Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

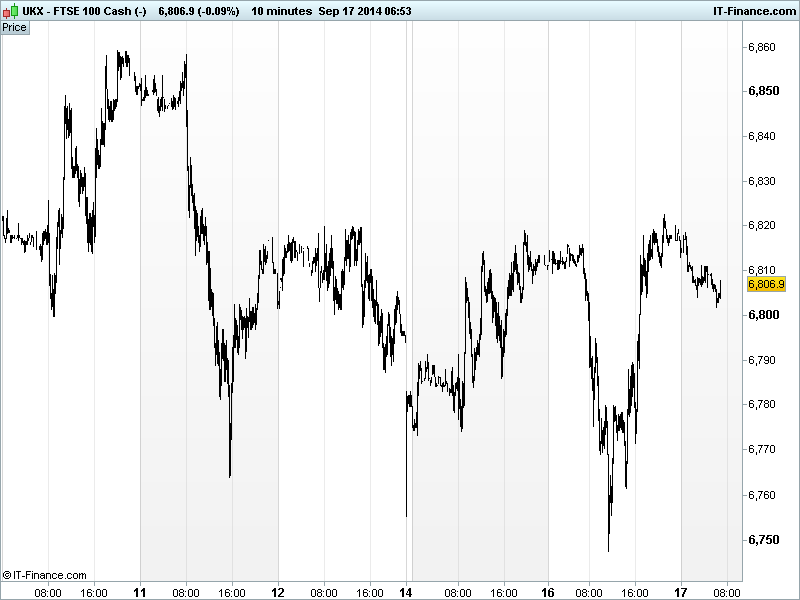

UK 100 called to open +15pts at 6810 having recovered from another test of recent lows in the 6750 zone engineered by some weak macro data and jitters ahead of key risk events later this week including this evening’s policy update from the US Fed FOMC, tomorrow’s ECB offering of TLTROs to banks to boost Eurozone growth and of course the Scottish referendum result on Friday morning.

US markets closed higher on improved risk sentiment based on talk that fears of a more hawkish Fed FOMC policy statement may have gone too far and the WSJ’s Fed watcher saying he expects no change to forward guidance. After weak data out of China, reports the PBOC is to offer $81bn of liquidity to China’s top five banks also boosted sentiment. This saw the DJIA make a new all-time intraday high.

Overnight Asian stocks are mixed on reports of China’s liquidity injection and a Moody’s report suggesting improved financial results for Chinese Property Developers in the second half of the year being offset by more weak China data with the MNI Business Indicator (5-month low).

There was also continued speculation over the Fed’s latest policy statement (Goldman Sachs says no major change) and a Die Welt report that the ECB are considering accepting asset-backed securities which are below the credit rating required for collateral for lending to banks to increase take-up and boost regional growth by staving off the threat of deflation

In focus today, we have UK Unemployment and Earnings seen improving a notch which could help GBP although it may depend on the latest minutes from the BoE which are released at the same time. Consensus expects a rebound in Eurozone Consumer Price Inflation which could boost the EUR.

In the US CPI is seen flat in August and falling below target on an annual basis which could reduce some of the hawkish fears related to the Fed update, although the US NAHB Housing index is seen creeping higher as a sign of consumer confidence. Then it’s all about the Fed statement in the evening and its update on economic projections and of course the press conference with the Chair Yellen.

The UK 100 remains in a September downtrend, with yesterday’s recovery from 6750 to 6823 unable to break the series of falling highs and lows. One positive from this week, however, was yesterday’s ability to test the highs of the prior day which could lead to a test of the September downtrend should sentiment get another boost from a nice dovish Fed statement this evening.

In the UK, those worried about a change to the union this week were appeased by news that the Scottish No-campaign was narrowly in the lead. Still too close to call, although Betfair did pay out yesterday based on any ‘no’ bets placed before 10am yesterday, based on its calculated “79% likelihood of a ‘no’ vote”.

In commodities, Gold is holding above 8-month lows of $1225/oz ahead of the Fed statement this evening with uncertainty boosting demand for the safehaven while US Light Crude is trading near a two-week high after OPEC’s secretary general said the group may cut crude-output targets next year.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- AU Westpac Leading Index Remained weak

- CN MNI Business Indicator Deteriorated

- EZ EU New Car Registrations Growth Slowed

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- IG Group revenue falls 9 percent in first quarter

- Chemring reports Q3 revenue of 77.5 mln stg vs 110.5 mln stg

- UK engineer Smiths Group full – year profit falls

- Petroceltic, Hess to resume oil drilling in Iraqi Kurdistan in October

- Dignity to return 54 mln stg to shareholders after debt cuts

- JD Sports lifts full-year outlook after record first half

- Imagination Tech sees progress in-line with expectations

- Daily Mail group confirms full-year guidance

- DS Smith sees performance in line with plans