Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

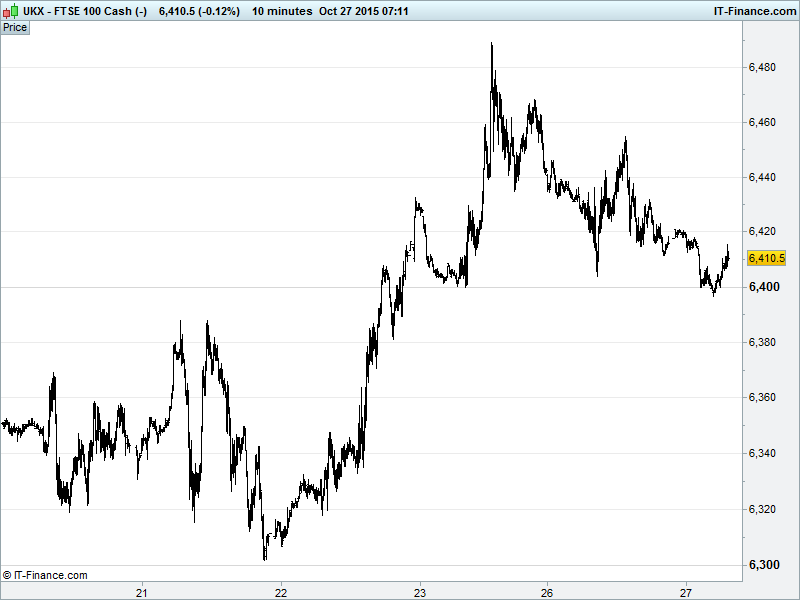

UK 100 Index called to open -5pts at 6410, with another overnight visit of 6400 extending the downtrend from Friday’s 6490 highs. However, the uptrend from end-September is still alive and well thanks to 6400 proving supportive for a third time in as many sessions. We nonetheless look for a break above 6430 before assuming resumption of rally from 5900 towards 6800. Updated watch levels: Bullish 6430, Bearish 6390.

The neutral open comes as markets adopt a now traditional ‘wait-and-see’ attitude in the run up to the Fed’s policy update tomorrow (and BoJ on Friday) with easy monetary policy still desired to buoy risk appetite. We also continue to consolidate recent gains following the PBOC rate cut and ECB ‘more QE’ hints last week which saw equities fly last week.

Stocks in Asia in the red, falling from two month highs and echoing a lacklustre US close, with low volumes as investors await central bank decisions, continued digestion of Q3 earnings as well as a lower oil price (3rd down day, 2-month low) on expectations of US stockpile growth adding to global supply glut concerns, keeping the bulls in their pen and energy names in check.

While uncertainty lurks about the outcome of China’s 5yr economic plan, note US Congressional leaders have reached a tentative budget deal with the White House that would set government funding levels for the next two years and extend the nation's debt limit through 2017, avoiding routine talks of a government shutdown. Another bright spot overnight was Chinese Industrial Profits only falling a touch in September. Almost back to growth?

Poor macro data (new home sales -11% while Dallas Fed Manufacturing Activity posted its 10th straight contraction) and a slump in the oil price weighed on the US Dow and S&P indices. No such woes for the tech-heavy NASDAQ though, which again held just above the waterline, still buoyed by a positive mood in that sphere.

Note the potential exists for bullish ‘buy on the dip’ opportunities in US indices as initial market declines correct back upwards once participants forget bad data and move on to digesting the prospect of record low interest rates for longer following the 2-day Fed meeting which kicks off today. But while the US central bank is probably not going to raise rates in December, be assured we’re unlikely to get any form of confirmation either way this week.

Having not heard from Greece in a while, note German paper Suddeutsche Zeitung reporting that bailout creditors are holding back on paying the first €2bn tranche of €3bn due because PM Tsipras has failed to implement promised reforms on schedule. Creditors finally laying hardball. Greeks voted, Tspiras promised. Fair’s fair.

In focus today we have the first estimate for UK Q3 GDP with consensus looking for a slight slowing and while exports orders data yesterday is a worry, the dominant services sector (70%) should offset with more solid gains. In the afternoon, US Durable Goods are again seen weak, but less so than August and even returning to growth when volatile air and defense elements are stripped out. US House Price growth seen picking up in August coupled with solid PMI Services and Consumer Confidence prints.

The outlook for Gold again lacklustre with investors concentrating on the outcome of this week’s Fed meetup. Volumes likely to remain low for the next couple of days and prevailing dovish winds still blowing in the direction of Loose-Policy Land. The general commodities slump continues to include Oil too this morning with upcoming US inventory data expected to show that the world is still heavily oversupplied with the world’s suppliers still stubbornly supplying too much.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Eurasia Drilling expects 2016 revenue at $1.7–1.8bn

- DS Smith says trading in line with expectations

- BP sees Q4 production to be slightly higher than Q3

- BBA Aviation says new shares to commence trading on Tuesday

- Spirax – Sarco says Finance Director Meredith to retire

- Oxford Instruments says group finance director Kevin Boyd to step down

- Utilitywise changes payment terms with supplier

- St James's Place Q3 net inflows rise 17% to record $2.3bn

- Grafton to buy Isero BV for €91.5m

- Utilitywise names Brin Sheridan chief operating officer

- Equiniti prices shares for London stock market debut

- Aquarius Platinum says Q1 production up 8% from last year

- Bloomsbury Publishing H1 pretax profit falls

- Dialight says does not expect to declare dividend before 2017

- Kenmare Resources HMC production rises 7%