Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

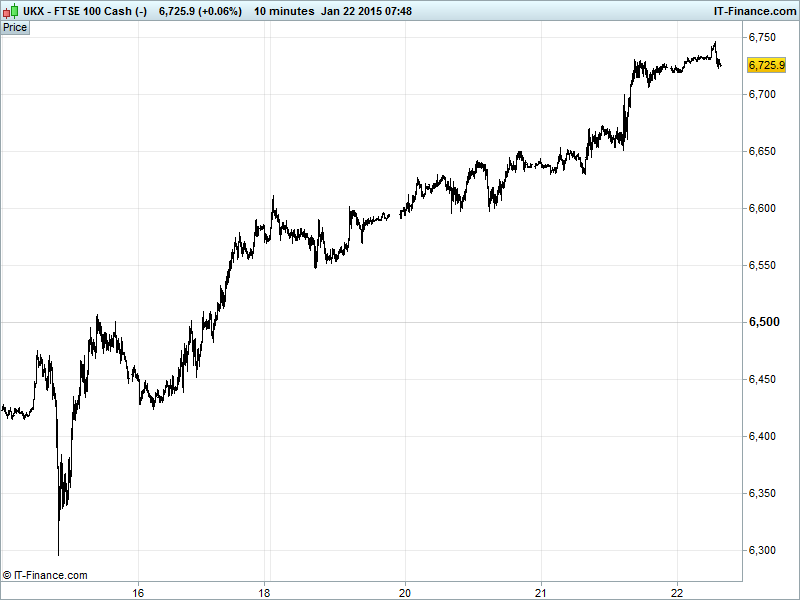

UK 100 Index called to open flat at 6725, having rallied hard yesterday following the break above both the 200-day moving average and falling highs from September. Overnight highs suggest completion of the bullish flag pattern highlighted, but gains could continue until Nov/Dec highs 6765. Updated watch levels: Bullish 6760, Bearish 6690.

The muted open follows all the excitement yesterday ahead of the ECB announcement this afternoon with additional stimulus expected and much talk/speculation following a ‘leak’ as to how it will be structured (Fed style €50bn/month). Priced in after recent market gains? Potential for surprises? Positive or negative? Gains also thanks to dovish stances from the BoE minutes and BoC rate cut (to offset oil price drop).

US markets closed higher for a third day on monetary policy optimism (ECB, BoE, BoC) but gains held back by mixed US Housing data and Chinese Premier Li saying the downward adjustment in the Chinese economy reflects the global economy, no hard landing on the cards, but continued pressure to be felt in 2015. More stimulus needed from Beijing?

After the US close, AMEX disappointed with a rise in expenses and provisions offsetting profits +11% and 4000 job cuts. Retail platform eBay reported 10% earnings growth ahead its spin-off of PayPal (still growing), while it also plans to cut 7% of its workforce/2400 jobs.

Asian markets mildly positive, as nerves rise ahead of ECB update this afternoon. China still rebounding strongly helped by the PBOC injecting more cash to meet seasonal demand ahead of the Lunar New Year, and despite the first monthly drop in MNI Business Indicator in three months.

Australia’s ASX positive despite cooling in inflation expectations and New Home Sales. Note Japan’s Nikkei buoyed by BoJ report citing continued economic recovery (moderate) with signs of demand picking up with recovery in overseas economies.

With so much optimism ahead of the ECB announcement, the risk is that yesterday’s leak provided the major headline and that there are no additional positive surprises and that worries shift to the Greek election at the weekend.

In focus today will be the ECB press update (12.30pm) and press conference (1.30pm). QE or not QE? How much? How structured? Enough to save Eurozone from deflation/recession? Elsewhere, look out for UK CBI Sales/Orders trends as well as US Jobless Claims, more US Housing readings and the Kansas City Fed.

Gold back from five-month highs $1300, hindered by weaker EUR and stronger USD ahead of ECB announcement. Another pause before completion of bullish flag pattern? Safehaven demand still important given global uncertainty (ECB action, Greek election, global growth).

Oil continues to firm, with Brent around $49/barrel and US Light $47, thanks to comments from Iraqi oil minister that he believes floor reached while OPEC secretary expects further volatility but no slide to $20-25 (a level Iran said is not a threat), with $45-50 likely the downside limit. Note US Crude stockpiles this afternoon with expectations for another build, although smaller, emphasising global supply glut.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Australia Consumer Inflation Expectations Deteriorated

- Australia New Home Sales Growth slowed

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- UK tool firm HSS Hire sets price range for market listing

- Royal Mail posts slowdown in nine-month revenue

- Wolseley may exit French building materials business

- Balfour Beatty cuts profit forecast on construction problems

- St. James's Place assets hit record 52 bln pounds in 2014

- MySale sees first half revenue up 8 pct

- Rexam completes purchase of UAC stake

- Chemring's profit falls as defence budget cuts pinch

- Oxford Instruments sees FY adj pretax profit at about 35 mln stg

- Faroe Petroleum sees 2015 production of 8,000-10,000 boepd

- Tullow Oil says exploration well in Kenya encountered oil and wet gas

- Monitise says to start strategic review of ops