Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

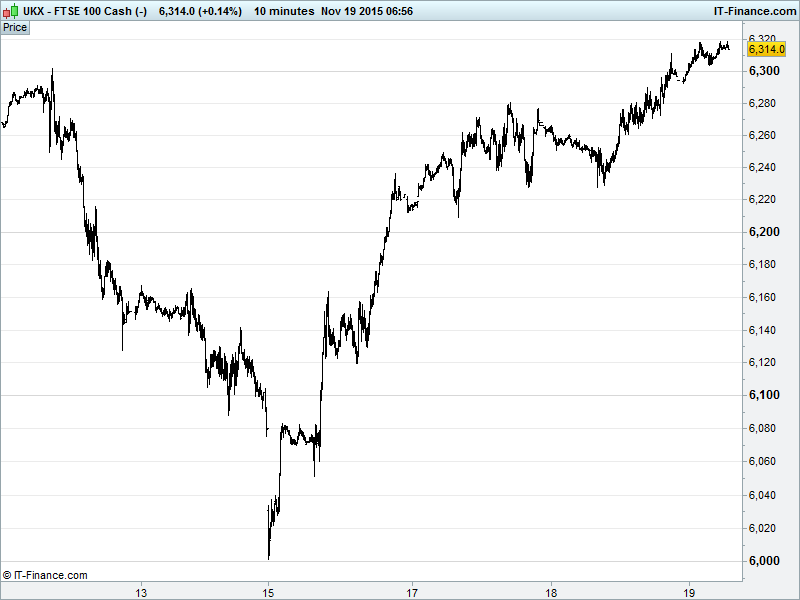

UK 100 Index called to open +35pts at 6315, having made a break above 6300 overnight which the bulls hope will serve as support for any subsequent retreat, keeping the Aug recovery on track for May/Aug/Nov falling highs at 6400. Potential for recent oscillation around 6250 to have been a pause before another 200pt advance towards June falling highs at 6500. Watch levels: Bullish 6335, Bearish 6295.

The positive opening call comes after US and Asian bourses reacted positively to the Fed minutes which, while pointing towards increased potential for a December rate hike, handily left the door ajar for further delay whilst reiterating that any further tightening would be very slow and very gradual. Perhaps even a touch less hawkish than last month? Be prepared for a very dovish hike.

Markets clearly liking the US central bank’s faith in US economic recovery and belief that a gentle ‘testing of the water’ first move towards policy normalisation, whilst peers are doing the exact opposite, will not derail economic recovery or deliver market mayhem. Just that little bit more certainty goes a long way. A USD off its highs is giving commodities a little help from yesterday’s fresh lows.

Asian stocks positive taking the lead from Wall St, on reduced uncertainty regarding Fed policy. Japan’s Nikkei higher despite the BoJ leaving policy unchanged despite the nation falling back into recession and the JPY gaining on USD weakness. Chinese stocks lower in spite of a plunge in Business Sentiment. Australia’s ASX is the regional outperformer after commodities got a lift from a weaker USD.

US stocks rallied Wednesday as the markets gleaned what could have been a little added clarity from the FOMC meeting minutes. Less hawkish than of late (still hawkish though…), but with the USD showing near record strength this week it would be in the interests of the Fed to rein in its uber-hawkish rhetoric just to try to control it in the run up to December. As above, the door remains ajar. An Apple upgrade to 'Conviction Buy' from Goldman Sachs also did its bit to boost sentiment.

In focus today, will be UK Retail Sales which are forecast to be weak while CBI Trends are seen improving on last month’s weakness. In the afternoon, the US Philadelphia Fed could recover back to break-even while the US leading Index could rebound strongly, both vindicating the Fed’s view that data could continue to improve, paving the way for an early Christmas present. With all eyes on the ECB for more stimulus to help the region and counter a Fed hike, watch out for the latest ECB minutes and several ECB speakers today.

Oil up off the lows of yesterday but suffering underneath 2 weeks of falling highs. Both Brent and US Crude remain near support as the strong Dollar and global supply glut continue to weigh. Note, however, currency fluctuations (USD off highs this morning) and bottom-picking continue to provide swing trade opportunities.

Gold has recovered slightly, tracking those small USD fluctuations. We’re still not expectant of any big moves in the short term with the US Fed still on track for a December rate hike (making interest-bearing US treasuries more desirable as a safe haven) and physical demand muted (buyers waiting for it to get even cheaper?).

With all this talk of the USD, an overnight gap-down on the US Dollar Basket could be filled today making for a potential trade opportunity.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Royal Mail sees lower FY operating cost

- Bovis Homes says sales rate strengthened in the autumn

- Ted Baker group sales for 13 weeks to 14 Nov rise 20.5%

- Domino's Pizza says CFO Doughty has resigned

- Euromoney says Q1 has started in line with board's expectations

- UK Lender Close Brothers says remains confident in FY outlook