Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

UK 100 called to open +20pts, despite holidays in Japan and China meaning a quiet regional session for Asia, however, Australia in the green, outperforming peers, despite an absence of news and headlines bar Saturday’s slower reading on Chinese Industrial Profits growth. The IMF did, however, lower its growth estimate for Asia-Pacific from 5.9% to 5.7% noting China’s vulnerability to a slowdown.

Australia benefiting from continued expectations of central bank easing (most notably the Fed) after Friday’s weaker than expected and yet still decent US GDP figure, keeping the USD on the back foot versus GBP, but less so versus EUR on competing hopes of an ECB rate cut due to recent very weak regional macro data.

Flatter EUR/USD seen commodities lose a bit of momentum after recent gains, possibly taking a similar pause for breath to equities since early last week, with a the situation of macro growth uncertainty no more resolved after surprise recent mixed GDP surprises and weak sentiment numbers (US equities closed flat on Friday).

Overnight macro data includes an improvement in UK Lloyds Business Barometer and UK Hometrack housing Surveys. The weekend also saw Italy’s new grand coalition sworn in, ending the political deadlock and helping remove some uncertainty (borrowing costs down).

In focus today will be the Eurozone confidence figures (seen deteriorating), likely adding weight to calls for an ECB rate cut. Division in markets as to when this might be delivered, with expectations ranging from this week to June, but belief in ultimate impact still seen as low in terms of helping Eurozone periphery with credit system’s broken transmission mechanism.

After weak US GDP but better consumption on Friday, US Personal income and spending will be of interest in terms of consumer confidence as will Pending Home Sales. Another manufacturing survey to close the day, with Dallas Fed updating. Better or worse than peers?

Later in the week, Central banks the focus (Fed and ECB) as well as the traditional first Friday of the month US Non-Farm Payrolls and global PMIs. The former watched most notably for any change in FOMC outlook in terms of QE, which could impact risk appetite and so USD, financials and commodities/commodities-linked names.

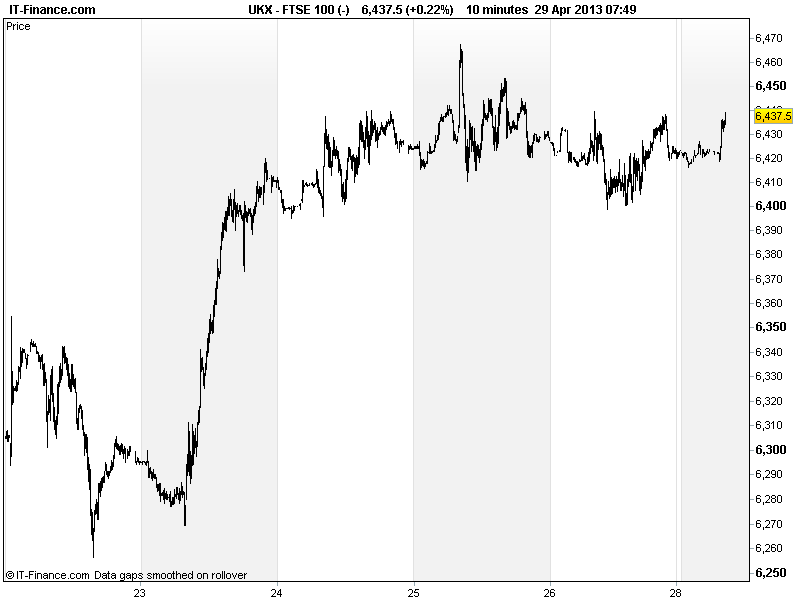

UK 100 still trading sideways from last Wednesday, likely awaiting more confirmation on global growth signals before deciding how high to pin their colours on the risk appetite mast. Range-bound in a very narrow 6400-6440 for now, but a very busy macro week should manage to see a break.

Gold still trading up near recent highs, although with a pause since Friday around $1470, following the solid rebound from 2yr lows of $1321. This week’s central bank meetings could dictate USD direction and help/hinder demand for the yellow metal.

Oils slowed up and taking a breath on account of EUR/USD bouncing around 1.30-1.31, with US Light Crude weakening back from $93.5 to $92.5. Brent Crude sideways around $103.

In FX, GBP/USD rallied to above 1.55 on expectations weak US GDP seeing Fed’s QE continue/accelerate rather than taper. EUR/USD sideways with hopes for an ECB rate cut competing with hopes for more Fed QE.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Industrial Profits Deteriorated

- UK Lloyds Business Barometer Improved

- UK Hometrack Housing Survery Improved

- See Live Macro calendar for all details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Lloyds to sell Spanish retail business to Sabadell – paper

- BHP Billiton to sell Pinto Valley mining operation to Capstone for $650 million cash

- Greggs sees full-year profit below market expectations

- Rentokil Initial's Q1 adj profit up 11.1 pct

- Rentokil to sell City Link for 1 pound

- LSE makes public Italian valuation report

- Greene King like-for-like sales up 2.2 pct

- Fresnillo to ensure minimum free float via placing

- Innovation Group signs partnership deal with AXA France

- ViaLogy signs collaboration deal with CGG

- Eurasia Drilling says Q1 revenue up 6 pct y/y

- Fund firm Aberdeen posts 25 pct jump in H1 revenues

- Balfour Beatty to significantly miss 2013 profit forecasts