Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

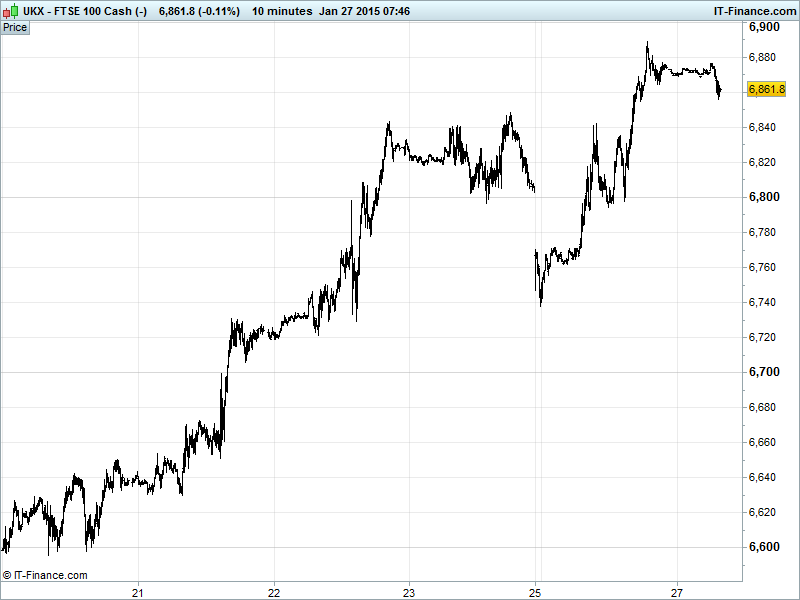

UK 100 Index called to open +10pts at 6860, having made a late breakout at 6850 around the close yesterday to go and test close to 2014 highs 6900 overnight. The mid-January uptrend remains intact, and the hope is that 6850 reverts to support. Updated Watch levels: Bullish 6910, Bearish 6790.

The positive open is despite a flattish finish stateside as the Greek election result was digested and a harsh storm approaches the Eastern Seaboard, coupled with China Industrial Profits growth showing a worsening in contraction in December overnight, adding to global growth worries and emphasising the commodities rout and Russia being downgraded to junk by ratings agency S&P.

US bourses closes flattish to higher amid some lingering but easing uncertainty surrounding Greek funding with the IMF saying it will continue providing assistance to Greece but the Eurogroup head Dijsselbloem saying the Troika’s assistance depended on the newly-elected PM’s stance. US data also weighed, with the Dallas Fed Manufacturing index plunging negative.

After the US close, tech giant Microsoft hit profits forecasts and beat revenues for Q4 helped by its headlong growth into cloud computing although commercial software licensing revenues slipped.

Overnight, Asian bourses largely positive thanks to ratings agency Moody’s saying Asia will be resilient to global macro-economic challenges in 2015, although China hurt by the Industrial Profits growth data. Australia positive after a return from holiday, so an element of catch-up, offsetting mixed Australian Business Conditions surveys and the weak China data.

In focus today we have UK GDP growth seen a touch slower in Q4 although still registering solid annual growth. In November, the key Services component is expected to have shown similar growth as October. Before US data begins, note results from global growth barometers Caterpillar (CAT) and Proctor & Gamble (PG) around midday.

In the afternoon, US Durable Goods Orders are hoped to deliver a rebound in December as are New Home Sales, while S&P Case-Shiller House Prices is forecast to have remained solid in November. US PMI Services expected to improve slightly, while US Consumer Confidence continues to rise. After the US close note results from AT&T (T), Yahoo (YHOO) and Apple (AAPL).

Gold continues to fall back from five-month highs $1300, dented by the strong USD (product of weaker EUR following ECB QE announcement, less pressure from petro-dollar selling, the prospect of a US rate rise and the Fed meeting this week), as equities move higher denting safehaven demand even if uncertainty remains on global growth and Greece’s future.

Oil has also seen some more weakness creep in taking it back towards 6yr lows, with US Light Crude down to $45 and Brent hovering around recent $48 support with global growth and oil supply worries persisting despite OPEC’s warning that without new investment in production prices could surge failing to shift the market’s focus from the supply glut.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Australia Business Confidence Improved

- Australia Business Conditions Deteriorated

- China Industrial Profits Contraction accelerated

- China Conf Board Lead Econ index Growth accelerated

- Japan Small Business Confidence Remains in contraction

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Greencore Group says Q1 revenue up 3.6 pct to 331.9 mln stg

- Aer Lingus recommends $1.5 bln offer from BA-owner IAG

- Carpetright says full year view unchanged

- easyJet says first-half losses to fall this year

- PZ Cussons says H1 operating profit rises 3.5 pct

- Meggitt says Securaplane to supply surveillance system for Embraer's E-Jets E2

- Foxtons sees lower full-year earnings after property sales slow

- Gem Diamonds sees weak diamond prices continuing into Q1 of 2015