Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

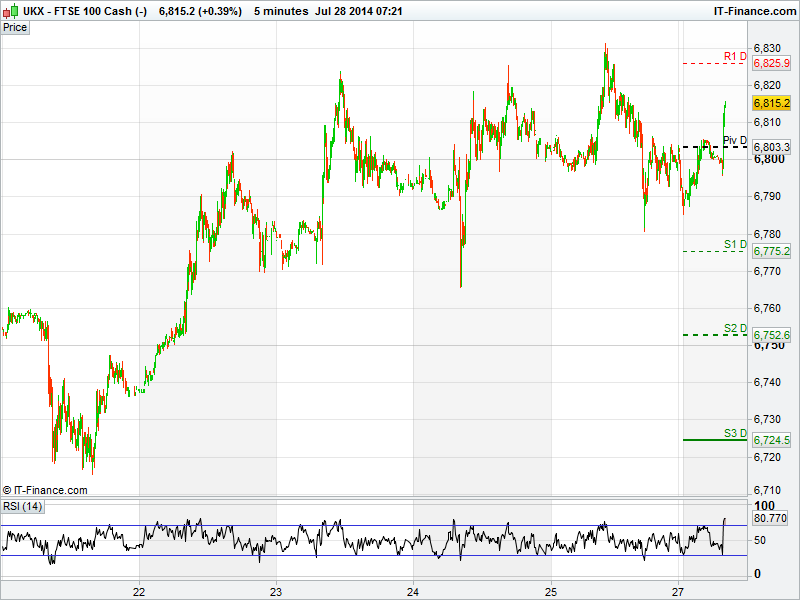

UK 100 called to open up 28pts at 6816, having shed 30pts on Friday with traders taking some risk off the table ahead of the weekend.

The star of the show was Royal Bank of Scotland (RBS.L), shares in the bank, 80% owned by the taxpayer, closed 10.77% higher after notifying the market of a doubling in first-half profits to £2.65bn.

This news also helped Lloyds Banking Group (LLOY.L) and Barclays (BARC.L) advance. Shares were up 1.16% and 1.66% respectively. Traders should be prepared for more news from the sector - Barclays reports its first half trading figures on Wednesday, Lloyds on Thursday and then RBS provide a full report on Friday.

First half results also pushed shares higher for Anglo American (AAL.L). Shares closed 3.44% up on the day after the chief executive said he remained confident that he can deliver the company's promised improvement of the business in the next two years despite weak commodity prices.

At the foot of the table was BSkyB (BSY.L) as the company's latest trading update detailed plans to acquire Sky Deutschland and Sky Italia for £5.3bn. In the longer term the transaction will "create a world-class, multinational pay TV business" according to BSkyB chief Jeremy Darroch, however in the short term the company will part will a significant amount of capital.

U.S. Stocks slipped into the red on Friday on continued profit taking. Corporate earnings have push share prices higher across the board helping the S&P 500 record a record high during the week.

Reports of escalating tensions in Russia/Ukraine combined with high share prices led to traders cashing out with a 'we'll see where we stand on Monday' attitude.

The Dow Jones closed lower by 123pts at 16,960 and the S&P 500 retreated from a record level of 1,991pts to close at 1,978pts.

In focus today we have little from the Eurozone having to wait until the afternoon with US Markit PMI at 14:45pm and US pending home sales at 15:00pm.

In commodities, gold had its first weekly back-to-back losses since May, trading around the $1300 level, but still up 8.6% this year. Hedge funds though last week increases their bets on a gold rally. WTI fell for the fourth time in five days, down 1% last week, amid speculation of a slowdown in growth in the US trading at $101.50 a barrel. The dollar traded near the strongest in eight months against the euro as investors raised bets it would climb versus the single currency to the most since November 2012.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Pace says Roddy Murray stepped down from board with immediate effect

- Pace H1 revenue falls 13.6 pct to $1.14 bln

- Premier Oil names Richard Rose as FD

- Petra Diamonds full-year production rises 17 pct

- Hiscox H1 pretax profit falls

- Trinity Mirror sees full-year results ahead of forecasts

- Reckitt Benckiser to spin off pharma business

- Mothercare says confident of ongoing strategy

- National Grid says keeps outlook for 2014/15

- Aberdeen AM June quarter assets hit by client withdrawal

- XP Power profit rises on China, Vietnam push

- Great Portland Estates portfolio value rises 3.8 percent in Q1

- JKX Oil & Gas H1 revenue falls 18.6 pct