Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

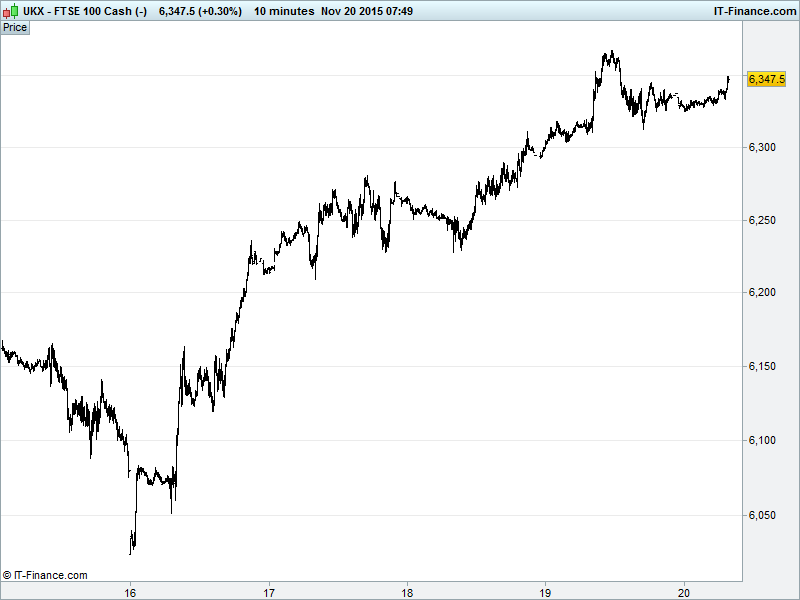

UK 100 Index called to open +20pts at 6350, having held above 6330 overnight following a pull-back from 100-day MA resistance at 6366. Bulls asking whether the week’s gains of 5.6% can be held into the weekend, maintaining the uptrend from August lows towards 6500 although 6-month falling highs lurk closely, just below 6400. Watch levels: Bullish 6355, Bearish 6320.

A positive opening call comes after Asian bourses posted gains following a slightly negative US close. Expectations of a US December rate hike may be rising (we still expect further delay), but sentiment supported by conviction in subsequent rate rises being slow and steady. The Fed can’t, after all, risk derailing global economic recovery while peers are obliged to remain in easy policy mode.

Gains in Asia see it set for its best week in a month, buoyed by a rise in metals prices (Copper breakout) as the USD retreated from highs, the chance of a US rate rise now pretty much baked in. Could this mean a December hike actually results in the USD pulling back from its highs, throwing a lifeline to battered commodities and their Miners? It is said that Long USD is one of the most crowded trades right now. Note however Goldman Sachs suggesting Oil could yet fall back to $20/bl.

China held back by debt mountain concerns and despite growth in the Conference Board Leading Economic Index. While Japan’s Nikkei is hindered by the stronger JPY, Australia's ASX is outperforming thanks to a brighter session for Commodities.

A largely flat Thursday for US equities saw stateside indices close marginally lower. healthcare the noted underperformer while consumer staples, utilities, airlines and industrials benefited - presumably in part from Goldman Sachs’ outlook for oil which saw further downside in the short-term (beneficial for consumers) while some upside towards year-end - better for producers, but note the investment bank is touting $20 oil this morning.

In focus today, in the absence of any major market-moving data except Eurozone Consumer Confidence (flat), expect much attention on what the raft of Central Bank Speakers including ECB President Draghi, several of his colleagues, and Fed counterparts have to say. With the potential for December to see a US rate rise and more stimulus from the ECB, potential for volatility depending on what is said.

Oil prices have flattened out this week and are range bound in the low- to mid-$40s (narrowing patterns for both Brent and WTI a concern for bulls), this having been the case all week but with the world now running out of storage space, the outlook is anything but bullish.

Investors preferring to see downside then, pushing E&P and other energy sector stocks down. Be prepared for a reversal of fortunes if the GS prediction rings untrue, and while we’re talking Goldman Sachs keep an eye on the Eurodollar, with the bank calling for parity by end-Dec.

Gold still treading water near 5-year lows with technicals indicating a bounce off the floor of what is nonetheless a 2-year falling channel. We still don’t expect much upside due to Dollar headwinds - the US Dollar Basket has also bounced off the floor of its own rising channel (a break above 99.6 would put 99.8 on the cards for the and place more pressure on Gold).

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Sunrise Resources says unaware of undisclosed reason for share price fall

- Fuller Smith & Turner says H1 revenue rises 10%

- Melrose Industries optimistic a suitable acquisition will be identified

- Lonmin says subdivision of ordinary shares to be effective on LSE on Friday

- Spectris sees FY adj operating profit towards lower end of market expectations