Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

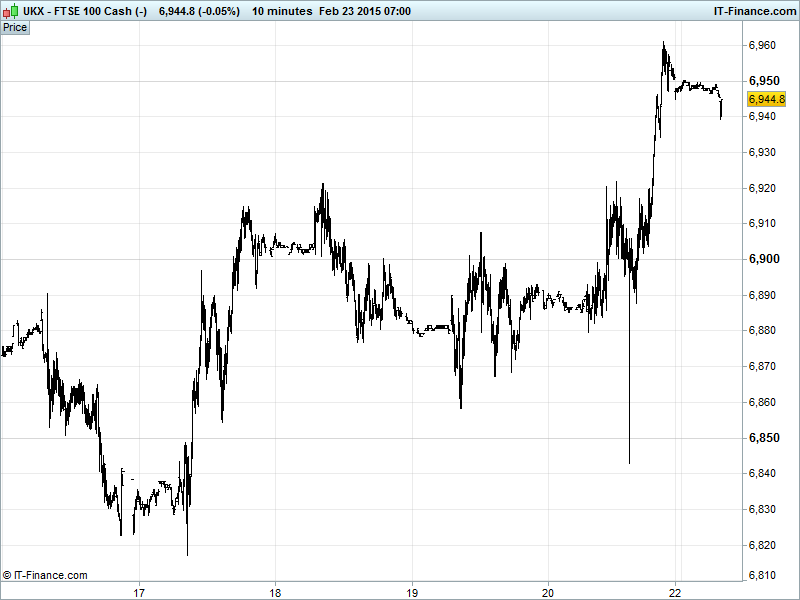

UK 100 called to open +25pts at 6940 this morning, having made it as high as 6961 on Friday night to post a new all-time intraday high for the UK flagship index. Back from the highs, all eyes on whether the breakout at 6920 can prove supportive should weakness creep in. Also of interest, now the level has finally been tested, will be whether we can stay above prior-all-time highs of 6950 which had proved so elusive for so long, harking back to the turn of the millennium. Being able to stay above would allow the UK Index to join global peers. Watch levels: Bullish 6970, Bearish 6910

The positive open comes after news late Friday that Greece and the Eurogroup have reached a tentative agreement for an extension of its bailout for four months. The deal calls for Greek and European officials to agree to a series of reforms by the end of April with Greece due to present a first list of reform measures, still subject to validation by the International Monetary Fund, the European Central Bank and the European Commission, today. Finance minister Varoufakis has said that the deal is a ‘small step in a new direction’ while European finance chiefs will decide this week whether the proposals go far enough, or necessitate another round of emergency negotiations.

US bourses rallied on Friday afternoon and closed with moderate gains following the news from Europe and confidence was up on the perceived attitudes of all involved – Eurogroup head Djisselbloem said that Greek bank recapitalisation would remain for the four month extension while PM Tsipras is ‘committed’ to honouring Greece’s obligations. In other US news, the Fed’s Bullard and Plosser were increasingly hawkish on Friday, both indicating that last week’s most watched key-word, patient, was indeed likely to be dropped from the March minutes which would pave the way for a possible rate rise in June. This came after the positive US employment report which itself came after the surprisingly dovish January minutes.

Asian markets were mostly higher, buoyed by the gains on Wall Street and the above European news. In Japan the stock market is advancing on the back of the BoJ’s satisfaction with the pace of its economic recovery, with the Nikkei having touched fresh 15-year highs last week. Governor Kuroda conceded that the inflation target of 2% was likely to be missed due to tumbling energy prices, however inflation is increasing and the target is likely to be hit in fiscal year 2015. The Australian ASX ended Friday up 0.5%, while key trading partner China remains in holiday mode for Lunar New Year until Wednesday.

In focus today we have German IFO data at 09:00 with improvements expected in Germany’s business climate, followed by an interesting round of US sales data (mixed consensus) which will be particularly interesting to watch amidst the US Fed rate rise issue.

Oil shows US Light crude ($50.6) back around its trend-line of Feb rising support at $50 despite the US Baker Hughes Rig Count posting another weekly drop in the number of active installations. The drop was the smallest in seven weeks, and markets seem to be realising that real changes in US output are likely be slow. The nation is still sitting on record stockpiles according to last week’s EIA and API data. Brent Crude ($60) holding around Friday’s levels, still in a Feb uptrend (steeper than that of US Light) and close to recovery highs of $63 buoyed by Middle East uncertainty (Libya output, OPEC etc.).

Gold ($1203) made another test of $1200 on Friday night as a Greek deal dented safe haven demand. While we have bounced back, progress is limited, hovering around recent levels with the metal still in a down channel from 22 Jan, still technically testing the 4.5 month trend line of rising lows as trade is muted by Chinese holidays and conflicting drivers hindering demand for the safe port in a storm (strong USD, equities trading highs, decent global macro data, Greek progress vs Greece’s tough outlook). Note The Fed’s Yellen testifying this week with markets looking for fresh clues on rate rise timing that could move the USD.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Premier Oil abandons Kenyan onshore oil well

- Bovis Homes full – year pretax profit up 69 pct

- UK government's stake in Lloyds falls below 24 percent

- Quindell says talks progressing with Slater & Gordon

- Wincanton says Magnet renews home delivery and transport contract

- Keller Group wins contract for Koralm railway line between Graz and Klagenfurt

- Old Mutual says Nedbank Group to buy back 1.79% of shares currently in issue

- DFS sets listing price range at 245 – 310 pence per share

- AB Foods maintains year earnings guidance

- APR Energy says in talks with lenders

- DS Smith proposes to acquire Duropack for 300 mln euros

- XP Power says FY pretax profit rises to 24.3 mln stg

- Balfour Beatty JV wins 270 mln stg building deal in Hong Kong

- Dechra Pharmaceuticals says H1 group revenue up 5.2 pct

- SeaEnergy says BP accelerates contract with Return to Scene

- Britain raises 500 mln stg through sale of Lloyds shares