Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

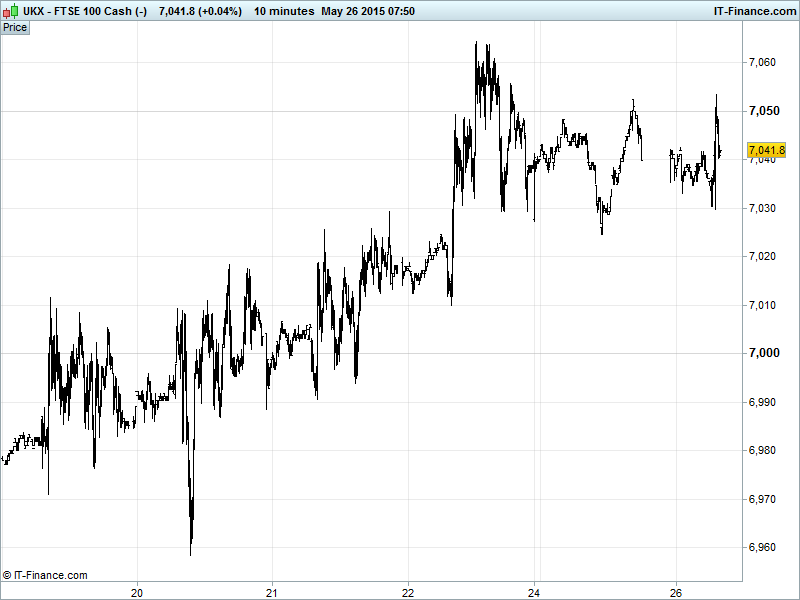

UK 100 Index called to open +10pts at 7040 after the long weekend, holding its May uptrend but with momentum hindered by April falling resistance trend-line at 7050. Support available via May rising lows at 7030 following last week’s 7020 breakout. A break above falling highs needed before revisiting recent/all-time highs 7088 and 7127. Still potential for last week’s bullish ascending triangle pattern to complete 7100. Watch levels: Bullish 7065, Bearish 7015.

The lukewarm opening call comes after European indices ended last week mixed with UK 100 , DAX and CAC40 trading around three-week highs into the long weekend. Greek government spokesman Sakellaridis put forward the country’s desire for a deal by the end of May or early June, adding that a bailout extension would not be needed.

This appeared at odds with PM Tsipras and FM Varoufakis’ comments that Athens would likely default on its next repayment if creditors refuse to make concessions in ongoing negotiations. Meanwhile, the ECB’s QE programme was appraised with government and corporate debt purchases rising by €11.8bn in the week ending 22 May, the smallest increase in 3-weeks.

US bourses closed flat on Friday 22 May with investors squaring positions ahead of the bank holiday weekend. Monday (US, UK and European markets all closed) saw US Fed vice chair Fischer seeking to calm rate-hike nerves by saying that the issue is not when, but by what process policy tightening would happen, and over what time period – namely a series of small hikes over several years.

Asian equities positive with Japan’s Nikkei a touch higher thanks to EUR weakening on regional concerns (Greek debt, Spanish regional elections) which strengthened USD and thus weakened JPY to the benefit of exporting names. Data showing a marked slowing in Japanese Producer Price Inflation has added to JPY weakness (more stimulus needed). Australia’s ASX higher for a similar reason (AUD weaker), helped by utilities as well as perceived benefit from Chinese stimulus.

Chinese stocks registering biggest 6-day gains since Nov ‘08 and Hong Kong hit 7yr highs (playing catch-up; closed yesterday) thanks to continued optimism over Beijing plans to stimulate Chinese economy with >1000 infrastructure projects (worth $318bn; open to private investment), slashing of import tariffs on clothing, liberalisation of capital markets to spur foreign inflows as well as opening of Hong Kong-registered mutual funds to Chinese investors.

In Focus today we have UK CBI Reported Sales looking for a large increase on last month’s print; US Durable Goods Orders pushed down by the transport component (expected -0.5%, ex-transport 0.4%). After lunch it’s an all American afternoon with FHFA House Price Index, Services PMI, New Home Sales (big improvement expected) and Dallas Fed Manufacturing Activity (looking for a less negative print in May).

Oil prices have come off over the weekend with the Brent benchmark trading around $65 with resistance above at $66, while US cousin WTI (US Light Crude) around $59 and testing its own resistance at $60. Both benchmarks now in shallow falling channels, however, amid continuing violence in the Middle East and with OPEC production policy and the prospect of Arctic drilling adding to global supply glut concerns.

Gold back below $1200 for first time since 13 May on account of USD rally/EUR weakening rendering yellow metal safehaven more expensive for non-USD buyers. Having fallen through the major moving averages, watch for assistance around rising lows $1190 which could keep the uptrend dating back to mid-March alive. Support $1190, Resistance $1215.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Australia Consumer Confidence Deteriorated

- Japan Producer Prices Slowed markedly

See Live Macro Calendar for full data line-up, incl. consensus expectations