Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

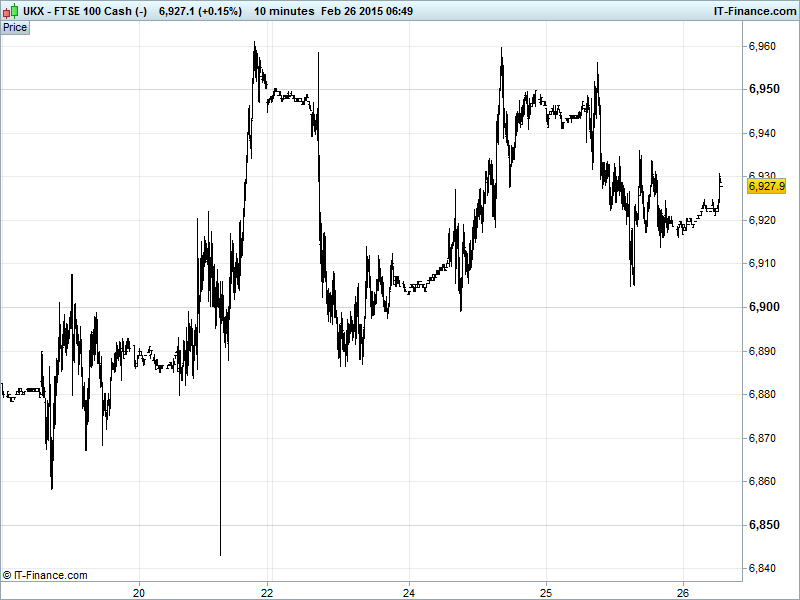

UK 100 called to open -5pts at 6930, finding support overnight around the 6920 level which maintains the acceleration in February’s rising trend via steeper rising lows since 19 Feb while the index attempts to make a decisive test and break above the for-so-long elusive 99/00 highs of 6950. We look for the index to make another test of recent highs today with support likely around 6900. Watch levels: Bullish 6980, Bearish 6860.

The negative open comes as European stocks take a break from yesterday’s probing of record highs as Greek finance minister Varoufakis said that while the indebted nation has no immediate problem with government liquidity, it will have difficulties making debt payments to the IMF and ECB in the spring and summer. Ratings agency Fitch sees recent Greek news as positive but uncertainties remain around sovereign and bank financing.

Elsewhere, the ECB chief economist, Praet, commented that Eurozone QE has been a net benefit to the economy, with the risks associated with deflation worse than those of QE itself, while Fitch said European credit investors are wary of deflation, but still sceptical about the benefits of the ECB’s stimulus measures. Note Draghi emphasising QE will continue until inflation recovers but monetary policy can’t create growth without accompanying structural reforms.

US markets finished largely flat on Wednesday with Yellen repeating in her second day of testimony to U.S. lawmakers that inflation and wage growth remain too low to warrant a rate rise at the next meeting, calming the nerves of those observing the patient-impatient tug of war while traders remained on the sidelines.

Asian bourses were mixed at close of play, tracking cues from Wall St. and with a lack of fresh drivers. In Japan, the BoJ’s Kuroda said that economic growth is fragile but on track, helping the markets to a positive close. Reports from China suggested a possible rate cut in 2015, but with no cut planned for the near term, and Australia’s ASX was down 0.6% following worse than expected Q4 Business CAPEX showing a pull-back of 2.2% after a modest rise in Q3.

In focus will be a whole lot of data from Europe and the US. We have German unemployment, UK GDP, Eurozone industrial and consumer confidence and US durable goods orders and inflation data. Consensus is mixed but generally quiet, with no big surprises expected. Also of note are the speeches with the BoJ, ECB, BoE and US Fed representing today.

Oil holding strong gains, despite US EIA inventories surging for seventh successive week (still at 80yr highs). Markets more focused on drops in US diesel/gasoline stocks (cold weather) which suggests a pick-up in demand, along with slower US production growth, better Chinese PMI manufacturing and demand signals from Saudi Arabia countering recent global supply glut concerns. Note Brent ($61.4) back up around recent highs holding mid-Jan uptrend, and US Light Crude ($50.7) holding February sideways shift.

Gold ($1210) continues its bounce from recent lows, back above the trend line of rising support from early November and potentially testing an exit of its 2-month down channel. Watch for resistance at 100-day MA $1214. Help from a weaker USD following Fed chair Yellen’s testimony (‘patience’, ‘rate rise when inflation on track’) and some signs of rising demand from China.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Aussie Private Capital Expenditure Miss, contraction

- Germany GFK Consumer Confidence Beat, improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Interserve Chairman to step down by 2016

- Domino's Pizza year underlying profit up 15.1 pct

- RBS makes $5.4 bln loss after taking hit on value of U.S. business

- RBS says sells $36 bn U.S. loan portfolio to Mizuho

- UK finance minister tells new RBS chairman bank must stay backmarker on pay

- UK's Phoenix Group says chairman to step down to join RBS

- CRH FY earnings up 11 pct as US recovery gains momentum

- Reed Elsevier FY underlying adjusted operating profit rises to 2.16 bln euros

- Gulf Keystone receives $26 mln payment for Shaikan crude sales

- Reed plans 500 mln stg buyback, simplifying structure

- Colt Group SA FY revenue fell 5.1 percent to 1.5 billion eur

- Merlin Entertainments sees another year of growth in 2015

- Capita posts 14 percent rise in full – year revenue

- British American Tobacco sales fall slightly smaller than expected

- Kenmare Resources says to deliver 2015 budget on Mar 31

- Exillon Energy Jan average daily production was 16,945 bbl/day

- Britain's National Express looks to expand in North America

- Copper miner Kaz Minerals posts annual profit slightly ahead of forecasts

- RSA swings into profit in 2014, restarts dividend

- Chemical maker Synthomer's underlying pretax profit falls

- Jupiter posts FY profits beat, to pay special dividend

- Howden Joinery says to return 70 mln stg to shareholders

- Premier Oil scraps dividend as it swings to 2014 loss

- Telecoms provider Colt's profit hurt by lower voice revenue

- Capital & Counties Properties FY adj EPRA up 25 pct

- Reed plans 500 mln stg buyback, simplifying structure