Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

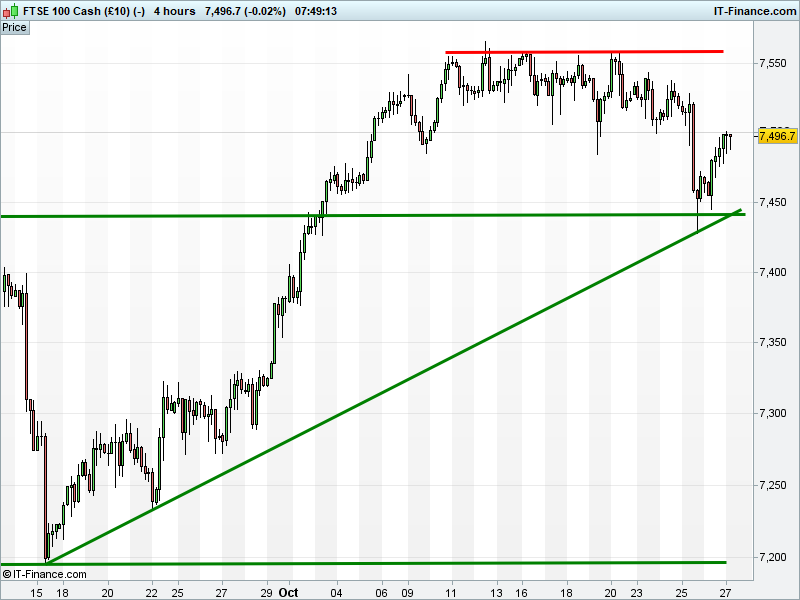

UK 100 Index called to open +10pts at 7495, having extended its rebound to flirt with 7500 overnight. This giving hopes to the bulls of a recovery to recent highs of 7560, although a break above falling highs resistance at 7515 is required. Bears need a breach of rising support at 7475 and then 7450. Watch levels: Bullish 7510, Bearish 7475.

Calls for a positive open come after a largely positive US session was made up for by some after-hours earnings beats from big Tech names that have inspired overnight trading in Asia. After yesterday’s dovish ECB policy update sent the EUR sharply lower, resulting USD strength is having mixed effects ahead of US GDP this afternoon.

Japan’s Nikkei outperforms thanks to the aforementioned dollar rally sending the Yen lower to help exporters. Australia’s ASX, however, underperforms due to stronger USD weighing on both metals and their miners, which may hamper those with a UK Index dual-listing, although oil prices remain firm.

In corporate news; RBS reports higher than expected Q3 profits and capital ratio, although impairments a shade higher; maintains guidance and outlook, still expects to be profitable in 2018. IAG Q3 revs & profit in-line; new 2017 guidance of €3bn operating profit a touch above consensus.

Tullow Oil abandons Araku-1 Well in Suriname. Swiss bank UBS reports 3Q17 profits before tax +39% YoY. Carillion will have a new CEO from next April. Computacenter announces Q3 revenues +27%, or +20% on a constant currency basis; group momentum maintained if not improved. Q4 is a difficult quarter, but company on track for record performance.

US equity markets closed mixed on Thursday as the Dow Jones rallied back towards record highs thanks to American Express and Dow DuPont strength, while rail company Union Pacific led the S&P500 0.1% higher. The Nasdaq closed lower by 1%, however its fortunes could change later today after Amazon, Alphabet and Microsoft - the 2nd, 3rd and 5th largest companies in the world - all beat expectations for third quarter earnings after the market close.

Crude Oil prices have traded fresh 2 year highs overnight following further pledges from Saudi Arabia to address the global supply glut, producing fresh speculation that OPEC-led production cuts could be extended beyond March 2018. Brent Crude has dipped slightly from an overnight high of $59.5, while US has fallen back to former resistance at $52.6 from $52.8.

Gold has fallen to a fresh 3-week low after the ECB announced its long-awaited asset purchasing taper, however the negative reaction from the Euro has seen the US dollar trade at its highest level since July, further denting sentiment. The precious metal is back trading at support around $1266, in close proximity to fresh 3-week lows below $1265 and 2.5-month lows below $1260.

In focus today will be US Q3 GDP (1:30pm) which is forecast to have slowed to 2.5% from 3.1% in Q2, holding around the 5-quarter average, supportive of another US interest rate hike by year end. Inflationary metrics are expected to show improvements which would also be supportive.

With a lack of European data on the calendar today, the only other data to note this afternoon is the University of Michigan Sentiment (3pm), expected to be confirmed today at its highest level since 2004.

Events today, on the other hand, have a distinctly European feel, with Spanish parliament meeting to vote on Article 155 which, if enacted, would dissolve the Catalan government and force direct rule from Madrid on the region. Despite attempts yesterday from Catalan President Puigdemont to de-escalate the tensions between the factions, the Article - Madrid’s ‘nuclear’ option - could spell the end of the region’s latest attempt to secede from Spain.

Elsewhere, speeches from the ECB’s Chief Economist Praet (8:15am), Angeloni (11:45am) and hawkish Weidmann (12:00pm) will likely provide further comment on yesterday’s long-awaited taper, especially with the latter in the running to replace Draghi at the end of his mandate.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.