Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

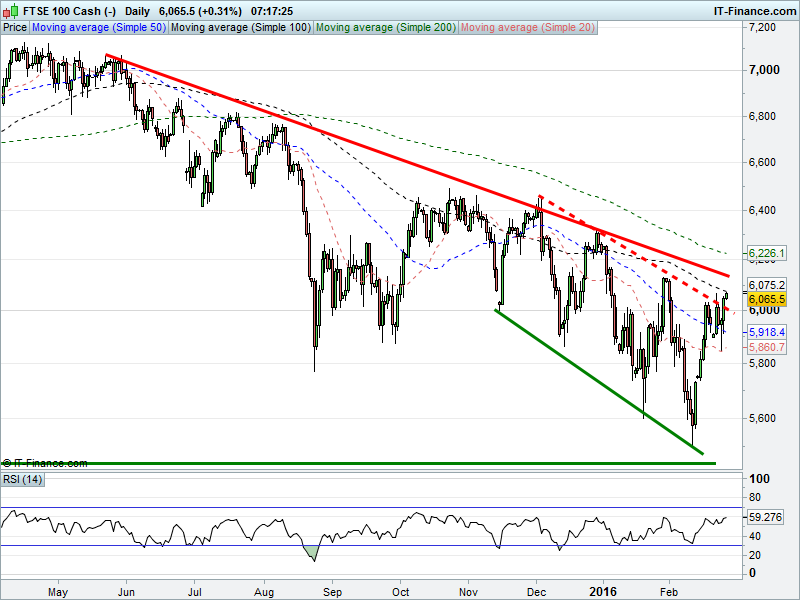

UK 100 Index called to open +55pts at 6065, in the midst of testing Monday’s highs as the rally from Wednesday’s lows extends, allowing for a tentative breakout from a 3-month downtrend, the ceiling of which has dogged the index of late. We do, however, point to the more significant hurdle in with 9-month falling resistance around 6130 which coincides with end-Jan highs. Only once this is bettered can we look further north. Watch levels: Bullish 6100, Bearish 6040

The positive opening call comes after a largely positive Asian session with investors grabbing onto the coat-tails of US gains, helped by China’s PBOC saying it sees room for further easing of monetary policy to address downside risks ahead of the G20 meeting of finance ministers to discuss global stimulus. An oil price back at technical resistance highs is also helping buoy sentiment into the end of the week, along with a small rebound in commodities prices.

Chinese and Hong Kong stocks outperforming thanks to China stimulus suggestions. Japan’s Nikkei making small advances despite the JPY breaking below 2-day rising support to hinder exporters, although traders may be focusing on the fact that currency’s Feb downtrend may have run its course. Aussie ASX underperforming (barely in the red) despite commodity price strength, potentially held back by a stronger AUD.

It now seems that simply announcing a meeting is enough to make Oil prices rally (ok, so the word oil should also still be contained in the announcement somewhere) - rebound as they did from early losses yesterday, settling up around 1%. This time it was the Venezuelan Oil Minister’s turn to suggest a March meeting had been agreed with Saudi Arabia, Russia, and Qatar. No reason to think crude will have a down day today given the blatant ignorance of fundamentals this week.

Resultant strength in crude prices lifted US equities which closed with decent sized gains. The Fed’s Bullard sought to reassure that the US central bank still has its eye on economic progress and is not aiming to raise rates without due consideration for fundamentals and data, while he did note that the risk of a global recession isn’t particularly high right now. Williams was bullish on the US economy, predicting growth of 2.25% this year with unemployment trending down and inflation moving back to 2% within 2 years. Such numbers apparently vindicating the Fed’s decision to start normalising in December ‘15.

In focus today will be French GDP expected confirmed at 0.2% QoQ and 1.3% YoY, which may be offset by annual CPI falling back to flat and still negative PPI. Spanish and German CPI may also show a worsening along with a tick back in Eurozone sentiment indicators. In the afternoon, US GDP seen slower in Q4, but personal consumption unchanged and personal income and spending improved. US GDP inflation data will be looked to for hints on US monetary policy. To close the week, US Uni of Michigan Consumer Confidence forecast slightly higher while the Baker Hughes Rig Count may well have dropped again on the low oil price pushing players out of the game.

Gold is apparently still benefiting from safe haven demand (the same safe haven demand that’s pushing up equity markets?!) although selling looks to be kicking in above $1240, limiting upside. Note a likely risk-on Friday...

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Rightmove say FY underlying operating profit rise 16%

- Engineering firm IMI begins restructuring Swiss ops

- RBS posts full – year loss of $2.75 billion

- Riverstone Energy says chairman of board to leave

- Intu Properties FY net rental income rise 7.8 pct

- William Hill announces share buyback, hikes dividend

- Spain's Telefonica sees revenue growth of 4 percent this year

- Pearson sees profit recovery in 2018