Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

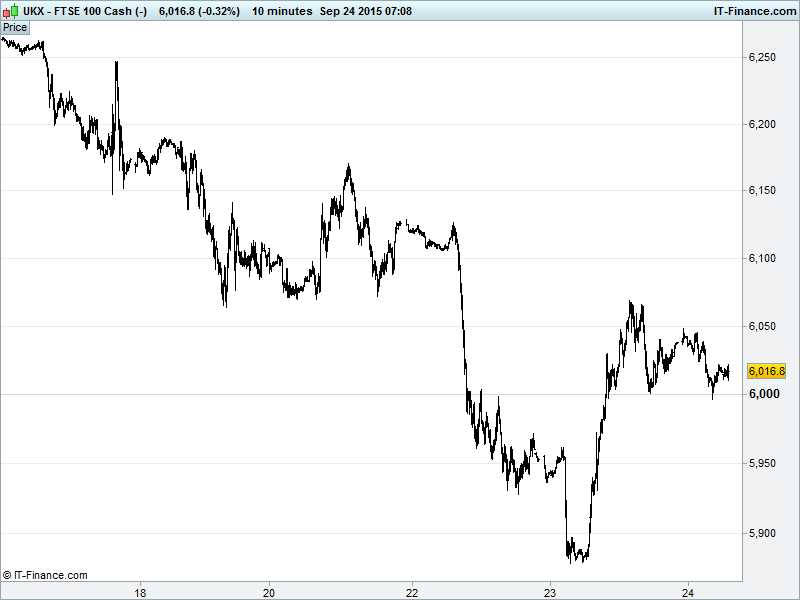

UK 100 Index called to open -10pts at 6020 with bulls happy to see it holding above 6000 and twice finding support after yesterday’s break back above. The bounce from 5900 keeps us in a sideways 1-month channel and we note potential for a break above 6050 falling highs to deliver a bullish flag pattern with upside to 6175. Although beware potential hindrance from falling highs from 17 Sept. Updated watch levels: Bullish 6040, Bearish 5985.

The negative opening call comes after a disappointing preliminary PMI Manufacturing read for Japan, both missing expectations and giving up ground from August after a sharp drop in export orders attributed to weak demand from China. This adds to China’s own poor PMI report yesterday and to the existing global growth woes which saw the Fed hold rates. What will Fed Chair Yellen have to say about that tonight? Any update on thinking over the last week?

Asian markets mixed overnight, with Japan’s return from a 3-day holiday seeing it play catch-up with global peer bourse losses this week. A stable JPY despite safehaven seeking should have helped, but a poor PMI, a first-half profits warning from electronics maker Sharp and car makers getting their first chance to react to the VW emissions-gate story have held the index back strongly.

Australia’s ASX is the regional outperformer as shares rally from below 5000, the lowest level in over 2 years, after a European recovery included strong performance by the battered miners. Note China positive, and talk of rout cooling on reduced leverage trading, although Hong Kong’s Hang Seng negative for a fourth day, hurt by energy and financials on fears of China slowdown.

US markets still under pressure after a negative close on Wednesday. (Dow, S&P and Nasdaq all paring early losses to close down less than 1% each, but down nonetheless for 4 out of the previous 5 sessions). US interest rate chatter continued in much the same vein as it has been for the past month: Atlanta Fed governor Lockhart repeating his view that rates will rise this year while putting last week’s decision to hold off down to simple post-crisis caution. This in contrast to ECB President Mario Draghi who sought to reassure European markets that the ECB will not hesitate to act dovishly should the need arise, while ECB peer Weidmann suggested the ECB should look past oil price induced deflationary pressures.

In focus today we have German IFO Business Surveys seen falling slightly. ‘Volatile’ US Durable Goods Orders are expected to post deterioration in August after a strong June and July, although the core reading should hold up around breakeven. The Chicago Fed Nat Activity Index is forecast to drop, but the Kansas City Manuf Activity improve and New Home Sales deliver further improvement towards May highs. As mentioned the Fed’s Yellen speaks tonight.

Crude prices staged a lacklustre bounce off support at rising lows from mid-Sept after Chinese President Xi Jinping signalled a willingness to open up to more foreign investment, that bounce losing momentum quickly (this is China, after all) with Brent ($48) re-testing its support and WTI ($44) failing to make it above $45 overnight.

Gold ($1135) back up on both safe-haven and physical demand as talk of US monetary policy still dominates and the USD basket comes back from another test of Sept highs in a potential bearish saucer top formation (15-min chart) that could signal further downside today, which could prove bullish for the yellow metal.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- National Grid North America to raise £350m of new debt financing

- CRH names Towe as chairman of America operations

- Range Resources updates on Trinidad operations

- Alliance Trust appoints Samuel, Sternberg as non – executive directors

- Poundland says to raise £50m via share placing

- Micro Focus Intl says trading in line with expectations

- Euromoney sees FY adjusted pretax profit of no less than £107m

- WS Atkins sees first half results in line, outlook remains positive

- Air Partner HY underlying profit doubles

- Thomas Cook sticks with forecast for growth

- SVG Capital's H1 NAV +3% to 606p

- Daily Mail & General Trust PLC Pre-Close Trading Update