Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

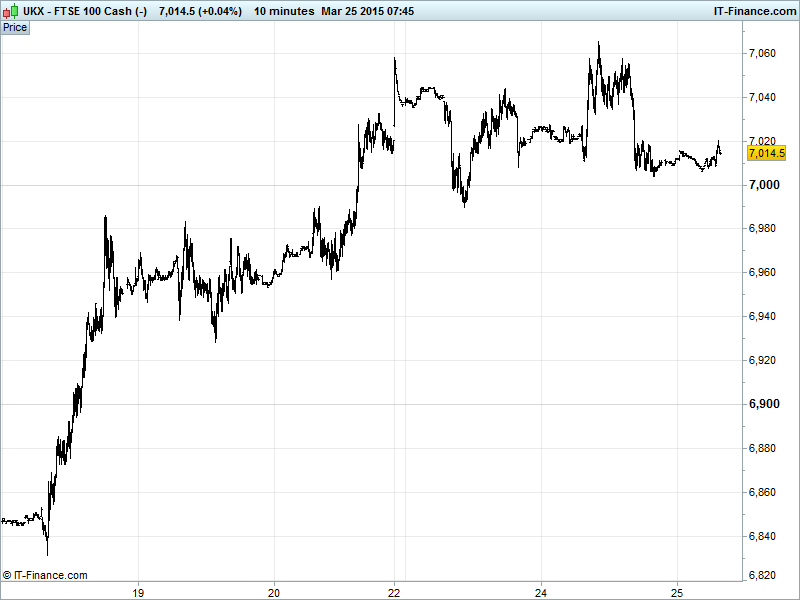

UK 100 called to open -5pts at 7015, back from another all-time high of 7065 yesterday but still holding up above the key 7000 mark which will be eyed for whether it will serve as a platform for both consolidation of recent 5.4% gains as well further upside now that the index has finally managed to test clear water. Watch levels: Bullish 7075, Bearish 6980.

The tepid opening call comes as Asian equities drifted overnight after US markets came under pressure from economic data (housing, inflation, PMI) bolstering prospects of higher US interest rates and uncertainty over the strong USD impact on exports. Also weighing is continued apprehension about a slowing China and an FT report suggesting the ECB wanting to prohibit Greek lenders from buying more short-term government debt, in effect removing a key funding source for Athens and adding to fears of a cash crunch and default.

Note however, M&A news boosting sentiment with Hutchison Whampoa striking a £10.25bn deal for Telefonica’s UK mobile network O2 and suggestions that Brazil’s 3G Capital is in advanced talks to acquire Kraft for $40bn hoping to merge it with Heinz.

US stocks pulled back on Tuesday to close lower, partly due to renewed concerns about interest rates – upbeat housing data, consumer price inflation up for the first time in 4 months and positive manufacturing PMI showing growth and supporting US Fed Hawks. The US Dollar Basket is back down below 9800 on renewed Fed patience, but remains strong on yesterday's data.

Asian markets have been mixed overnight, as usual following strong cues from the world’s #1 economy (the US). In China the PBoC said it will be prudent with monetary policy which will have done little to avail the China Slowdown fears. This added to the downwards pressure from yesterday’s disappointing manufacturing PMI to push the Shanghai Composite down. In Japan, BoJ Deputy Governor Iwata said it was hard to achieve 2% inflation within the 2-year deadline set by the central bank, but added that deflation will soon turn to inflation and the broader uptrend in prices will benefit the transition.

Australia’s ASX outperformed its peers in Asia, trading flat around its highest level in 7 years helped by mining stocks benefiting from a rebound in iron ore prices, and this despite key trading partner China’s economy seemingly wallowing in the doldrums of late.

In focus today will be the German business surveys all looking for upbeat prognoses, with US durable goods orders (not including highly volatile transport sector orders) looking for an improvement to back up yesterday’s positive data with indications that businesses are, on the whole, buying more things. EIA weekly oil stocks round off the bill on a fairly quiet day data-wise.

US Light crude ($47.1) and Brent ($54.8) both back from 10-day highs despite a weaker USD as investors begin to look towards this week’s EIA US stockpile data which is expected to show another rise, and even more than yesterday’s API reading of +4.8m barrels.

Inventory data remains key in gauging global oversupply as OPEC refuses to cut production to defend market share and the US tracks back on expensive operations in light of the oil price decline. Both benchmarks in uptrends from 18 Mar, although the latter already testing rising support after poor China manufacturing, Saudi/OPEC stubbornness and uncertainty on supply from Iran amid nuclear talks.

Gold ($1189) managed a brief test of $1195 thanks to the weaker USD and jitters related to Greece and China and the tragic air accident in France but failed to maintain its recent winning run as investors continue to weigh up the likelihood and timing of higher US interest rates in light of incoming macro data. As expected late Feb lows served as some resistance. Now watch for whether yesterday’s low of $1185 act as support.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Westpac-MNI Consumer Sentiment Improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Suit specialist Moss Bros' profit rises 9%

- AstraZeneca to collaborate with Harvard Stem Cell Institute on diabetes research

- Card Factory says full-year profit rises 8.9%

- AA says FY revenues up 1% to £983.5m

- AA to raise £200m of equity as part of £935m refinancing

- Johnston Press says FY underlying revenue drops 4.4%

- Johnston Press signs new print contract

- Stagecoach's south west train franchise gets investment ramp – up

- Airbus sells further 15% stake in Dassault Aviation

- IP Group says U.S. FDA grants portfolio co's Chronocort orphan drug designation

- Topps Tiles posts 5.2% first half sales rise

- Monitise appoints Telefonica, Santander backed Shurrock as non-exec director

- Chime Communications 2014 EPS rises 12%

- Bellway ups dividend after first-half profit rise

- Fastjet says receives air service permit from Zimbabwe

- United Utilities expects modest 2014/15 profit rise

- Moneysupermarket share sale priced, offer size revised –source

- London Capital Group says Charles-Henri Sabet will assume role of CEO

- Balfour Beatty suspends dividend, posts loss of £59m

- Anglo Pacific posts FY pretax loss of £42.4m

- Hilton Food full-year pretax profit rises 1.3%

- Pendragon buys dealership in California for $48.5m

- London Capital Group FY revenue from continental operationss falls 10%

- Petroceltic, Hess to withdraw from Dinarta licence

- OneSavings Bank completes purchase of UK mortgages portfolio

- TUI Group confident on hitting profit growth target