Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

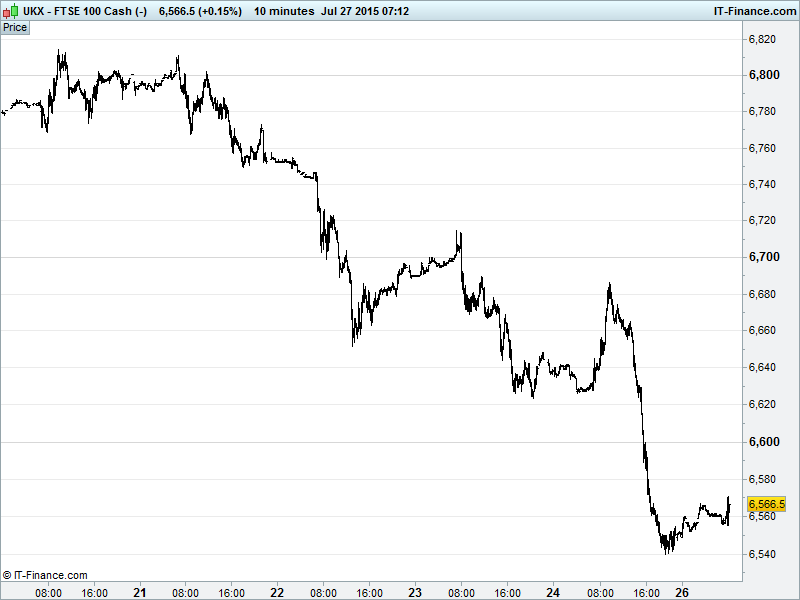

UK 100 Index called to open -20pts at 6560 having found support at 6550 late Friday following a risk-off session which saw the index turn in a 275pt hi-lo range for the week. Long-term uptrend intact but with potential for current correction to fall as far as 6475 before bouncing. Trend of falling highs from last week requires breakout at 6615 to before 6815 can be revisited. Updated Watch levels: Bullish 6605, Bearish 6530.

The call for a negative open comes after a risk-off Friday which saw US markets follow Europe lower and Asian equities put in in a weak session overnight. This is on the back of China’s sell-off resuming (despite all that intervention) and the commodities slump continuing after Chinese industrial profits declined in June, adding to Friday’s weak PMI manufacturing read and the weight of evidence suggesting economic slowdown and need for more stimulus.

US markets closed weaker on Friday (Dow Jones’ worst week since January) as the weight of disappointing corporate results, notably technology names, took hold along with the commodity sell-off, the strong USD and weak housing data falling to its lowest in 7 months offsetting solid PMI manufacturing for the world’s #1 economy. Some reticence to place bets ahead of US Fed meeting and latest GDP read (and revisions).

Asian stocks lower on weak China data and Oil sell-off as well as caution ahead of the US Federal Reserve meeting which could provide clues as to whether we should expect a September or December rate rise. On the results front as we move towards UK names reporting, note Swiss Investment Bank UBS being forced to pre-release better than expected Q2 results with profits +53% after a local press leak suggested growth of just 25%.

While Greece had moved to the back-burner note final negotiations on a third bailout are encountering hurdles with Athens making life difficult for creditors wanting to oversee correct use of rescue funds. This compounds the political pressure PM Tsipras finds himself under having had to accept a more stringent offer, painful capital controls in place and a stock exchange still closed, while ex-PM Varoufakis has revealed 'plan B' discussed internally which may erode creditor trust in reforms

In focus today will be German IFO business surveys at 9am although expectations are for nigh on no change in July. In the afternoon, US Durable Goods Orders will be watched given the consensus forecast for a rebound in June. Result-wise, we have no big name US corporates scheduled.

Oil has extended is bear market drop after a rebound in Baker Hughes US drilling rig count (thirds weekly increase) adds to signs that US producers are set to keep pumping despite Saudi Arabia/OPEC doing the same and a clear global supply glut. Note US Light Crude trading around $48 while Brent is sub-$55 not helped by China recent data. Note net long positions in Oil contracted 28% in the 7 days to 21 July suggesting bulls fleeing.

Gold has rebounded from 5.5yr lows of $1077 early on Friday to trade back above $1100 as interest returns for the safehaven metal despite poor performance of late, a strong USD, lack of inflation, no yield and clear absence of investor panic despite plenty to be concerned about with the Greek situation not yet resolved, China slowing, a questionable US results season. Note COMEX data suggesting speculators net short of Gold for the first time as bearish bets increase ahead of the US rate rise.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Acacia Mining says says H1 EBITDA -26% to $97m

- XP Power's H1 pretax profit £12.6m vs £12.2m

- Merlin warns on profit after roller coaster crash costs

- AstraZeneca sells rare cancer drug to Sanofi for up $300m

- Amec Foster Wheeler awarded power contract by Fortum Zabrze

- Dialight group underlying operating profit -74%

- Reckitt Benckiser raises year revenue and margin targets

- Cranswick says financial year started in line with its expectations

- Aircraft parts maker Senior's H1 revenue +9%

- GVC Holdings makes revised proposal for Bwin.Party

- BG says Brazil competition authority approves Shell offer

- Pearson says in talks to sell its 50% stake in The Economist

- Hiscox H1 gross written premiums rise