Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

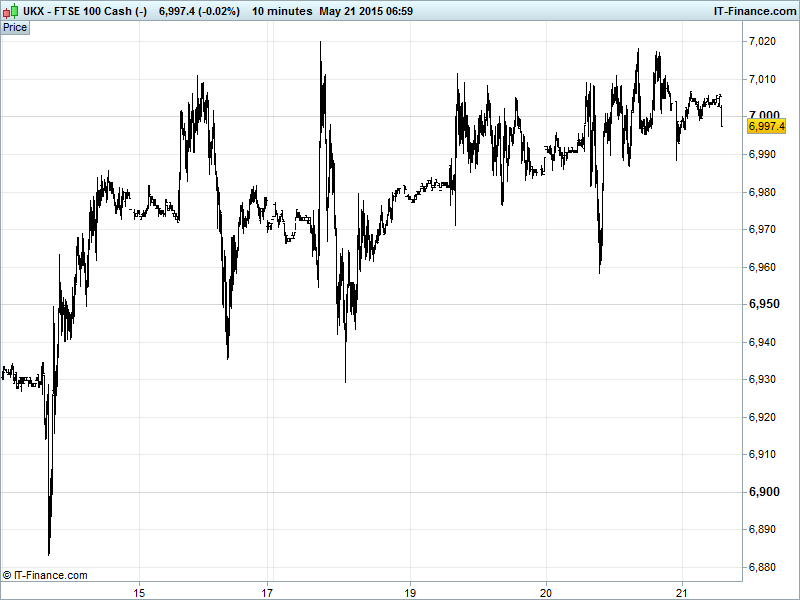

UK 100 Index called to open -10pts at 6995, holding around the round number 7000 as it moves further towards the apex of a bullish ascending triangle pattern (90pt projection if we breakout), with a 7020 ceiling and rising support 6980. The long lower candlestick wicks since mid-month show desire to bounce back from any weakness, and the break-out above 50-day MA is positive, however, further gains required to overcome the downtrend since April. Watch levels: Bullish 7025, Bearish 6950.

The negative opening call comes after a mixed US performance yesterday with markets not getting too excited after FOMC minutes seemed to reaffirm a June interest rate rise as being off the cards following unofficial Fed chatter last week that indicated the same. Greek negotiations are headed deal-wards, according to Yannis Varoufakis who said that early June would likely see an agreement reached. He also talked of allocation of funds between IMF debt repayments and Greek public sector wages & pensions with the latter two taking priority if prioritisation becomes necessary.

US bourses finished mixed and little changed, as they have over the past couple of sessions, with apparent problems concerning the US GDP calculation erasing gains made on the back of the FOMC minutes which gave the most explicit indications yet that the Fed will not raise rates in June. A split within the Fed sees many the US economy has not yet proved itself strong enough for a tightening of monetary policy while others cited macro data as supporting their arguments for an imminent rate hike. Quite what data they are talking about remains a mystery with the muted outlook for consumer spending and the pace of growth in the labour market seeming to win out in the US rate debate thus far.

Asian equities mixed again overnight following a breakeven US finish on underwhelming Fed minutes (rate rise still data dependent; June unlikely), opposing PMI Manufacturing readings from China and Japan and continued wait-and-see on Greece.

Chinese stocks outperforming thanks to calls for increased stimulus following a third straight month of contraction for HSBC’s Flash China Manufacturing PMI (new orders at 23-month low) bolstering concerns about the world’s #2 economy. Sentiment boosted by a bounce by the MNI Business indicator and Xinhua reporting Chinese Premier Li as saying China has the ability to meet 2015 GDP growth target of around 7%.

Japan’s Nikkei just positive, hitting fresh 15-yr highs thanks to a weak JPY, a Manufacturing PMI returning to growth and reports the BoJ could upgrade economic forecasts tomorrow. Australia’s ASX following Chinese equities higher thanks to the export links between the two nations and hopes for Beijing stimulus.

In Focus today we have a healthy bill of macro prints starting at 0830 with Germany’s PMI, followed by that for the Eurozone with ECB QE chat yet to boost consensus expectations for both. 0930 sees UK retail Sales, with ex-auto & fuel looking to be flat on the month and down on the year. This afternoon we have US jobless claims which consensus indicates will increase – further vindicating those US Fed doves if the data matches the forecasts. Later on will be the US manufacturing PMI, Eurozone consumer confidence & existing home sales with US Kansas City Fed manufacturing rounding off a busy day data-wise.

Gold unmoved around $1210 with bullish and bearish appetite very well matched. Still holding uptrend from mid-March lows, but potential for correction from recent highs to see another leg down to rising lows at $1190. Support $1203, Resistance $1214.

Oil prices are recovering from Tuesday’s May lows supported by improved Chinese manufacturing data overnight suggested the downward pressure on the big oil consumer’s growth may be easing slightly. EIA data also supported prices with US stockpiles falling by 2.7mn barrels in the week ending 15 May. The prospect of a US rate hike has weighed on (dollar denominated) commodities across the board of late so the prospect of a delay in policy tightening and a resultant weakening of the dollar in the world’s #1 economy are also supporting prices. A standoff between Iranian and US & Saudi warships off the coast of Yemen is also garnering traders’ attention this morning. Brent trading around $66 while US cousin WTI currently at $59.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Aussie Consumer Inflation Expectations Improved

- Japan Manufacturing PMI Beat, improved more

- China HSBC Manufacturing PMI Miss, improved less

- China MNI Business Indicator Improved

- Japan All Industry Activity Miss, bigger deterioration

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- South Africa's Investec FY profit up 10.2%

- Electra private equity sees diluted net asset value rise 12%

- Car dealership Inchcape sees revenue rise as new CEO takes his seat

- Daily Mail and General Trust sees higher EPS

- United Utilities posts rise in FY operating profit

- Electrocomponents group finance director Boddie steps down

- Darty Q4 like–for–like sales fall 0.5%

- Mothercare year profit up 37%

- Gem Diamonds says Ghaghoo mine ramp – up remains on track

- Phoenix IT Group in advanced talks for offer by Daisy Group

- National Grid posts full – year profit rise

- Just Eat says to raise about £445mn via placing, open offer

- Electrocomponents' FY pretax profit falls 5%

- QinetiQ posts annual profit rise, reaffirms trading expectations

- Optimal Payments says four-month trading in line with expectations

- Booker to buy Londis and Budgens grocery store chains