Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

UK 100 Index called to open -20pts at 6250 as investors digest China’s latest economic data which unsurprisingly highlights slowing Q3 GDP growth (slowest since Q1 2009), suggesting targeted policy easing has work to do, supporting calls for further stimulus, but not as weak as expected thanks to a pick-up in exports which reinforces the government’s stance of holding off from broader intervention for now.

While China’s Industrial Production accelerated from August’s slowest pace of growth in 5 years, which may help counter some recent commodity weakness, Retail Sales growth eased, as did Fixed Asset Investment. The weak opening calls likely reflect now reduced speculation about large-scale China stimulus (mini-stimuli still possible) while global growth concerns dominate.

With China’s update out of the way and having failed to put slowing growth fears at ease, the focus will no doubt revert to dissecting global central bankers’ rhetoric for any excuses to relax via hints of accommodative stances for longer to give markets’ sugar high a second, make that third, even fourth wind.

US stocks closed higher led by gains in energy and materials despite an earnings miss by tech giant IBM which hurt industrials, while a weaker USD helped via sluggish US inflation expectations and continued global growth uncertainty, especially Europe’s drag on the US, ahead of the China data.

After hours Q4 results by Apple beat estimates thanks to impressive iPhone sales (+16% YoY) following the launch of the iPhone 6 and 6 Plus which helped it beat on revenues profits and margins and more importantly providing upbeat guidance for the current quarter with its ‘strongest product line-up into the holiday season’.

In geopolitics, Russia-Ukraine tensions appeared to escalate again with the head of the Donetsk’s People’s Republic announcing an end to the ceasefire with the Ukrainian government following reports of fighting around Donetsk airport and shelling in the City which the rebels hold in the East of the country.

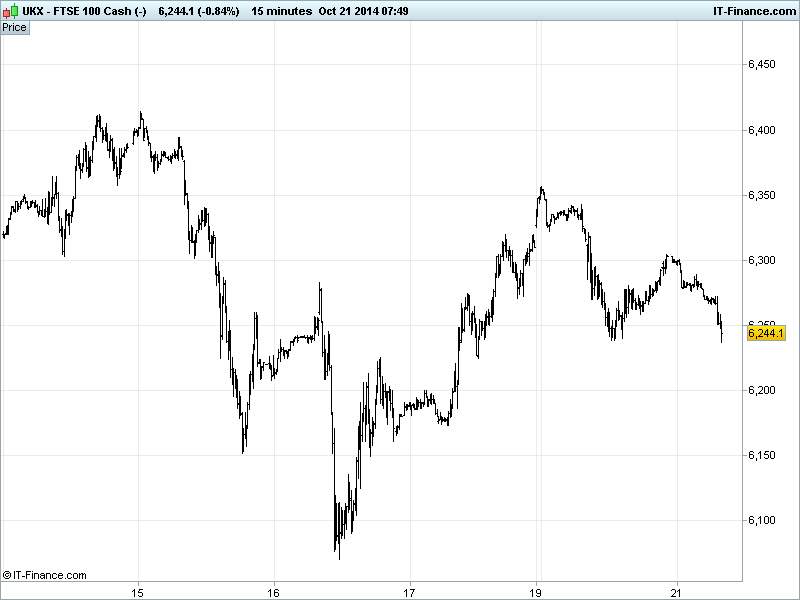

While the UK 100 index bounced from below 6100 late last week, its failure this week to regain 6400 and indeed 6350 yesterday leaves the downtrend intact, meaning 6000 lows of June 2013 could well be revisited. A soft opening call suggests China data not good enough to inspire and the raft of concerns from last week have certainly not gone away. Our watch levels move to a bullish 6350 and a bearish 6200.

In focus today amid another quiet macro-data line-up we have US Existing Home Sales which are expected to have rebounded in September. US Q3 results updates from Coca-Cola, McDonalds and Verizon Communications before the US markets while Yahoo reports after the US close.

In commodities, safehaven Gold holds near a 5-week high $1250 as investor assessment of the global growth outlook and monetary policy trajectory continues. WTI Oil is holding up around $82, and Brent at $85, off OPEC supply worry lows but without much to inspire further gains.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- CN GDP Beat, but growth still slowed

- CN Industrial Production Beat, growth accelerated

- CN Retail Sales Miss, growth slowed

- CN Fixed Asset Investment Miss, growth slowed

- JP All Industry Activity Beat, declines improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Devro says outlook for full year remains unchanged

- ASOS annual profit falls 14 pct on strong sterling

- Galliford Try Chairman Coull to step down

- ARM Holdings misses Q3 royalty revenue expectations

- Whitbread posts first – half profits ahead of forecasts

- Devro says outlook for full year remains unchanged

- Snow plough driver in Total CEO plane crash was drunk – Russian investigators

- Informa nine – months organic revenue rises 1.8 pct

- Meggitt wins contract to supply systems to new Gulfstream jets

- Hochschild Mining repays convertible bond, cutting debt by $114.9 mln

- Afilias Ltd says intends to float on London's AIM

- InterContinental posts 7 pct rise in room revenue

- GoAhead says on track to meet FY expectations

- Reckitt Benckiser reports higher third-quarter sales

- JKX says Elizavetovskoye testing well indicates 167 meters of gross pay

- GKN says on track for growth in 2014

- Carpetright says Bob Ivell to become chairman when Harris retires