Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

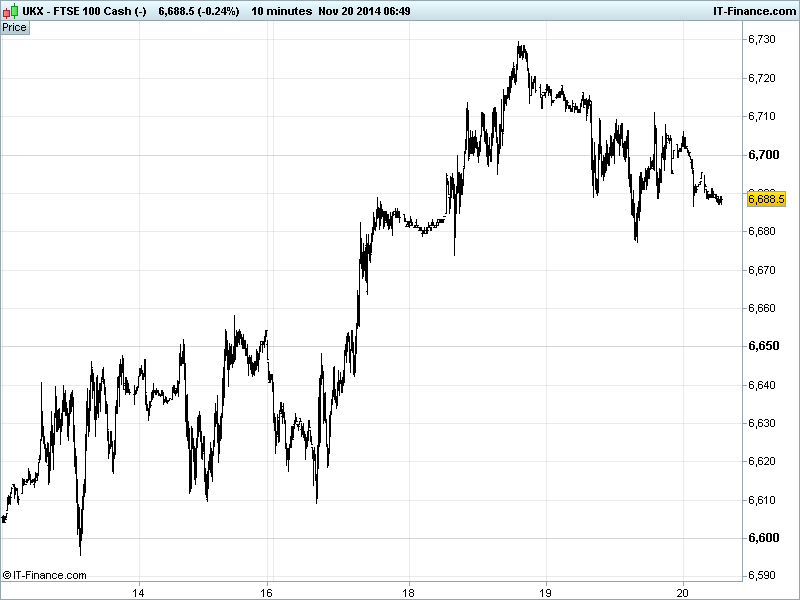

UK 100 Index called to open -10pts at 6686, maintaining its downward bias from recent 6730 highs thanks to underwhelming Fed minutes and disappointing China Manufacturing. Nonetheless, watch level 6675 yet to be tested so potential for support 6680 to keep overall uptrend from 17-Oct alive, and a revisit of 6900 by year-end. Our watch levels stay put: Bullish 6735 and Bearish 6675.

Negative open stems from HSBC PMI Manufacturing falling to a 6-month low of 50 (breakeven) in November (from 50.4), missing consensus 50.2 and adding to signs that more stimulus is needed to offset slowing growth in the world’s #2 economy. There is talk of China boosting banks’ lending power to help spur growth, with more flexible loan-to-deposit ratios (short term boost, longer term danger?)

US equities closed flat-to-lower yesterday after Fed minutes showed policy makers debating whether to communicate more about views on probable pace of interest rate rises next year, with many agreeing they should be on the lookout for a fall in long-term market-based interest rate expectations (fear of complacency?) and some wanting to remove “considerable time” language. Anxiousness about undershooting inflation target and dependence on data/outlook suggests any hike is still a good way off yet.

Asian equities mixed with a flat US-like finish for the Nikkei and the Hang Seng but the ASX in the red. We have Japan’s Nikkei helped by further JPY weakening (divergence in Fed and BoJ policy; rate hike prep vs more stimulus) after Japanese PMI manufacturing declined to a 3-month low while trade data largely improved with exports expanding the most in 8 months. Note Australia underperforming due on China PMI.

In focus today, amid a very busy calendar, will be PMI Manufacturing and Services for France, Germany and the Eurozone, with small improvements expected all round, but the former staying in contraction and holding back the Eurozone. This morning’s German Producer Prices confirm deflationary worries with negative prints.

UK Retail Sales are seen rebounding in October, although still likely hampered by the mild weather which clothing retailers spoke of in recent results. US Consumer Price Inflation (CPI) seen giving up ground in October (lower oil prices) reinforcing Fed minutes last night and recent US inflation data (falling).

US PMI Manufacturing is forecast to gain ground, consensus puts Existing Home Sales weaker in October after a strong September (similar to US Housing Starts yesterday), the Philadelphia Fed is expected to fall back another couple of points to Q2 levels but the troubled Eurozone is forecast to show marginal improvement in Consumer confidence in November.

In commodities, Gold holding around $1180 on stronger USD and as markets continue to decipher Fed minutes and eventual timing of a rate hike given current data.

Oil prices holding around recent lows with Crude at $74.5/barrel and Brent Crude $78/barrel slipped again as we inch closer to next week’s OPEC meeting. Will it cut production to stem price falls? Or will it emphasise its global power and hold steady? China PMI data only goes to highlight uncertainty of global demand.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP Manufacturing PMI Miss, deteriorated

- CN HSBC Manufacturing PMI Miss, deteriorated

- DE Producer Price Inflation In-line, deflationary

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Young & Co's H1 revenue rises 7.8 pct

- RBS fined 56 mln stg for 2012 IT failures

- BAT says Nicoventures MD Des Naughton to leave firm

- UK losses weigh on Mothercare's profit growth

- IP Group says Modern Biosciences unit gets 2.4 mln stg grant

- Babcock reaffirms full-year profit outlook, raises dividend

- Quindell not "actively seeking" to sell Nationwide Accident Repair Services stake

- UDG Healthcare full-year operating profit rises 9 pct

- Centrica lowers earnings per share forecast as mild weather bites

- Euromoney Institutional FY underlying rev up 3 pct

- Close Brothers sees "good" full-year results

- Johnson Matthey posts growth in half-year profit, lifts outlook

- Rio Tinto says Megan Clark to join the board

- QinetiQ maintains forecast for flat annual profit