Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

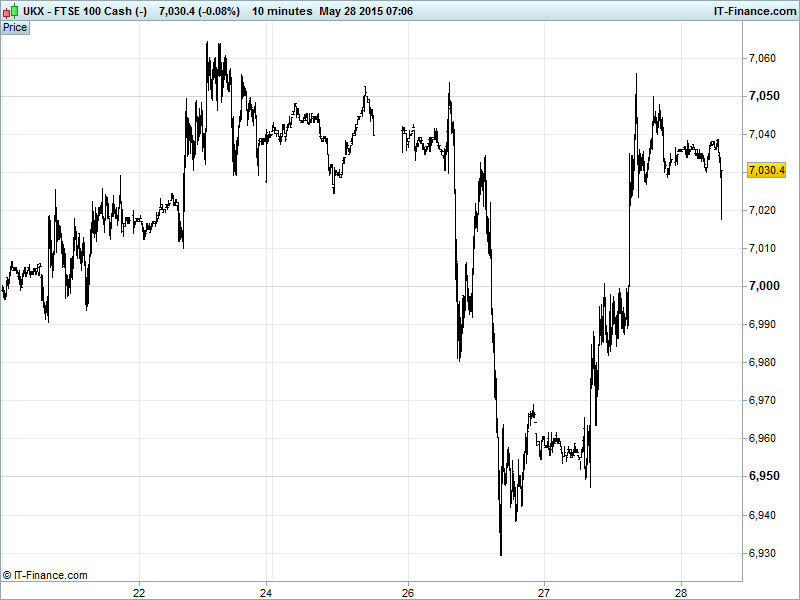

UK 100 Index called to open -5pts at 7025, with yesterday’s market rebound again struggling to better the key 7050 level, finding double-whammy resistance from the duo of April falling highs and the recently breached and now intersecting trend-line from 7 May lows. Watch levels: Bullish 7075, Bearish 6975.

The tepid opening call comes after Greek government officials suggested on Wednesday that they were close to a deal with creditors over fresh bailout funds. EU officials poured cold water on the claims, however, saying negotiators still had much work to do before sealing a deal.

Investors nonetheless seemed confident in certain details (no risk to Greek salaries, pensions, bank deposits) of the Greek claims to keep European equity markets in the green this morning. US markets also posted gains off the back of the Greek news, with the Nasdaq the outperformer, making fresh all-time highs.

Asian equities seeing another mixed session despite a positive finish on both sides of the Atlantic with Greece’s debt deadline looming large and it remaining unclear whether an agreement can be reached. Be prepared for unhelpfully conflicting headlines (deal, no deal) from both sides of the negotiations continue.

Japan’s Nikkei making it a 10-day winning streak (longest since 1988) and fresh 15yr high thanks to a stronger USD on Fed rate-rise expectations sending the USD/JPY to its lowest in almost 12 years and the BoJ’s Kuroda saying an asset bubble not brewing and despite Retail data failing to rebound as much as forecast.

Note Chinese stocks lower, ending their 7-day rally on worries that the government will intervene to cool a rampant equities market and HSBC cut its China GDP outlook (to 7.1% from 7.3%; softer external demand, yuan strength) which is seeing Hong Kong’s Hang Seng underperform overnight.

Australia’s ASX just in the red, lead lower by a USD-hindered basic materials sector following a 3rd straight quarterly disappointment for Private Capital Expenditure as mining investment declines from historic highs and China fears (intervention, growth cuts) has a negative knock-on.

In Focus today we have UK GDP at 0930, Eurozone confidence data at 1000 and US employment prints this afternoon. Traders will be watching the US data closely for further indications of a Fed move on interest rates in the absence of other boat-rocking news on that front.

Crude oil prices still trending down, although of their May lows this morning as worries of a supply glut eased on forecasts of a supply/demand re-balance in late 2015. Nonetheless the prospect of increased US stockpiles (Arctic drilling, fracking…) is keeping gains modest at best. Brent currently at $63 while US cousin WTI trading around $58.

Gold holding support around $1185-1190 thanks to rising support from mid-March. USD hindering any advances, despite uncertainty linked to Greece and global growth after poor Aussie investment and SBC cutting China GDP estimates. Support $1185, Resistance $1205.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan Retail Trade Miss, Rebound as not as strong

- Australia CAPEX Miss, contraction worsened

- Germany Import Prices Beat

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Applegreen says it intends to float on AIM and ESM

- Retailer B&M posts 56 pct full – year profit rise

- Kingfisher posts Q1 profit rise

- Serco names former Compass boss Gardner as non-exec chairman

- IG Group says remains on track to deliver FY expectations

- PayPoint's full-year pretax profit rises

- Tate & Lyle posts lower profit in line with its guidance

- Amec Foster Wheeler wins contract from government of Timor-Leste

- Sports Direct lifts profit outlook on lower interest charges

- Falkland Oil and Gas says oil discovered at Isobel Deep well

- Optimal Payments acquires FANS Entertainment Inc for about $13 mln

- Screwfix helps Kingfisher to first-quarter profit rise

- Ferrexpo Q1 core profit falls 41 pct