Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

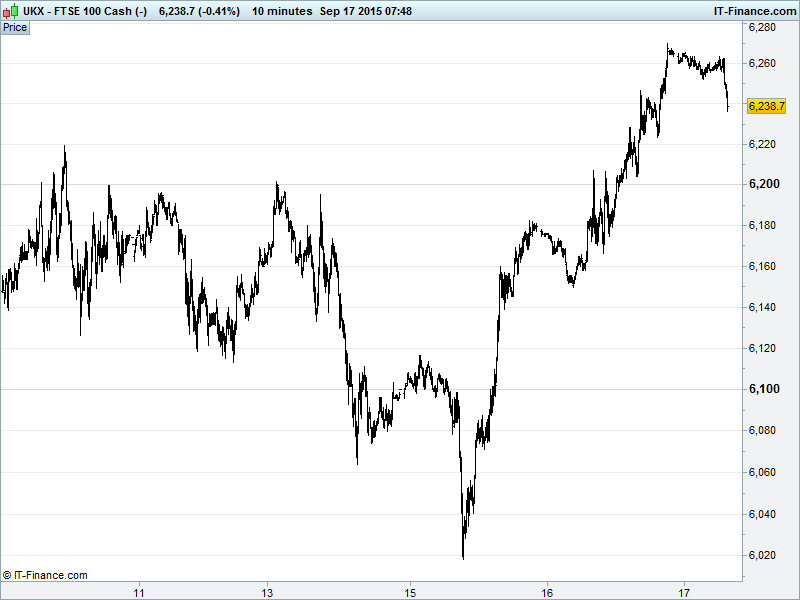

UK 100 Index called to open +5pts at 6235 having broken above 6200 yesterday, keeping the uptrend from Aug 25 lows intact. Currently testing 6250 resistance-turned-support having pulled back from 6270 overnight highs. The 6300 highs of last week remain in sight and a break above this level could allow for upside towards Aug highs 6600. Updated watch levels: Bullish 6275, Bearish 6220.

The positive opening call comes after another session of gains for both Asian and US equities despite investors being quite clear they haven’t the foggiest about which way the Fed FOMC committee will vote (Fed Fund Futures imply less than 25% chance of hike, Analysts/Economists polled are 50/50).

A Dovish hike (small rate rise then nothing more for a while) or reiterate its long-standing Hawkish Hold (not yet, but we’re closer)? Or could we be in store for a surprise (unlikely)? Plenty of factors for (Jobs, growth) and against (missing inflation, already strong USD, China, market volatility etc.)

As the clock ticks towards the ‘big’ announcement, we wonder whether deliverance of some much desired and long-awaited clarity (be it hike or hold) will in fact be the instigator of a relief rally with markets at least knowing what the next few months will hold (months being long-term in these new short-term focused markets). Have the gains of the last 2 days been a warm-up? Are markets equally confident in a pleasing Hold or low-impact hike?

Asian equities higher, helped by a higher oil price and yet more M&A deals (beverages, media) flowing through and boosting sentiment. Japan’s Nikkei rising on continued low volumes as traders await the Fed decision and despite another set of worse-than-expected trade data (5th in a row).

US bourses closed positive on Wednesday, posting a second straight session of solid gains as Some of the biggest names in the financial industry deemed a rate rise unwise – notably the market oracle that is Goldman Sachs, and even those whose firms would benefit from higher interest rates – in a stark reversal of sentiment to that expressed earlier in the year when a mid-2015 hike was widely expected. In similar vein to the invocation of Hitler in a desperate attempt to win back ground in a debate, doves hardly need to invoke the ‘great depression of 1937’ argument, but are doing so anyway.

In focus today will of course be the Fed this evening. However, data-wise we have UK Retail Sales at 9.30am expected to show slower growth in August backing up recent BDO data suggesting consumers making the most of strong GBP and weak EUR to reverse trend of staycations and resume foreign travel thus spending less in the shops while poor weather kept people away from the high street. Tourists also spending less due to weak EUR and poor weather kept.

In the afternoon, US Jobless Claims seen unchanged while Housing data shows more Permits but less Starts. The Philly Fed is seen giving up a little ground while the Fed FOMC policy announcement at 7pm and the press conference by Fed Chair Janet Yellen will draw a quite significant crowd given it could see the first US rate rise in almost a decade signalling crisis-end and return to growth.

Rallying Crude prices following some odd yet bullish EIA US stockpiles data (forecast +1.2m barrels, reported -2.1m), with Cushing, Oklahoma inventories alone down by 2m barrels, seen to bolster both US and UK energy stocks ahead of the European open. Brent ($50) and WTI ($47) both potentially forming day-long bearish reversal patterns (Brent double top, WTI head & shoulders) after oil traders engaged in a maniacal shopping spree yesterday afternoon.

Gold ($1121) flattened out overnight after rallying on Wednesday with some traders looking to avoid queueing up for ‘crowded’ risk-off positions elsewhere. Support regained at $1118 as the yellow metal awaits the Fed decision with baited breath. Expect a big sell-off tonight/tomorrow if the Fed pulls the plug, while arguably little price action if it doesn’t.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Kier raises FY dividend after profit rise

- Just Retirement posts 11% fall in 2014/15 pre-tax profit on higher expenses

- Phoenix Groups confirms in talks to buy rival Guardian Financial

- Premier Farnell says to sell industrial products unit, cuts dividend

- Crawshaw sees FY exceeding market expectations

- Rotork sees FY revenue between £530m-£555m

- Shell's Takeover of BG Faces Hurdle in Australia

- Merlin Entertainments Says Rollercoaster Crash Will Affect 2016 Profit