Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

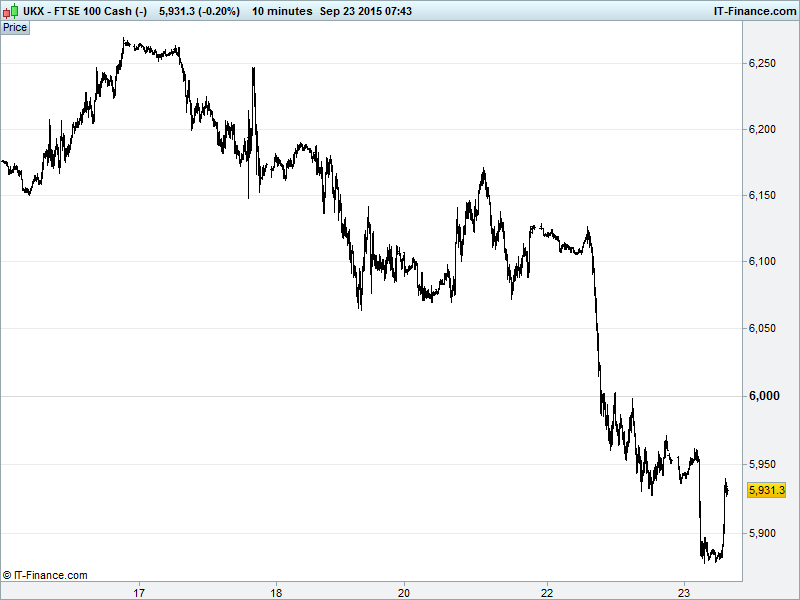

UK 100 Index called to open flat at 5935 having recovered from a probe below 5900 overnight which itself followed a sharp break below September lows 5985 yesterday. While still above Aug 24 and 2015 lows of 5770 the uptrend and rising lows from Aug 25 are now off the table. The drop also maintains the downtrend from April which accelerated in August. Support around Aug 25 lows 5890 is helping deliver a semblance of a bounce. More possible, or full retrace to 5770 for a genuine double-bottom rebound? watch levels: Bullish 6005, Bearish 5870.

The flat opening call comes despite China's unofficial Caixin PMI Manufacturing for September falling to a 6.5yr low of 47.0 and thus remaining safely in contraction territory. This will just serve as affirmation of a troubled and slowing China and support the Fed's decision to hold interest rates at historic lows based on concerns related to growth in China, Emerging markets and globally. The official fig (also in contraction in Aug) are out next week which could see sentiment held back until then.

Asian stocks suffering on the China PMI news (although Japan still closed) with Chinese and Australian bourses down around 2% as the commodities space continues to remain under pressure from the USD recovery and now confirmed global growth worries. Note Copper back down around $5000/ton. While Japan remains closed, Nikkei futures are hindered by safehaven seeking in the JPY which will is sure to hurt exporters on their return.

US markets sold off heavily yesterday to close really quite red as the prospect of imminent cold turkey for the global economy weighed heavily on investor sentiment. Cheap money for a while longer, yes, but for how much longer exactly? Even embattled emerging markets urging the Fed to get on with policy tightening may be pushing the US central bank to pull the plug before the end of 2015. While EM arguably have nowt to lose, developed economies may be walking a knife-edged ridge according to many economists (including Nobel laureate Robert Schiller), leading many to flee into safe havens.

The IMF's Lagarde has warned that downside risks to global economic growth have increased including low commodity prices (she means deflation) and monetary policy realignment from China (adjusting to new normal of slower growth). This adds to existing messages of caution being delivered by all and sundry, despite reassurances from China's US state visit about reforms, no FX manipulation and growth rate just 'fine and dandy'.

In focus today we have Eurozone PMI Manufacturing and Services figures which are seen showing the Eurozone faring well, Germany very well, but France mixed (services strong, Manufacturing still contracting). The US PMI Manufacturing figure is also seen firm in the afternoon. Note ECB President Draghi speaking in the afternoon, which will be interesting given the talk of more stimulus after the Fed held fire, followed by Bundesbank head and ECB official Weidmann and the Fed's Lockhart again (already said hike in 2015).

Crude prices staging a minor recovery this morning having lost a dollar or two overnight following some more disappointing Chinese manufacturing data with the usual implications of stifled demand from the world’s #2 oil consumer. However, broader economic indicators aren’t quite as bearish according to Capital Economics. Brent ($49.2) now back above Sept falling highs and looking for a break above $49.5, WTI ($46) still heading up towards its own falling resistance line around $46.6.

Gold ($1125) still struggling despite a widespread flight into safe havens sparked by another equity markets sell-off. Investors still preferring interest bearing US treasuries with the prospect of higher returns in the near future. Note the US Dollar basket almost back at early Sept highs while continuing to languish in what looks a YTD bearish triangle formation.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Smiths Group Full-Year Net Profit Rises Despite Lower Sales

- Smiths Group's CEO Philip Bowman to step down

- BBA Aviation proposes to acquire Landmark Aviation for $2.06bn

- United Utilities: 1H Profit Will be Hit by Compensation Claims But Trading in Line With Views

- Diageo Sees £150M FY Impact From Currency Movements

- Premier Oil Backs FY Capex View, Sees Significant Reduction In 2016