Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

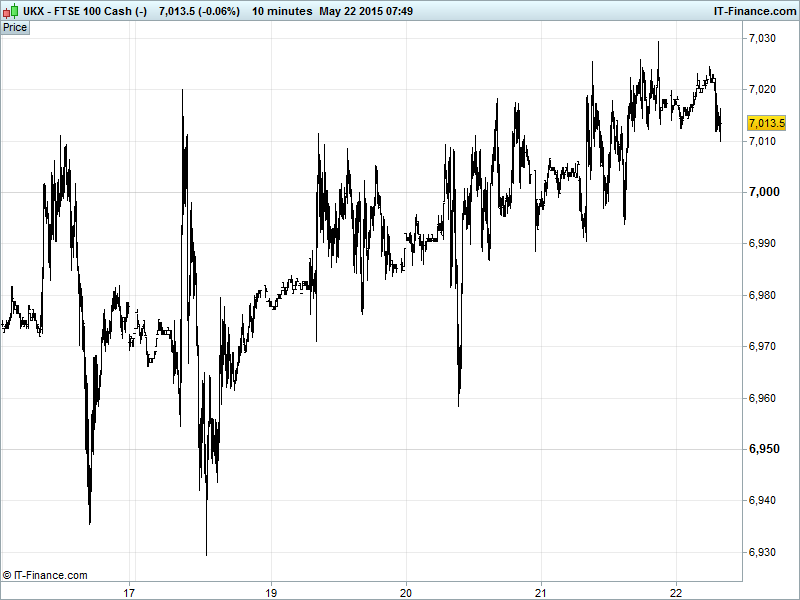

UK 100 Index called to open flat at 7015, holding its uptrend from May 7, still trying to engineer a decisive breakout above the week’s 7020-7030 ceiling in order to challenge April’s falling highs 7060 before revisiting recent/all-time highs 7088 and 7127. The 1-week bullish ascending triangle pattern is still valid (just) but we may be getting too close to the apex. Watch levels: Bullish 7035, Bearish 6975.

The tepid opening call comes amid mixed news from the global markets with US equities advancing Thursday, China’s leading index advancing in April and the BoJ keeping its super-QE programme in place following observations that the Japanese economy is continuing to recover slowly. Negatives closer to home kept the UK 100 from making progress as Greek bailout talks broke up in Riga with little if any progress made and earlier optimism largely forgotten about. Still, they’ve got ‘til the end of the month….

US bourses closed with moderate gains (although the hitherto unstoppable S&P500 made another new record…) as recovering oil prices boosted energy stocks, and after some mildly encouraging, yet mostly disappointing, macro data. Encouragement will of course stem not from the data itself, but from the diminished prospect of an imminent Fed rate hike, which looks well off the cards in June, keeping the money supply cheap for the time being. All eyes will be on Fed chair Yellen’s speech today at 6pm GMT ahead of the long weekend.

Asian equities taking the positive lead from Wall Street (more record highs) as weak US economic data appeases low-rate-lovers’ fears of any imminent Fed rate rise which would confirm the beginning of the end of an era of excessively loose equity-boosting monetary policy. Comments from ECB President Draghi (speaking again at 9am) about below-growth potential but a recently improved environment are also all the while we patiently await concrete progress on Greek debt talks which are unsurprisingly dragging.

Hong Kong’s Hang Seng outperforming (7yr high) thanks to further gains in China (Shanghai comp 7yr high; financials leading) where the Conference Board Leading Economic Index improved but confirmed a slowing six-month growth rate, bolstering stimulus hopes while IPOs boost demand for stocks.

Japan’s Nikkei advancing on the back of the BoJ pledging to continue QQE and adjust policy where appropriate while upgrading its economic assessment for the first time in 2 years and highlighting a moderately economic recovery. Australia’s ASX the underperformer on a stronger AUD.

In Focus today we have German IFO Business climate at 0900, but the hot data will be this afternoon’s US inflation print with consensus well below that 2% target. Traders will be gathering around the telly at 6pm for Janet Yellen. Other speakers include Mario Draghi at 9am and Mark Carney at Midday. Data this morning already confirms slowing in German GDP growth from 0.7% QoQ in Q4 to 0.3% in Q1 while the annual pace of advances dropped back from 1.4% to 1.0%.

Gold trimmed losses to trade back around $1210, having fallen almost as far as $1200 on news that US Jobless claims fell to a 15yr low and the USD gained. Holding uptrend from mid-March lows, but still potential for further declines to rising lows at $1190. Support $1201, Resistance $1214.

Oil coasting sideways after making good gains yesterday; both US Light ($61) and Brent Crude ($67) consolidating themselves into possible continuation patterns which could see a break to the upside today given the current situations in the Middle East and what appears to be a pullback in the chutzpah of US shale producers this morning.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Conf Board Lead Econ Index Improved, accelerated

- Germany Q1 Final GDP In-line, confirmed

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Quintain Estates announces sale of 50% of Hilton London Wembley Hotel

- Close Brothers assets under management rise 9% year to date

- Whitbread names Lloyds' Alison Brittain as new CEO

- Nationwide CEO to retire next year, 2014 profit up 32%

- Apax Global Alpha Limited to list on London Stock Exchange

- Severn Trent full – year profits rise on higher demand

- Segro acquires logistics property firm Vailog for £28mn

- HSBC wins reversal of $2.46bn Household judgment

- Tethys Petroleum in talks to sell convertible debenture

- Prosafe: Value of BG contract reduced