Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

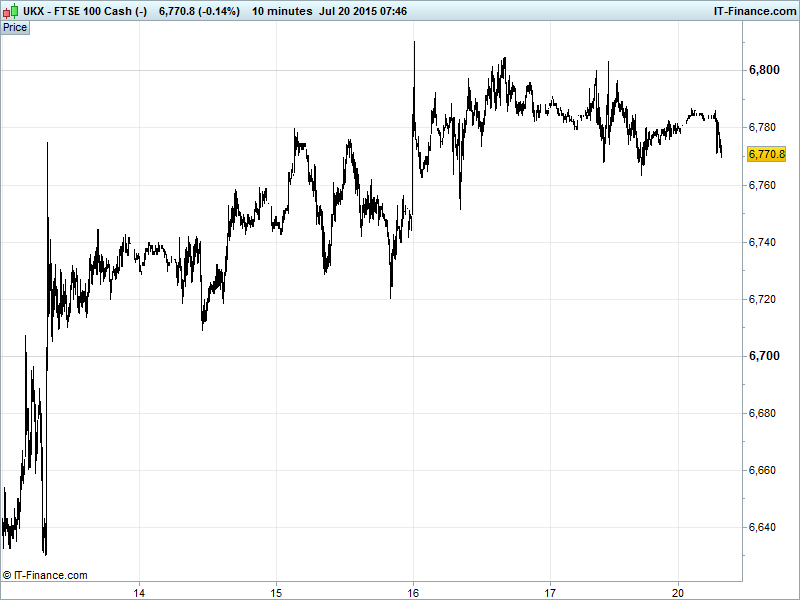

UK 100 Index called to open -5pts at 6775, still consolidating around 6760-6800. While the bounce from 6415 9-month rising support is still valid we note loss of momentum at 6800 and overnight resistance 6790. Nonetheless, it’s still possibly just a pause before another rally towards May/June highs 7000 with support available from 200-day MA 6750. Updated Watch levels: Bullish 6815, Bearish 6740.

The tepid opening call comes despite news of Greek banks reopening today, a solid start to US Q2 earnings season and German Chancellor Merkel signalling that Greek debt relief (maturity extensions, lower interest rates) is an option for the third bailout, even if she continues to rule out a write-off/haircut of any description.

This is due to China’s government/regulatory-led equity market recovery seeing volatile trade and Gold seeing a sharp slump to 5yr lows (The USD index hits 3-month highs, China holds less reserves) and Greek progress sees focus revert to outlook for US interest rate lift-off, especially with ratings agency Fitch saying its expects a rate rise by year-end.

Greek banks today resume a limited range of services with capital controls still in place (weekly rather than daily withdrawal limits) following German approval of a third bailout plan, the ECB’s extension and increase in Emergency Lending Assistance (ELA) and a €7bn bridge loan in place allowing Athens repay an ECB bond due today and clear IMF arrears.

While some less onerous reforms still need passing into law in Athens this week, the main hurdles appear to have been cleared, however, PM Tsipras has lost more support, requiring a cabinet reshuffle and increasing political risk via the chance of snap elections in the autumn.

US stocks closed mixed on Friday with the Nasdaq outperformance to new highs continuing thanks to a very positive reaction to Google’s Q2 results while other indices were buoyed by progress on Greece, strong US housing data and in-line US Consumer Price Inflation readings even if consumer confidence disappointed.

Asian bourses largely lower overnight with Friday’s mixed cues from Europe and the US spill over into a quiet start to the week. Japanese markets closed for Marine Day holiday while HSBC has forecast a further cut in Chinese banks’ reserve requirement ratio and further monetary easing in Q3 to encourage economic activity out of the slow lane. House price growth data from the world’s #2 economy showed an increase on the month while a longer term slowdown continues with a 10th consecutive YoY decline, albeit at a slower pace.

Australia’s ASX outperforming despite high volatility in the commodities realm overnight (hurting Aussie listed miners) after China announced it had boosted its bullion assets by less than analysts had forecast, and amid general concerns about the US Fed’s plans to raise interest rates in the near future; a stronger US Dollar impacting dollar-denominated commodities off the back of it. Platinum went sub $1000 for the first time since 2009 and Gold extended its own 5-year lows.

US light Crude ($51) and Brent ($57) still trading around their respective support levels with pressure in the form of an Iran nuclear deal and imminent US rate rises (more likely now that Grexit risk is off the table). Falling US inventories and higher demand from US refineries supporting prices, just, into this week.

Gold ($1116) is recovering this morning having lost 4.2% overnight, in the midst of a longer term downtrend (sixth straight day of declines), in reaction to data from China and US Dollar strength impacting the commodities sector as a whole. Prior support $1140 now resistance?

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Standard Chartered reshuffles management team

- UBM appoints Robert Gray as CEO of PR Newswire

- Aveva to buy Schneider Software

- Worldview Capital Management requests separate Petroceltic EGM

- Rolls – Royce says International Airfinance buys Trent 700 engines for 20 aircraft

- Rolls-Royce wins new engine contracts totalling $2.23bn

- Tullow Oil suspends gas export from the Jubilee Field to Ghana Gas plant

- British Land says has had a good start to the year

- IQE says on track to achieve its FY expectations

- Wincanton secures contract with BAE Systems

- S.Africa's Amplats still weighing disposal options, H1 earnings soar

- Anglo American sees H1 underlying earnings of $175m from Amplats