Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

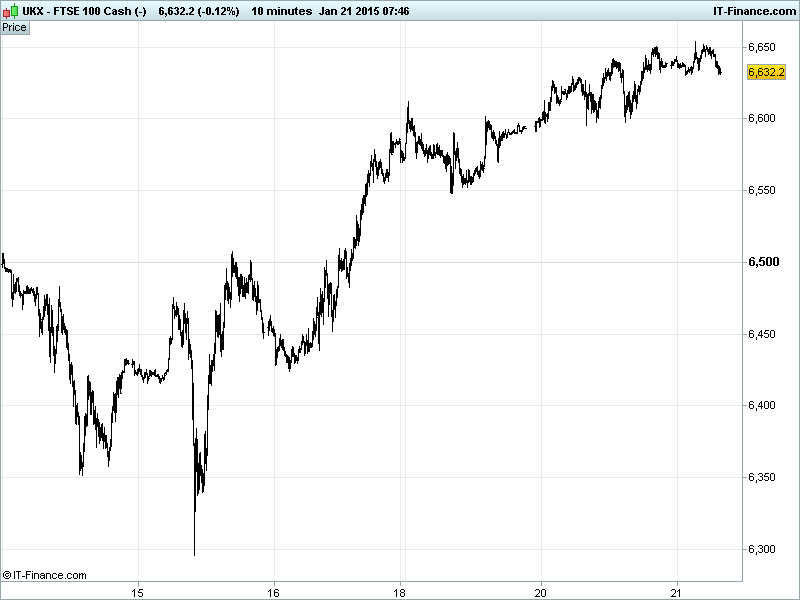

UK 100 Index called to open +10pts at 6630, building on its recent breakout even if hindered at 6645 highs overnight by 200-day moving average. A pause would make sense, and potential remains for completion of bullish flag pattern around Nov/Dec highs 6765. Note falling highs from Sept at 6685 still need clearing. Watch levels: Bullish 6675, Bearish 6590.

The positive open comes from a largely upbeat performance in Asia following better Chinese GDP and solid German ZEW surveys yesterday, some stability in Oil, and widespread expectations/complacency that the ECB delivers tomorrow, keeping global central banks accommodative.

US markets closed flat to higher with results from Morgan Stanley proving another Q4 banking disappointment while US NAHB Housing Market Index stayed flat. A tech rally helped erase losses derived from concerns over weaker corporate earnings and global growth outlook.

After the close, ratings agency Fitch said US growth underpins its stable corporate outlook while President Obama’s State of the Union address called on the America to turn the page on war and recession with far-reaching initiatives to boost wages and jobs to improve US competitiveness and fight domestic inequality.

European optimism on ECB QE hopes was offset by the Greek finance minister saying QE would not be enough to solve Athens’s liquidity problems, and called for Greek debt to be included in QE despite its junk rating. Russian President Putin was also sabre-rattling about strengthening armed forces to protect sovereignty against foreign challenges.

Asia-Pacific bourses mixed, with Japan’s Nikkei in the red due to JPY strengthening after positive macro data and unchanged BoJ policy although there was some tinkering with inflation forecasts cut (oil to blame) and GDP expectations revised up (oil to thank?). Stocks in China outperforming for a second day. Australia’s ASX the outperformer after a rebound in consumer confidence and despite stronger AUD.

In focus today, we have the UK Employment report for Nov/Dec seen showing another drop in jobless claims, another tick down in the unemployment rate and most importantly in a world of low inflation, another pick-up in wages growth with growth now comfortably above that of price rises. A welcome consumer boost.

BoE Minutes will be watched for any changes in voting and comments on falling inflation (oil again) or revised growth outlook. In the afternoon, US Housing Starts and Building Permits are expected to show a growth rebound in December offsetting the stable reading by NAHB yesterday.

Gold holds a five-month high around $1300, maintaining its northerly course and showing little sign of fatigue. Helped by weaker USD overnight and safehaven demand from uncertainty surrounding global growth and ECB action tomorrow and Greek election at the weekend. Could another bullish flag pattern complete around July $1340 highs? Note Daily RSI overbought but not yet reversed.

Oil has found support, with Brent around $48/barrel and US Light $46-7, after sliding back from highs and amid continued volatility. All eyes on US Crude stockpiles again tomorrow with expectations for another build, although smaller, emphasising the global supply glut situation. Iran still at odds with Saudi Arabia, saying no threat from $25/barrel.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Australia Consumer Confidence Improved, rebound

- Japan All Industry Activity Index Beat, stable

- Japan Bus/Econ Sentiment Beat, accelerated

- Germany Producer Price Inflation Improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Poundland Christmas quarter sales rise 10.2 pct

- WH Smith posts fall in underlying group sales

- Pets At Home reaffirms trading expectations after robust Q3

- Workspace says completes two acquisitions

- Pearson expects to grow in 2015 after solid end to 2014

- Abcam to buy Firefly Bioworks for 18.5 mln stg

- Halfords posts strong Christmas sales rise

- Computacenter sees FY results in line with board's previous expectations

- Dixons Carphone raises year guidance after strong Christmas

- Amara Mining to raise 14.6 mln stg via placing

- Land Securities reports total sales of 886.4 mln stg for nine months to Dec 31

- Hochschild says exceeds 2014 production target

- Genel slashes 2015 revenue guidance on weak oil prices

- Faroe Petroleum says awarded 5 prospective exploration licences

- Quintain Estates and Development names new finance director

- JD Wetherspoon warns half – year operating margin to be lower

- Avocet Mining says limited operations resumed at Inata mine

- Diploma says Q1 group revenue up 14 pct

- Domino's Pizza finance chief quits

- FirstGroup says UK rail, U.S. shuttle bus keep it on track

- SABMiller performance hurt by China weather

- UK's Ofgem to launch competition investigation into SSE's power connections

- Cairn completes North Sea Catcher farm-out deal