Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

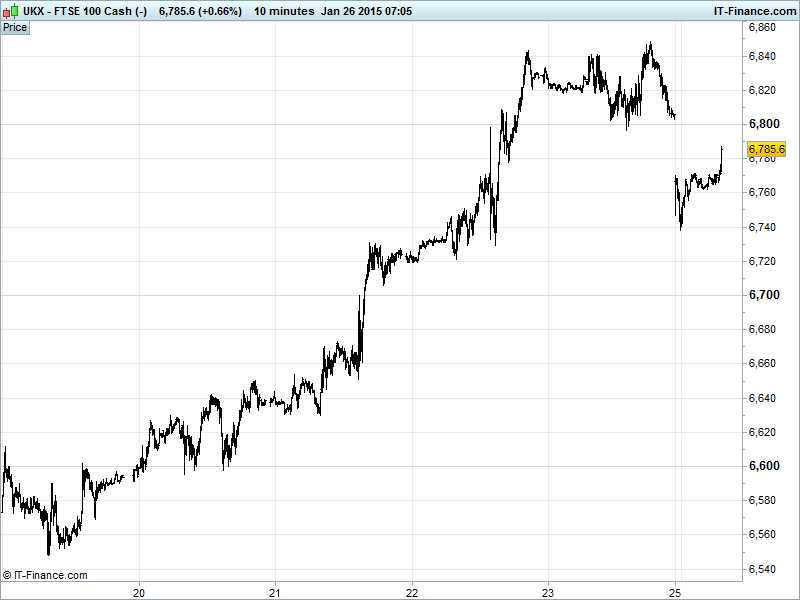

UK 100 Index called to open -45pts at 6785, having fallen back from 4-month highs 6850 to find support around 6750 giving hope that Nov/Dec highs 6775 can become a base for further gains and a challenge can still be made on Sept/2014 highs 6905. Uptrend still intact via rising lows from 19 Jan. Updated Watch levels: Bullish 6860, Bearish 6730.

The negative open stems from Greek national election results showing a sweeping victory for anti-austerity party Syriza. While this generates uncertainty based on strong desire to leave behind austerity and renegotiate/abandon current Trioika bailout conditions, as well as empower populist movements elsewhere in Europe, a slightly softer party rhetoric of late means losses are considered not as bad as they might have been.

US markets were mixed following Thursday’s ECB QE-induced gains with uncertainty creeping back in and focus turning to the risk involved with the weekend’s Greek election and after disappointing Chicago Fed, PMI Manufacturing and Existing Home Sales along with a mixed bag in terms of corporate results (McDonalds, BoNY Mellon, General Electric).

Plenty of ECB talk at the weekend with Visco saying there is risk of deflation and ECB QE will favour countries which have made structural reforms, while Coeure said ECB can’t do everything for Europe and Weidmann doubts QE will work. Note the EUR/USD at a fresh 11yr low. The BoE Governor Carney also said it is appropriate to look through the effects of lower oil price when wages are growing and expects gradual rate rises of the next three years.

Asian markets lower (Australia closed) following Greek election result where it is just shy (2 points) of a majority but expects to form a coalition by Wednesday, maybe even already done, setting the stage for tough Troika negotiations which could see the country excluded from ECB QE and ultimately even lead to a Greek exit from the single currency Euro.

In focus today we have the fallout from the Greek election which could well last for a few days. Data-wise, watch out for German IFO Surveys with small improvements expected in January. UK BBA Home Loans are seen flat adding to worries of the UK housing market topping out while the Dallas Fed Manufacturing Index is forecast to fall back as the Chicago print did on Friday.

Gold holding up just shy of five-month highs $1300, although unable to make progress due to the stronger USD (product of weaker EUR following ECB QE announcement, less pressure from petro-dollar selling, and prospect of a US rate rise), even if safehaven demand buoyed by uncertainty related to global growth concerns and the Greek election result.

Oil shows US Light Crude taking another leg to test mid-month lows $44.7 although Brent is holding around recent lows $48. Just. Uncertainty about global growth still rife after Greek election result and passing of Saudi King as well as huge US inventory builds last week emphasising global supply glut.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan Trade Data Beat, improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Aer Lingus says considering new bid from BA-owner

- UK energy supplier SSE to cut gas tariffs from April 30

- Balfour Beatty awarded 120 mln stg student accommodation project

- Vodafone and Docomo Pacific sign marketing deal in Guam, CNMI

- SThree full-year profit rises as global companies raise hiring

- Aveva Group warns on trading in energy equipment unit

- Rolls-Royce holdings receives 100 mln euro order for MTU engines