Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

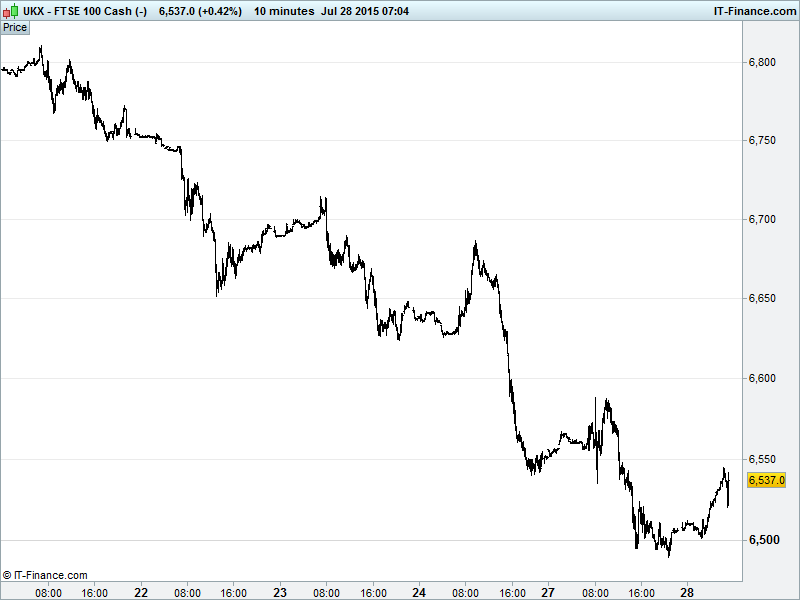

UK 100 Index called to open +30pts at 6535 having found support around 6500 overnight following an extension of the recent sell-off to 327pts (-4.8%) from mid-July’s 6815 highs. Note said support just above 9-month rising lows at 6475, meaning potential for correction to be over and due a bounce, however, breakout >6550 likely required before bullishness returns. Watch levels: Bullish 6555, Bearish 6480.

The positive opening call comes despite Chinese stocks delivering another highly volatile session (slump, pare losses, slide, pare losses again), with bargain hunting, strength in banking stocks from market intervention (mass buying/injection, investigating ‘malicious selling’; losing control?) and a rebound by Copper helping, but uncertainty still rife as the market adjusts to bursting of stimulus-led and margin debt-fuelled equity bubble.

US markets closed lower, extending their declines (first 5-day losing streak in 6 months) on concerns Chinese stock market intervention being pared, weakness in European bourses, a disappointing downward revision for May’s US Durable Goods Orders ex-transport and anxiety ahead of the Fed FOMC update tomorrow evening which could provide markets with the clearest signal yet on the timing of the first US rate rise in 9 years.

Asian bourses followed China lower overnight after Monday’s equity rout (the sharpest one day crash in 8 years with losses the equivalent of Italy’s entire equity market). Efforts by the PBoC to shore up the market have led to margin debt reaching $1.2tn as investors the world over fear the peoples' government is losing control of the situation. It was never really in control though, was it? Things look to have stabilised somewhat this morning while ‘volatility’ will certainly be the term of the day in Asia.

While Metals are showing some resilience with Copper bouncing from a 6yr low thanks to Chinese government assurances that it would continue to work to stabilize its stock market after the recent rout, note oil still under pressure extending bear market decline (down >20%) due to global supply glut (Iran about to return; US stockpiles forecast to grow) and USD bounce.

In focus today will be the UK’s GDP update with expectations for an acceleration in growth from 0.4% to 0.7% in Q2 which could have a knock on for Bank of England rate rise forecasts and thus the GBP. Any updates on Greek bailout negotiations (low level talks) likely to attract much attention given ECB rejection of stock exchange reopening proposals and IMF calls for debt relief

In the afternoon we expect US House Price data to have been solid in May, the US PMI Services and Richmond Fed index to tick higher, although Consumer Confidence may have dipped. Note US Q2 results from heavyweights Ford (F), Merck (MRK), Pfizer (PFE), Twitter (TWTR) and global growth barometer UPS (UPS)

Oil prices still near four month lows, under pressure as are many commodities as confidence wanes in China’s economic health, about which the current stock market wobbles say very little, incidentally. Now officially in a bear market with global supply glut concerns, the prospect of another big player in Iran entering the market and a US Dollar still too strong to boost demand in any meaningful way making the short term outlook pretty dire. Brent currently $53 while US Light Crude at $47.

Gold ($1097) off 25 July lows but still hovering near its lowest levels since 2010. While turmoil in Asia should be bolstering the yellow metal on uncertainty, the prospect of a coming US interest rate hike is keeping investors from the non-interest bearing safe haven’s door for the time being.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Zurich says weighing up bid for British insurer RSA

- BP misses second – quarter profit forecast on spill charge

- Next raises annual profit and sales guidance

- ITV sees net ad revenues improving gradually

- Jardine Lloyd Thompson Group H1 underlying pretax profit up 10%

- GKN to buy Dutch aerospace supply firm for €706mn

- Segro pretax profit £330

- Elementis H1 rev $360.4mn

- Power producer Drax starts strategic review

- Aquarius Platinum attributable production up 6%

- Melrose to sell Elster business to Honeywell for $5.1bn

- Mondi H1 basic HEPS 57 – 62 cents, up 18 – 28%

- Virgin Money Holdings (UK) H1 underlying pretax profit up 37%

- Pace sees FY revenue between $2.65bn to $2.72bn

- Informa's H1 pretax profit £121.9mn vs £100.2mn

- UK's Domino's Pizza on track as H1 profits rise 31%

- Acromas sells Saga shares for 205p each

- Hikma Pharmaceutical buys Roxane Laboratories and Boehringer Ingelheim Roxane Inc

- Ofcom questions Royal Mail's wholesale pricing strategy