Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

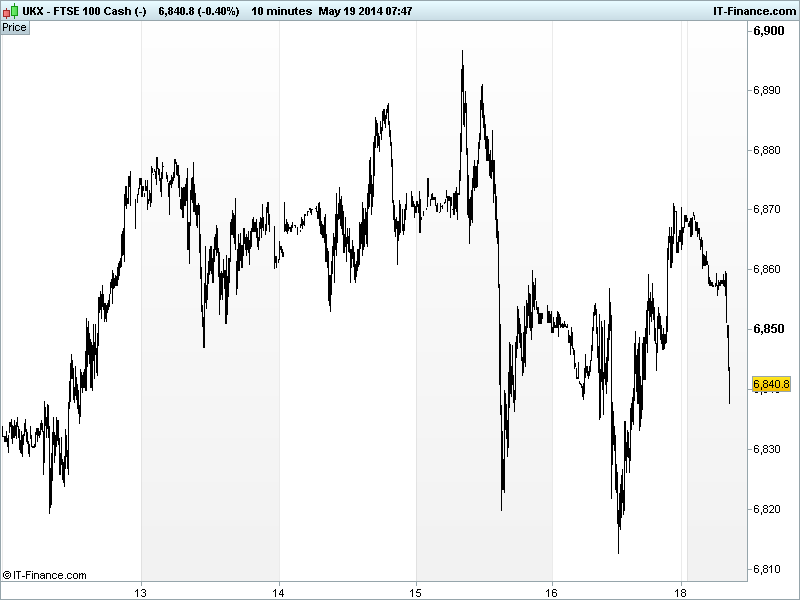

UK 100 called to open the week -15pts at 6840, as caution reigns with bourses in Asia mostly lower for a second day, China and Australia leading the declines, in the wake of Sunday’s China Property Price data (price rises at 11-month low; bubble deflating) which gave rise to further fears of distress in the world’s #2 economy and saw commodity prices such as Iron ore fall further with a knock-on to the Aussie listed mining stocks.

US markets closed slightly higher on Friday, despite a drop in consumer confidence, with little in the way of catalysts bar solid housing data and the Fed’s Bullard arguing that the economy is the closest it has been to its inflation and employment goals in 5 years but there remains work to do, noting the Fed is willing to be more aggressive if inflation out of hand, and rate rise expected Q1 2015.

Data overnight included UK Rightmove House Prices which showed continued acceleration (London hitting new record on shortage of sellers) and will surely add to the weight of concern we saw last week and from the BoE Governor Carney himself again over the weekend (‘housing market has deep problems and biggest risk to financial stability’). Note Japanese Machine Orders delivering a much stronger rebound than expected.

On the topic of ECB stimulus, over the weekend the ECB’s Praet suggested to German newspaper Der Spiegel that he would recommend a rate cut to 0.15% and a adopt a new negative deposit rate at the next meeting. Fighting has continued between Ukrainian forces and separatists in ahead of presidential elections and after declaring independence and desire to join Russia and wanting elections later in the year.

On the M&A front, Pfizer has upped its bid for AstraZeneca to 5500p per share (2476p cash + 1.747 PFE shares), with the sweetened supposedly ‘final proposal’ again being rejected by AZN. The Qatari Royals are buying a €1.75bn stake in Deutsche Bank as part of its $11bn capital raising plans, which may buoy peers, but Vodafone may suffer on confirmation that mooted predator AT&T is to buy DirecTV for $67.1bn.

In focus today we have the ECB and Bundesbank’s Jens Weidman speaking at 8am, Eurozone Construction Output data is released at 10am, the ECB’s Mersh and Coeure speak at 9am and 10.30 respectively, and in the afternoon we have the Fed’s Williams speaking about monetary policy at 5.10pm and the IMF’s Lagarde at 5.30pm.

The UK flagship index remains off its recent highs of 6900, having tried as low as 6815. Late Friday saw a move to 6870, at which resistance was encountered and the China property data has helped it back down below 6850. The failure at 6870 hints at a loss of momentum, reinforced by the daily indicator almost back to neutral. Support still valid at 6820.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- CN Property Prices Slowed further

- UK House Prices Accelerated further

- JP Housing Loans Stable

- JP Machine Orders Beat, rebound

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Alent says trading in line with expectations

- AstraZeneca rejects 55 pounds/share Pfizer offer

- Cranswick FY adjusted pretax profit rises 6 pct

- Dixons Retail to sell central European operations

- Punch Taverns to sell 4 pubs for 6.7 mln stg

- Babcock says confident on strong progress for year ahead