Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

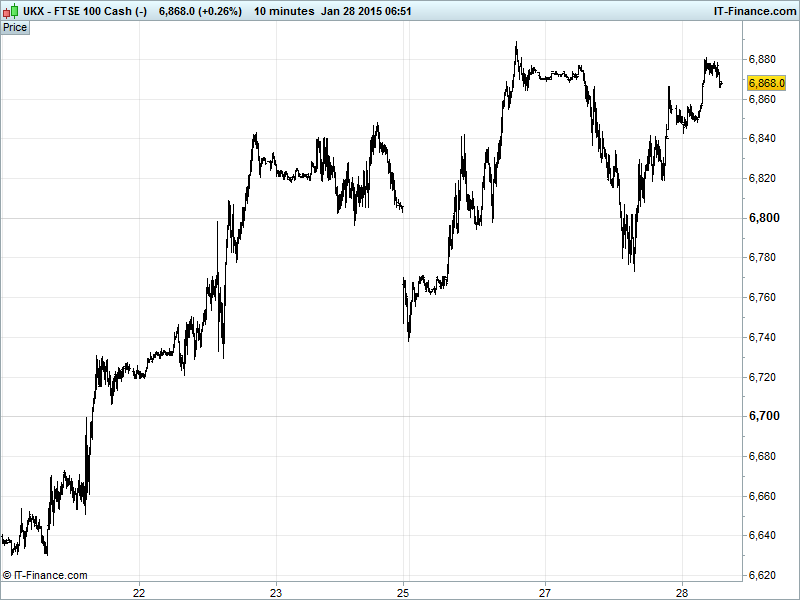

UK 100 Index called to open +50pts at 6860, having rebounded strongly overnight from yesterday’s test of rising support from 19 Jan around 6800. While the January uptrend remains more or less intact, note overnight highs no better than those of Monday night. Updated Watch levels: Bullish 6910, Bearish 6800.

Drivers for the positive open include, after the US close, very strong results from Apple (AAPL) on record iPhone sales and Yahoo’s (YHOO) announcement that it would extract value via a tax-free spin-off of its 40% stake in Alibaba (BABA). This helped buoy market recovery sentiment from the day’s lows along with recent macro data pushing Fed rate hike expectations out yet further ahead of today’s Fed Statement.

US bourses closed lower, hurt by weak corporate earnings (blame the strong USD) and a plunge in Durable Goods orders (less planes), but off their worst levels helped by better US Consumer Confidence and New Home Sales and reports in Italy’s La Repubblica that EU and Greek officials have already agreed to push back its debt repayment schedule (first payment 2020, last 2057) with lower interest rates on loans.

Overnight, Asian bourses just positive thanks to Apple results and Yahoo announcement, mixed US macro data raising concerns that the Fed may delay a rate increase (note Singapore added itself to list of recent rate cuts to counter low inflation), and easing concerns about Greece’s perilous debt situation and new government stance. Note Japan’s Nikkei hindered by stronger JPY and weak US corporate earnings.

Overnight data included stable China Consumer sentiment and falling Australian inflation. This morning Germany reported weaker Imports Price index which supports the ECB’s recent move to QE but this was offset to some extent by better Consumer Confidence.

In focus today after a volatile session yesterday to say the least, will be the Fed statement this evening where language will be analysed for changes in view towards rate rise timing given low inflation and mixed data of late. With oil in focus, keep an eye on US Oil stocks mid-afternoon and with US corporate results disappointing, on account of strong USD, note potential for Boeing (BA) and Facebook (FBK) to feel pain too.

Gold back below $1290 after its bounce off the trendline of 2015 rising support with the equities market recovery offsetting gains from the weaker USD (Fed rate rise expectations pushed out) and safehaven demand as Greek concerns reduced even if US corporates disappointed.

US Light Crude and Brent Crude still trading off support at $45 and $48, respectively, helped by a slightly weaker USD (due to push back in Fed rate hike expectations) and OPEC warnings on price surge without investment but hindered by reports that Saudi Arabia has secretly increased oil output to the highest since last October in an effort to win the price war against US Shale frackers, exacerbating the supply glut.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Australia Consumer Price Inflation Miss, deteriorated

- China MNI Consumer Sentiment Fell slightly

- Germany Import Price Inflation Miss, deteriorated

- Germany GSK Consumer Confidence Beat, improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Fresnillo says FY silver production exceeds guidance

- Severn Trent says James Bowling to take over as CFO on April 1

- Gulfsands Petroleum sees 2015 capex at least $2.5 mln

- Anglo hits production targets but flags writedowns ahead

- Petroceltic recommends shareholders vote against Worldview resolutions

- Severn Trent to launch share buyback programme

- AA Plc gets nod for premium listing of shares

- Johnson Matthey sees rise in full-year profit

- Brewin Dolphin's funds under management jumps to 37.9 bln pounds

- Copper miner Antofagasta hits annual output target

- Canary Wharf owner Songbird succumbs to QIA-led takeover