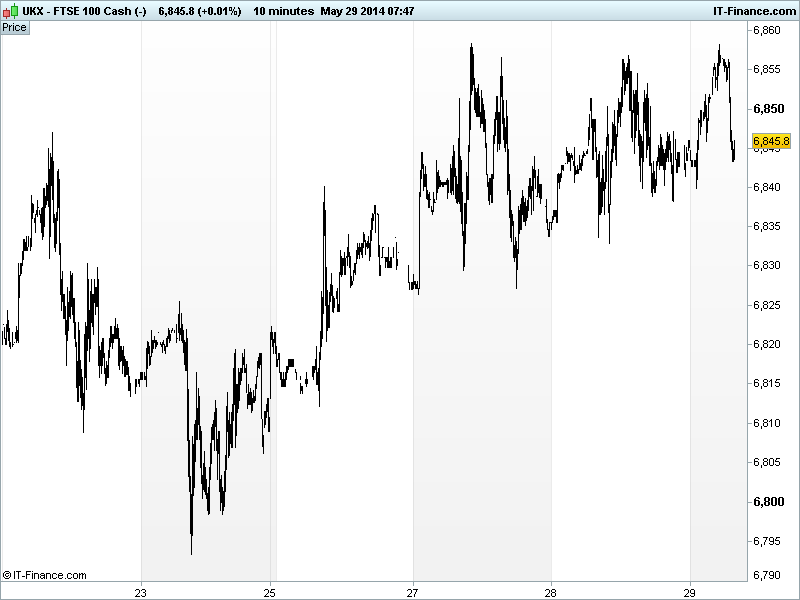

UK 100 called to open flat at 6845 although still trying to break above recent 6858 highs. The 5-day trend of rising lows and horizontal highs could culminate in a breakout from a bullish ascending triangle pattern which could be the fillip for a revisit of 6897 before an assault on all-time highs of 6950. Note many European bourses closed for Ascension Day.

US equities closed lower, ending their 4-day winning streak, retracing from recent all-time highs as weakness crept in to late trading following some disappointing earnings and a bad response to some M&A (Valeant + Allergan) which saw traders adopting a cautious stance ahead of today’s update on US Q1 GDP.

Asian bourses mixed and lacklustre, taking their the lead from the US, after a drop in Japanese Retail Sales (ahead of tax rise) while Aussie New Home Sales rebounded and Private Capital Expenditure remained weak due to the drop in mining investment, although forward CAPEX plans appear brighter. Japan’s Nikkei flat after 5 straight days of gains – its longest positive stretch of 2014.

In Europe, the BoE’s Weale said the bank can wait before its first rate hike, but he’s not sure how much longer, and that it’d be better to start sooner to avoid painful hikes later. Bonds also rallied on speculation the ECB will cut interest rates in the Eurozone to bolster stimulus next week.

In focus today will be the US GDP (2nd Est) which is expected to show a revised contraction in Q1 which could dampen the current bullish mood. Personal Consumption is seen holding up at above 3%, while Jobless Claims are expected to have improved. Consensus sees US Pending Home Sales growth slowing in April.

On the corporate front, Apple has agreed to buy Beats Electronics for $3bn ($2.6bn cash, $400m shares), adding music streaming, high-end headphones and music-industry connections to its stable.

Gold trades at a 16-week low of $1255 as worries about tensions in Ukraine ease with PM Yatseniuk asking Putin to block the border to prevent guerrillas entering the country, which could eliminate the crisis swiftly. Key is the drop below support at $1,262 which could mean technical pressure continues to weigh in the days ahead.

WTI has fallen back below $103/bl ahead of US inventory data this afternoon, while Brent continues to lose momentum on the prospect of a geopolitical calming between Ukraine and Russia.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP Retail Trade Mixed, deteriorated

- AU New Home Sales Improved, rebound

- AU Private Capital Expenditure Miss, stayed weak

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Paypoint full-year pretax profit rises

- Severn Trent posts 7 pct rise in FY pre-tax profit

- Mysale Group seeks London AIM listing

- B&Q sales surge boosts Kingfisher profit

- Man Group confirms in talks to buy Numeric

- Centrica exec Weston named CEO of Aggreko

- Oxford Biomedica plans 20 mln stg fundraising, 5 .7 mln stg open offer

- Tate & Lyle posts lower earnings, sees tough year ahead