Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

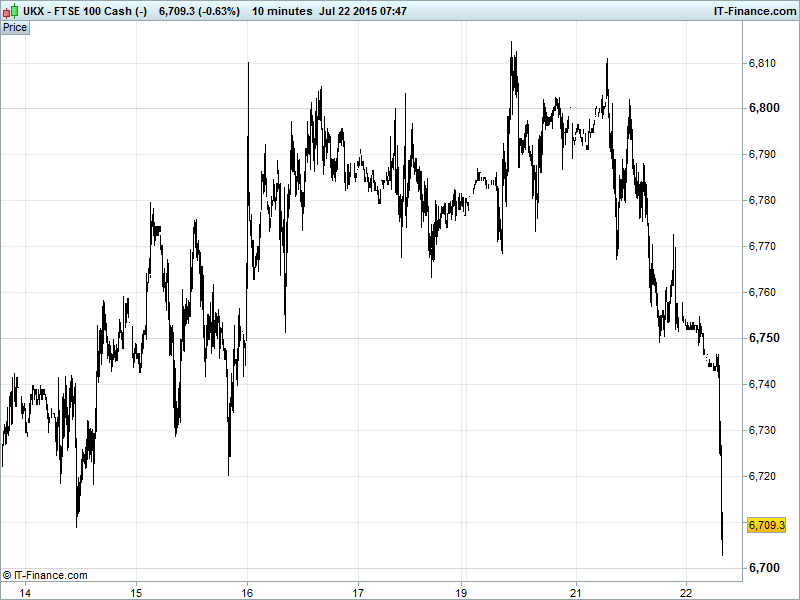

UK 100 Index called to open -60pts at 6710, having fallen back following a struggle at 6800 to break below the 200-day moving average 6750 and trade around last Wednesday’s lows. Is this the pullback before the uptrend resumes? The longer term rising trend is still intact after all. Or is this the start of a more significant correction back towards recent lows 6400? Updated Watch levels: Bullish 6760, Bearish 6705.

The negative opening call comes after Asia followed US futures lower following disappointing quarterly updates from US tech behemoths Apple, Microsoft and Yahoo! This after US bourses closed in the red following a weak European session soured by some poor US earnings reports and macro-growth/central bank uncertainty.

Note the USD Index retreating from recent highs has failed to offer any support to the current commodities rout while an S&P upgrade for Greece following bailout progress, bridge loan and debt repayments and has had little effect. It’s all about earnings season. The strong USD is not proving quite the hindrance that many had expected, but this doesn't mean all is rosy.

Apple Q3 revenues, gross margin and profits beat estimates, but 47.5m iPhones sold missed 49m consensus and the outlook was nothing to text home about. While Microsoft results also beat at the top and bottom line, a Nokia restructuring charge and low core product demand weighed. Yahoo! (YHOO) sales beat but profits missed estimates and guidance was below consensus.

Asian bourses lower overnight with a weak lead from Wall St. (disappointing corporate earnings from United Technologies and Apple) leading to profit taking after several straight sessions of gains for Japan’s Nikkei and a volatile July comeback by China’s Shanghai Composite, which could be about to succumb to a resumption of its 6-week selloff.

Aussie central bank governor Stevens said that further rate cuts are not off the table while cautioning about the longer term issues (excessive risk taking, over borrowing) with further easing. Non-mining capex is expected to pick up in H2 while the Aussie Dollar appears to be adjusting itself lower without external assistance at the moment which is having an expansionary impact on the economy, but a benign outlook for inflation (latest CPI print missed expectations) following 2 interest rate cuts this year makes further RBA action possible.

In focus today will be results from American Express (AXP), Boeing (BA), Coca-Cola (KO), Texas Instruments (TXN) and Whirlpool (WHR) while we have US housing data in the afternoon. In terms of Greece, lawmakers are back in parliament to vote on further bailout reforms, while the latest Bank of England minutes will provide an update on UK rate rise thoughts.

Crude prices remain in a medium term downtrend with prices weighed on by reports of a surprise rise in US inventories (API data, to be officially confirmed today). USD strength abated on Tuesday to support commodities, however, providing some respite for under-pressure oil prices. China demand also showing no signs of falling with seaborne volumes headed for the world’s #1 commodities consumer remaining high. US light largely unchanged from yesterday at $50 while Brent holding up around $56.

Gold ($1096) trending down again since Tuesday lunchtime amid the longest rout since 1996 for the yellow metal. Goldman Sachs’ predictions of further losses duly coming to fruition as ETF holdings also contract with US Fed rate hike preparations putting investors off bullion. Now in a falling channel with $1098 a key target to the upside before a potential pullback towards $1092 and below.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- AstraZeneca drug selumetinib fails in uveal melanoma trial

- Silver miner Fresnillo raises gold production outlook

- BHP beats fiscal 2015 iron ore guidance, takes copper hit

- Kier gets smart motorways contract from Highways England

- Fenner sees FY earnings slightly below previous management expectations

- Bill payment services provider PayPoint's Q1 revenue falls 2 pct

- Chip designer ARM posts Q2 profit rise on robust royalties

- Flybe Group says remain focused on tackling surplus E195 aircraft

- Johnson Matthey promises investor return as Q1 profits edge down

- easyJet guides to FY profit growth of 7 – 14 percent

- Euromoney Institutional's Q3 headline revenue falls 1 pct to 105.4 mln stg

- TalkTalk on track for full – year, earnings H2 weighted

- Costain Group wins smart motorway contracts by Highways England

- Gemfields says exploration planned for next few years at Montepuez ruby mine

- Carillion J/V wins 475 mln stg UK motorway contracts

- Land Securities to pay interim dividend of 8.15 pence per share

- Sage says on course for full – year guidance

- Pub firm Marston's says Q3 trading meets expectations