Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)!

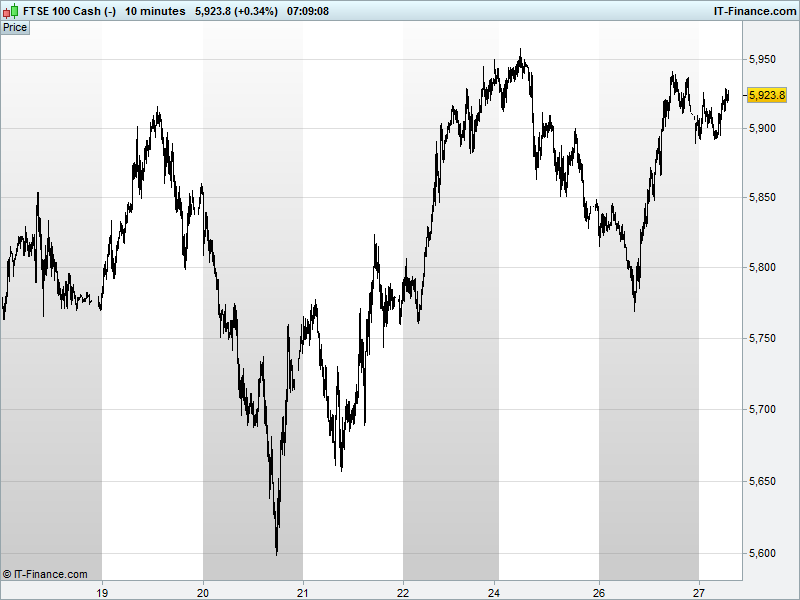

UK 100 Index called to open flat at 5910 potentially in the midst of a bullish flag pattern from yesterday’s lows. However, this requires breaking above Monday’s 5960 highs and the trend of shallow falling highs from 6 Jan, which would excite Bulls with potential for that 2-week complex inverse Head & Shoulders reversal we previously highlighted. Nonetheless, sideways (5890-5940) since yesterday afternoon, and yet to challenge recent highs. Recovery from lows, but Long term downtrend unperturbed. Bullish 5940, Bearish 5880.

The neutral opening call comes after a positive US close on improved US consumer Confidence and Oil retesting >$32, and after another mixed Asian session with Apple results hinting at Q1 likely seeing the first quarterly decline in iPhone sales since 2003 which lead to a mixed reaction from Asian suppliers.

While Asian equities largely in the green - Japan’s Nikkei leading - note Chinese stocks lower (off worst levels thanks to state intervention?). This comes after Oil backtracked on supply glut worries and the World Bank cutting its average 2016 forecast to $37/barrel (will brokers follow?) and industrial names slumped on deepening economic slowdown and capital outflows concerns after Industrial profits contraction worsened in December. More stimulus anyone? Oh, and authorities stepped up investigations into short Yuan trading (Must. Have. Bull. Market).

US markets closed up on Tuesday, yet remain under pressure thus far this year with today’s focus being the outcome of yesterday’s FOMC meeting - which is largely uncertain (save for the fact that rates are highly unlikely to be going up until May at the earliest). Markets are keen to know whether or not the Fed thinks it made a mistake by hiking in December.

While moves in the major US (and global) indices have largely been put down to the oil price, other drivers in the US include the outlook for earnings per share on the S&P500, seen falling in 2016 with this causing some worry as to the strength of the fundamentals in 2015 (again, December Fed rate hike a mistake?). Essentially, are US equity markets overbought?

In corporate news, note an unscheduled update from UK bailed out bank RBS which announced a series of exceptional charges. Aberdeen Asset Management has reported further net capital outflows. Watch shares in ARM Holdings after the Apple update last night while production reports from Antofagasta and Rio Tinto will provide the latest on the commodity sector. UK House Price growth slowed in January, which may impact UK Housebuilders.

In focus today will be the policy statement from the US Federal Reserve which is likely to have a toned down message in terms of rate rise trajectory given the market turmoil since it hiked in December. Data-wise, US New Home Sales seen stable while US Crude Inventories sure to spice up the oil price in the afternoon while we have quarterly results reports from Boeing, Facebook, eBay, Fiat-Chrysler, PayPal and Texas Instruments.

Crude oil prices again rallied yesterday - a main catalyst for the good performance in indices - but are now off overnight highs north of $32, with a slightly wider spread between Brent and WTI. That some Asian bourses were resilient in the face of such volatility is promising this morning (we’ll leave the Shanghai composite at its 13-month low for now!). Short positions in oil are seen much lower this week with an uptick in net longs also of note, while the IMF has cut its 2016 price forecast to $37 - could this be adding some buoyancy?

Gold is taking a pause this morning, its uptrend having steepened yesterday and overnight. We’re currently testing rising support, hopeful that a bounce might take it up above early November resistance $1123 from which it has recently retreated. Above that, $1133 beckons. Watch out for anything that indicates bullishness in the equities sphere though, as Gold has certainly regained safe-haven status this year.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- UK house price growth slows more than expected in January – Nationwide

- Aberdeen Asset Management sees more investors pull cash in the December quarter

- UK lender Paragon sees regulatory changes slowing buy – to – let growth

- RBS to take profit hit from pension charge, US litigation provisions

- London copper edges up as traders eye Fed; China imports support

- Aberdeen Asset Management says Chairman Cornick to retire on Sept 30

- Brewin Dolphin says Q1 total funds up 3.8%

- Antofagasta posts lower FY copper production

- Britvic reaffirms 2016 earnings guidance

- Sage Group says business on track after strong first quarter

- Paddy Power estimates FY oper profit before items of €180m, raises final dividend

- Melrose says shares temporarily suspended from trading

- Wizz Air raises full year profit guidance after strong Q3

- UK Mail appoints of Chris Mangham as executive director