Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

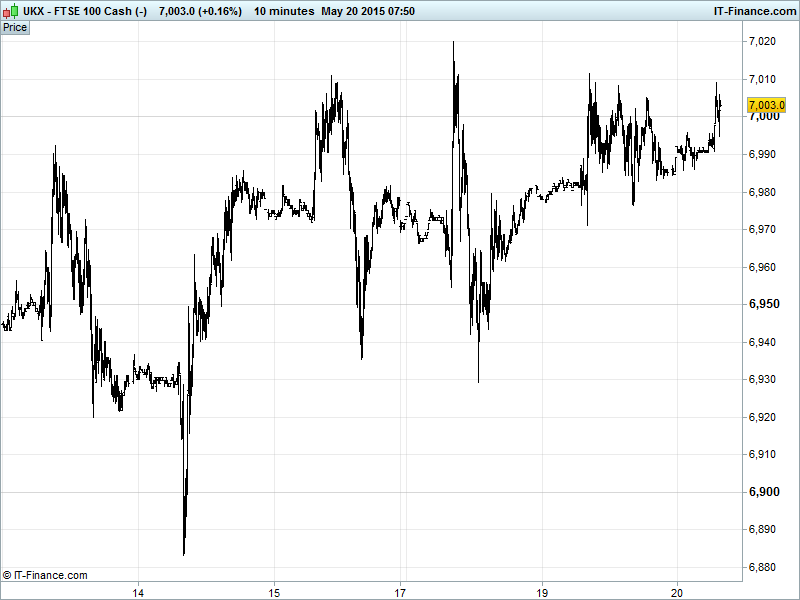

UK 100 Index called to open +5pts at 7000, maintaining the uptrend from May 7 lows of 6808 and breaking above the 50-day MA but still struggling to make much progress beyond brief forays above 7000 and thus yet to overcome downtrend from 16 Apr. The 3-day sideways 6930-7020 shift persists. Watch levels unchanged: Bullish 7025, Bearish 6925.

The positive opening call comes after European equities bounced on Tuesday as the ECB’s Nowotny said deflation in the Eurozone is no longer a threat and that negative interest rates are only temporary, although long term growth cannot be guaranteed by loose monetary policy alone. The ECB bond buying programme is likely to continue and even accelerate if required to ensure the Eurozone’s target inflation rate is reached. The assertiveness of the European Central Bank on the matter saw the DAX make an impressive 200 point advance while UK 100 managed to pop back up above 7000.

In Europe this morning indications are that, while there has been progress in negotiations, Greece will miss its June debt payment to the IMF unless a deal is reached by the end of May in which concessions for Greece are highly unlikely - the EU will almost certainly face a second revolt in the form of Portugal’s ascendant socialists if any are afforded to Athens.

US bourses finished flattish on Tuesday after posting record performances over the past couple of sessions, taking a break on near term uncertainty but supported by positive macro data in the form of the highest Building Permits reading since 2008 and Housing Starts up the most since 2007. Many eyes will be on the US Department of Justice today as five of the world’s biggest banks – UBS, JP Morgan Chase, Citigroup, Barclays and RBS are due to settle with US regulators today on forex rigging charges, with RBS also due to settle with UK authorities.

Asian equities mixed overnight, echoing Wall Street’s indecision ahead of this evening’s Fed FOMC minutes and looming Greek deadlines, but otherwise supported by a rebound in US housing data to the highest since 2007/8 and helpful ECB comments about QE, rates and deflation, all of which gave the USD a boost, weakening Asian currencies and benefiting exporters.

Japan’s Nikkei outperforming thanks to a weaker JPY and better than expected preliminary GDP data indicating a sharp acceleration in Q1 growth (fastest in a year). However, stripping out inventory builds meant the data was in-line, still struggling to gain traction following last year’s consumer tax hikes. Slowdown in Q2?

Australia’s ASX flat, held back by resources stocks which have been hindered by the rally in commodities being capped on concerns about weakness in China and the stronger USD, with no help from a rise in Consumer confidence to the best since Jan 2014 after the recent budget and interest rate cut. China stocks mixed and Hong Kong’s Hang Seng hampered by energy names reacting to a slump in energy prices on renewed USD strength.

In Corporate news, ratings agency Fitch has hit RBS with a 2 notch debt downgrade (significant pressure on profits) while it upgrades Lloyds (praised financial health) and maintains ratings on Barclays and HSBC. IN total Fitch downgraded more than 20 European banks by 1-4 notches after a review of sovereign support. While UBS has settled with US prosecutors, pleading guilty to FX manipulation and paying $545m in fines, we await news on how much Barclays and RBS have to pay.

In Focus on a quiet Wednesday we have Eurozone Construction Output followed by US MBA Mortgage Applications around lunchtime – one to watch after Monday’s disappointing NAHB housing market index and yesterday’s better than expected Housing Starts et al.

Oil prices fell by a massive 3% on Tuesday and are again lower this morning following a small overnight recovery as Militiamen and Iraqi Government forces encircled the city of Ramadi in preparation for a ‘liberation’ attempt. The recovery lost steam on a strongly rebounding US Dollar, however, which weighed on prices Tuesday and continues to win out against Middle East unrest this morning. Brent currently trading at $64 while US cousin West Texas Intermediate (AKA US Light) lower at $58.

Gold maintained its pullback from multi-month $1233 highs to trade down around $1200. Support? Back testing 50- and 100-day MAs. Concerns over Greece being overshadowed by USD strength after US Housing data rebound and ahead of the Fed’s latest FOMC minutes this evening. Support $1200, Resistance $1210.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan GDP Beat, growth accelerated

- Aussie Consumer Confidence Improved

- Japan Confidence Indices Mixed

- Germany Producer Price Inflation Miss

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Morgan Advanced Materials says FY expectations remain unchanged

- Increased traffic drives Zoopla H1 core earnings up

- Cable & Wireless posts first top – line growth since 2010 demerger

- UBS says to settle FX probe, pay $545mn, plead guilty over Libor

- Sacoil says withdraws participation in Oil Prospecting Licence 233

- Thomas Cook says dividends could resume from next year

- Hargreaves Lansdown posts record inflows in 4 months to end – April

- Faroe Petroleum says to abandon dry Bister exploration well 6407/8 – 7

- Burberry sounds cautious note after seeing profit rise

- John Laing Environmental Assets Group to raise £45mn via placing

- UK Mail cautions on full-year results on transition to new hub

- UK Mail sees FY performance more weighted to second half than usual

- CSR says trading and outlook in line in AGM update

- SSE beats full-year estimates, helped by energy supply business

- M&S profit rises for first time in four years