Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

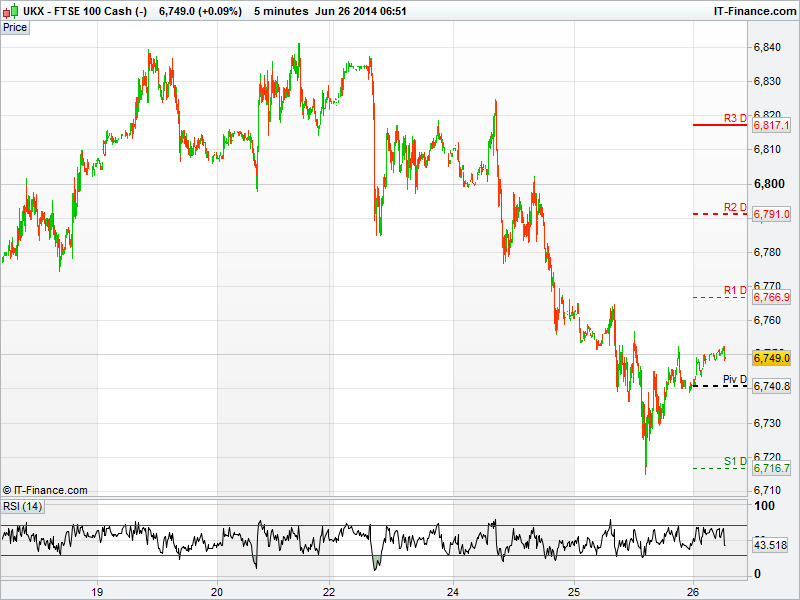

UK 100 called to open up +13pts at 6752, having shed 53pts yesterday on escalating violence in the Middle East.

The Wall Street Journal reported Syrian aircraft had carried out strikes in Western Iraq killing 50 people, prompting fears of retaliation. Traders rightly chose to take risk off the table on this news - 83 of the UK 100 members declined as a result.

However, there were pockets of sunshine in an otherwise gloomy day in the markets. Shire (SHP.L) continued its bid speculation ascent with a near 3% gain yesterday - the share price has advanced 28% in the last 10 days.

Property developers, both commercial and residential, cheered market chatter of interest rate rises being some way off as Bank of England governor Mark Carney acknowledged wages and economic productivity were not increasing sufficiently in the UK.

Five of the seventeen companies that finished the day in positive territory had links to the sector. The notable performers - Hammerson (HMSO.L), Barratt Developments (BDEV.L) and Travis Perkins (TPK.L) up between 0.25% - 0.7%.

US Stocks managed to shrug off worse than expected GDP data for Q1, the market was expecting -1.8% but was presented with a wayward -2.9%, the worst quarterly contraction in five years.

That said the Dow Jones logged an increase of 49pts to close at 16,867pts, the first time U.S. stocks rose in three days as investors watch data for signs of a recovery - Economists predict a gauge of personal spending by Americans today will show gains.

Asian Markets bought into US optimism with gains registered across the board. The ASX200 and Hang Seng notching gains of around 1%.

In focus today at 10.30am BoE’s Mark Carney speaks again on the Financial Stability Report. Later we have US Jobless Claims, and Personal Consumption, Income and Spending released at 13:30pm which can move both currencies and commodities.

In commodities, gold fell slightly to $1316.7 below a two-month high following US GDP data that showed the world’s largest economy shrank by the most in five years. Despite this gold is still on course for its first back-to-back quarterly gains since 2011. Copper advanced for a ninth straight session in New York, capping the longest rally since 2005, amid signs of tightening supply. WTI traded at a three-day high at $106.75 as violence continues in Iraq, OPEC’s second biggest crude producer. In FX, The dollar fell to a five-week low against a basket of 10 currencies after the US economy in the first quarter contracted more than analysts estimated.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

• Carphone Warehouse earnings jump ahead of Dixons merger

• Dixons Retail profits soar ahead of Carphone merger

• Cohort wins UK defence contract

• Costain Group says on track to deliver full year expectations

• Fastjet FY revenue jumps to $53.4 mln

• Ophir fails to find oil in well offshore Gabon

• Wood Group sees FY EBITA ahead of last year

• Monitise buys Markco Media businesses

• DS Smith says FY profit rises to 167 mln stg