Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

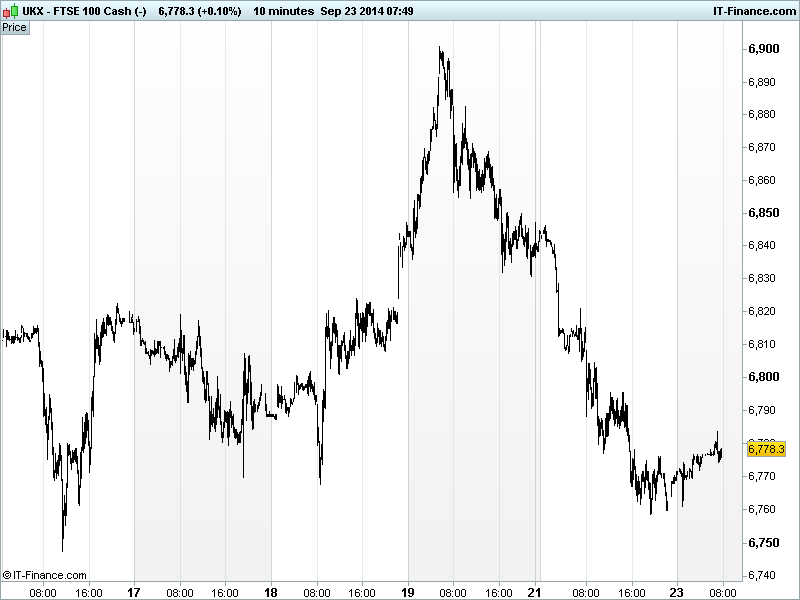

UK 100 called to open +5pts at 6780 having found support overnight just above 6750 thanks to the HSBC China PMI Manufacturing delivering a small helping of good news by beating consensus, staying above 50 and improving from last month to a 2-month high.

This follows a weak session yesterday as China growth jitters intensified, macro data failed to inspire on either side of the Atlantic, ECB President Draghi warned on the Eurozone losing recovery momentum with risks to the downside and the woes of Tesco all weighed on the index.

US markets closed in the red as investors worried about a slowing Chinese economy and weak domestic data with small-caps leading the way, while geopolitical concerns resurfaced amid reports of fresh air-strikes on the Islamic State in Syria. Ukraine is however preparing to withdraw artillery from the East as truce violations fail to disrupt plans for a settlement with Russia.

While manufacturing activity rose in September suggesting conditions held up better than expected, with strong growth in new orders/exports and steady retail/services, fears over a slowing China hold true and cannot be ignored, with the key employment component continuing to decline to a 5½ yr low and the China Beige Book also still struggling in Q3.

At a time when investors are looking to China to give global growth a push the news is welcome, but with the data focused on smaller, private companies, all eyes will be on the official PMI reading, due 1 Oct, which focuses more on large, state-owned companies

Stocks in Asia are back in positive territory (Japan closed) after a negative lead from the US, reversing some of yesterday’s weakness with Australia leading the way as metal prices such as Copper and miners recover on the better China data and USD Index pulling back a little on AUD strength as risk aversion calmed.

The UK 100 index has found support around September lows of 6760, which could help provide the foundations for another rally, but catalysts are needed for a return to recent highs of 6900 and a break back above the 100-day moving average would be welcomed. European PMIs today? QE hints from Draghi?

In focus today, we have French GDP seen confirmed flat in Q2, while preliminary PMI Manufacturing and Services readings are expected to remain weak and around breakeven respectively. German PMIs seen pulling back ever so slightly, meaning similar expectations for the Eurozone.

In the afternoon, US House Prices seen growing at a similar pace in July while consensus puts US PMI Manufacturing higher in September, joining China although the Richmond Fed is forecast lower in September echoing the Chicago reading yesterday,

In commodities, Gold is holding above its latest 8-month low ($1208) albeit still in a downtrend from March, while traders assess the health of the global economy, the path for US monetary policy and the outlook for physical demand. Having rallied as high as $1220 overnight to match yesterday’s highs, it has fallen back to support at $1217, just above a trendline of rising support from early on Monday morning.

In Oil, both US Light and Brent crude have seen a small bounce thanks to the China manufacturing gauge beating expectations, improving the demand output for the black stuff from the world’s #2 economy

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- CN HSBC PMI Manufacturing Index Beat, improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- PZ Cussons says impact of Ebola outbreak has been relatively small in Nigeria

- Miller Homes to float on London Stock Exchange

- Faroe Petroleum reports first half loss after tax of 3.7 mln stg

- Luxury shoe brand Jimmy Choo to float on London Stock Exchange

- Motoring group AA posts maiden H1 operating profit down 11.7 pct

- UK's IMI appoints Daniel Shook as finance director

- Close Brothers full-year operating profit jumps 20 pc

- Panmure Gordon first-half pretax profit from cont ops rises