Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

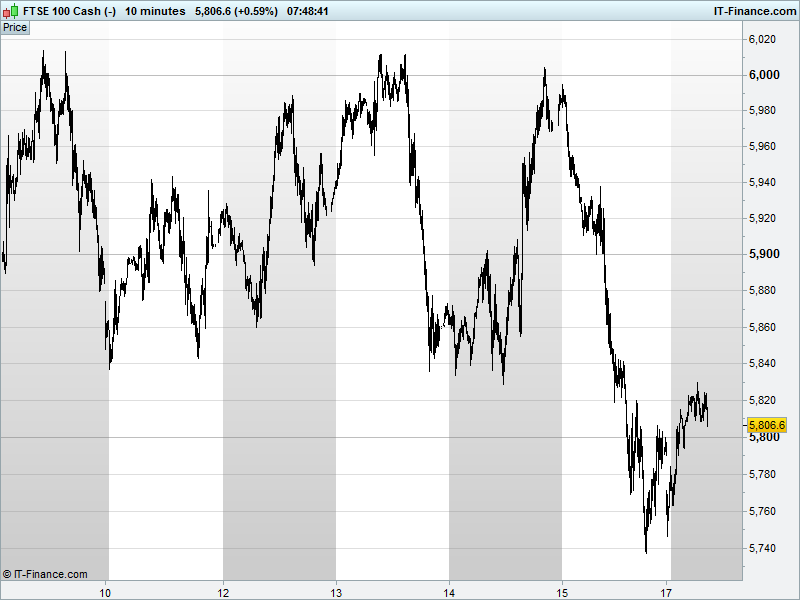

UK 100 Index called to open flat at 5805 having recovered from a double-test of 5765 summer lows, however, progress already checked at 5830 (95pt bounce from 5735 lows) with the base of last week’s sideways consolidation channel already turned resistance. The leg down late on Friday maintains the poor start to 2016 although we note positive RSI divergence (RSI uptrend versus index downtrend) offering potential for index reversal. Watch levels: Bullish 5855, Bearish 5790.

The neutral opening call comes thanks to a strong rebound from near 5-month lows after another leg down from the price of oil extending its declines to $28 in anticipation of an earlier return to market by Iran after sanctions were lifted this weekend. The bounce comes after a mixed Asian session, with only Chinese bourses higher, but regional losses less than Friday’s US 2% declines.

Note Japan’s Nikkei and the Australian ASX close to joining China in bear market territory (-20% from highs) as concerns grow over global economic strength in the face of a collapsing commodities space. Overnight, however, an improvement in Chinese property price growth buoyed sentiment along with state intervention to defend the Yuan against mounting bearish bets.

U.S. stocks fell sharply on Friday, capping another volatile week of trading as investors showed renewed concerns that lacklustre global growth (represented by plummeting Chinese stock markets and a tanking oil price) could prove contagious and start to infect the US economy. It’s debatable how much further US markets can or will fall, with one set of analysts arguing that the US is continuing to grow slowly but surely while more bearish commentators don’t think there’s been enough downside just yet, with more high volatility (if not all-out declines) likely.

Note bearish commodity bets doubling in just a week to their highest ever among money managers with oil at fresh 12yr lows and Copper at its lowest since 2009, fuelled by supply gluts, lower demand and a strong USD hindrance. Note comments last week from US banks revealing the painful knock-on from the commodity price declines with big jumps in bad loans to the energy sector.

In focus today (in what could be a welcome quiet session on account of the Martin Luther King day US holiday) with no major data scheduled will be the fallout from the Iranian sanctions lifting.

Oil’s woes were compounded over the weekend after Iranian sanctions were lifted, paving the way for fresh supply to enter the market – OPEC member Iran has the world’s fourth largest crude reserves. Both Brent and WTI now firmly in the $20s as hedge funds pile into short positions (panic phase?). Note WTI now trading above Brent taking the spread between the two back negative.

Gold is still benefiting from renewed oil-related uncertainty, still in a rising channel since early December. Off weekend highs this morning on profit taking, but it’ll be encouraging to see whether $1090 holds as support for further gains towards $1105 this week while the Dollar Basket struggles amid much debate about whether the Fed moved hiked too early.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Cobham says Simon Nicholls to join Wolseley as CFO

- Wolseley announces CEO and CFO succession

- Falkland Oil and Gas AIM – listed shares temporarily suspended pending announcement

- Christie sees FY revenue in line with market expectations

- Fastjet launches flights between Zimbabwe and Johannesburg

- Home Retail confirms Homebase sale to Wesfarmers

- Amec Foster Wheeler says CEO Brikho steps down

- JPMorgan Chase Declares Preferred Stock Dividend

- Union Jack Oil Commencement of Drilling Operations