Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

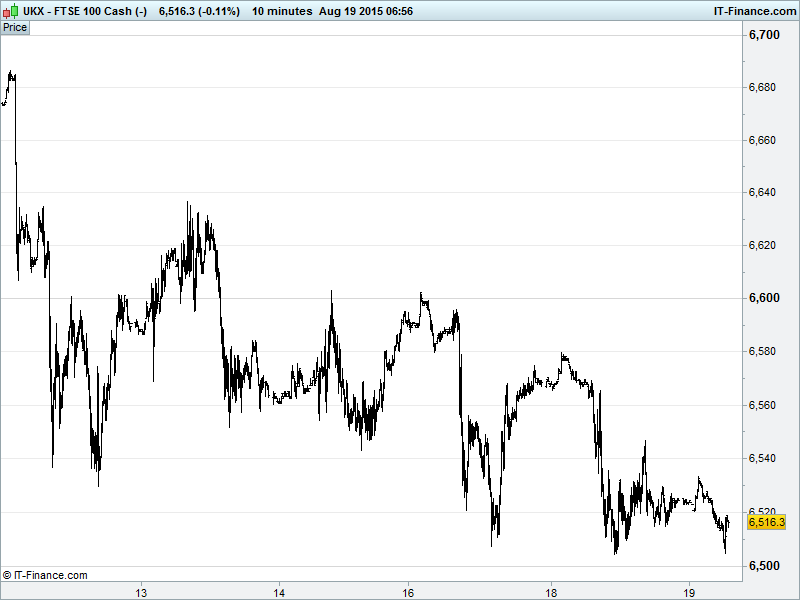

UK 100 called to open -30pts at 6505, approaching the floor of its week-long falling channel having spent much on Monday ranging around 6520. Downtrend from 10 Aug still intact with July rising lows and the 6550 level now breached. Disappointed Bulls now looking for the channel floor 6480 to hold firm for a 70-odd pt bounce while Bears still riding the decline. Watch levels: Bullish 6550, Bearish 6420

The negative opening call comes amid a China sell off that continues with the absence of further intervention by the people’s government proving to wealthier investors that there’s little hope to be had in the stock market’s ability to hold itself up. China being a global growth barometer, the ripple effects will be felt the world over.

Asia Pacific stocks followed China lower overnight with equally weak leads from Wall St, also on China concerns, compounding general market worries. Japan's July trade deficit widened a lot more than expected (-¥268.1bn vs. f/c -¥53.0bn) after a downward revised -¥70.5bn in June. Exports came in above expectations while imports fell less than expected.

US stocks closed lower on Tuesday, with macro-issues concerning the situation in China and micro-ones concerning US company earnings as Wal-Mart disappointed. Risk-off fixed income markets subdued on a solid housing report while oil prices rebounded somewhat on profit taking (outlook still very bearish though).

In Europe, both the Spanish and Austrian parliaments have backed the Greek bailout deal ahead of the German vote today, which is widely believed to pledge its support for a third unimaginably large bank transfer that will probably never be paid back. No debt haircut as put forward by the IMF but the lead creditor nation will consider re-structuring in the form of extended maturities and interest rate alterations.

Outgoing BoE MPC member David Miles went on the hawk-fensive to say that UK interest rates will rise pretty soon. They have to, since one can always find some reason not to hike rates and to continue the current artificial situation would lead to market distortions. We’re inclined to agree, but it’ll take a gutsy decision to actually go ahead on this. Low interest rates are nice.

In focus today we have a market-stalling slew of US data, starting a 12pm with MBA mortgage applications, continuing with CPI data at 1.30pm and culminating in the Fed meeting minutes at 7pm. Note we’re unlikely to see much in the way of volatility in the US markets until later on this evening as traders remain on the sidelines awaiting Janet Yellen & Co.

US Light crude ($42) benefitted to the tune of less than 1 buck yesterday as profit taking boosted the price, though today’s candle resembling a spinning top so far, indicating a potential return to prevailing bearishness. OPEC still pumping it out at record levels in competition for market share, which is hitting some members hard – including Iraq and Venezuela. Traders awaiting inventory data today for clues about US demand. Brent firm at $48

Gold ($1120) appears to be regaining safe haven status, although China’s outlook could signal more government intervention and thus currency fluctuations which may be keeping demand high. Again, big moves unlikely ahead of this evening’s FOMC minutes and subsequent USD movements.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Glencore posts 29% fall in H1 earnings

- Insurer Admiral posts 1% rise in H1 profit to $292m

- Imperial Tobacco says on track to deliver FY targets

- Hikma pharmaceuticals H1 operating profit falls

- Ricardo buys environmental consultancy Cascade Consulting

- Sirius Minerals announces upgrade of offtake agreement

- Circle Oil says Tunisia approves renewal permit for Mahdia block

- Enquest H1 rev $444m