Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

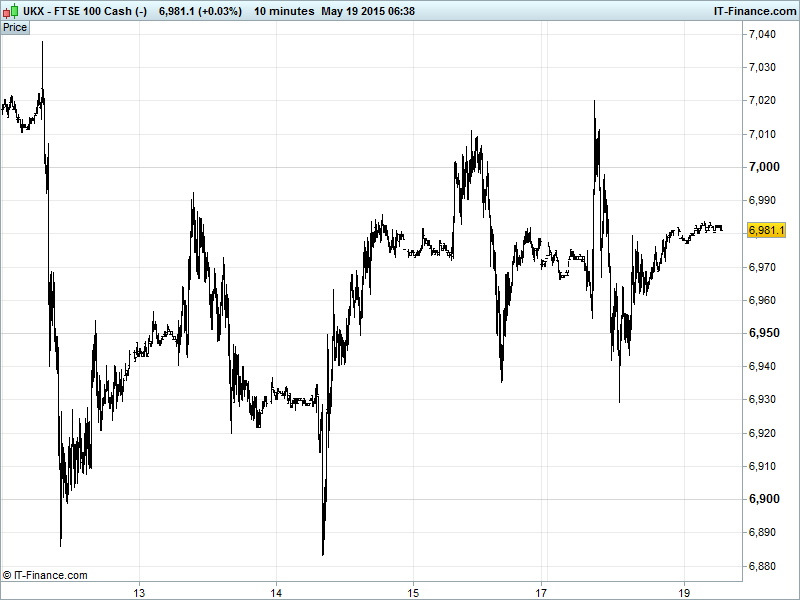

UK 100 Index called to open +10pts at 6980, maintaining the sideways 6930-7070 shift since Thursday afternoon, with yesterday seeing another test of both the floor and ceiling. Uptrend from 7 May intact but yet to overcome downtrend from 16 Apr. Still holding above 100-day Moving Average (6921) while testing 50-day MA. New watch levels: Bullish 7025, Bearish 6925.

The lukewarm opening call comes after the US San Francisco Fed released a paper stating that it believes Q1 growth has been understated and may be due for a significant upward revision in Q2. This would put a June interest rate rise back on the cards, according to Chicago Fed chief Evans who nonetheless continues to push for a delay until 2016, which still looks the more likely scenario with the 2% inflation target still not met.

In Europe, a Greek bailout deal is still wayward as sentiment among creditors and observers remains unconvinced in stark contrast to the mood of the Greek government which is confident that talks are ‘in their final stage.’ Whether the outcome will be good or bad remains to be seen and depends on who you ask.

US bourses made record highs in Monday trading with Apple shares boosted by comments from god-like activist investor Carl Icahn who said he thought they were worth $240 a pop. The Dollar Basket rallied strongly on expectations that strong macro data this week will wipe out doubts cast by a string of consensus-missing prints over the past couple of weeks to place a June interest rate hike back in the US Fed’s crosshairs. Note, however, yesterday’s NAHB Housing Market Index miss that while not of great importance, may not bode particularly well for further, better heeded MBA Mortgage Applications data due out on Wednesday.

Asian shares have advanced overnight, following a record Wall Street close, led by China as bonds trend lower and cautious optimism remains that Greece and its creditors will cobble ‘something’ together to allow release of much needed bailout funds to pay workers and the IMF. Japan’s Nikkei outperforming again (back >20,000) ahead of tomorrow’s GDP print, thanks to a weaker JPY boosting exporters and BoJ comments suggesting QE working with moderate economic recovery trend and inflation expectations rising.

Note Chinese stocks rallying on Beijing announcement of fresh investment plans (railways), led by brokerages and energy names as investors seek benchmark underperformers amid the recent flood of IPOs. Note an FT article on China’s record capital outflows due to financial stability fears. Aussie ASX bucking the trend with energy names leading the losses as investors digest dovish RBA minutes which maintained a mild easing bias but with a stronger AUD continuing to drag on the export-focused economy.

In Corporate news, results this morning from Vodafone (VOD) show its first gains for service revenues in 11 quarters as demand in Europe improved, with hints of stabilisation. Operating profit excluding exceptionals fell 19% on increased investment. Land Securities (LAND) has increased its dividend by 3.7% thanks to a jump in demand and valuations for commercial property.

In Focus today we have UK CPI data at 0930, consensus flat on the year and up on the month, with the same from the Eurozone at 1000 looking to be flat again on the year but down on the month. Zew Surveys this afternoon take in the Eurozone and Germany with the latter expected to indicate a worsening in economic sentiment – no doubt encouraged down by tiresome Greek negotiations that seem locked in circular motion.

Gold back down around the $1220 level after yesterday’s early visit of multi-month $1233 highs with the USD bounce from 4-month lows (speculation US Data later this week could bolster the case for a US rate rise) weighing on the safehaven metal. Concerns over Greece as well as the global growth and monetary policy outlook still providing support. Support $1210, Resistance $1233.

Brent ($66) and US Light Crude ($59) both steady this morning with reports of violence in the Middle East supporting prices in the face of resistance from renewed global supply glut worries with OPEC refusing to cut production and US shale drillers vowing to up theirs. Iraqi Shiite militias are converging on Ramadi in an attempt to retake the city from ISIL fighters and prevent them from marching onwards to the capital Baghdad. OPEC member Iraq is the world’s 2nd largest oil producer, accounting for around 4% of the world’s supply.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Aussie COnf Board Leading Index Deteriorated

- EU New Car Registrations Growth slowed

See Live Macro Calendar for full data line-up, incl. consensus expectations