Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

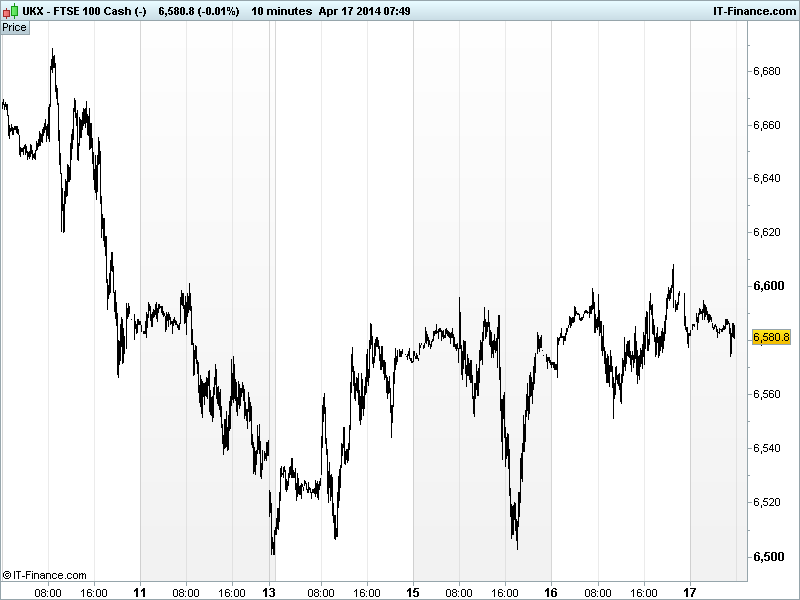

UK 100 called to open -5pts at 6585, having made a brief test of the eyed 6600 breakout level overnight as US markets made further gains (best 3-day rally for S&P in 2 months, back positive for 2014).

US progress was assisted by solid industrial production data, supportive/accomodative rhetoric from Fed Chair Yellen and colleague Fisher, a US Beige book suggesting economic activity increasing in most regions, labour conditions mixed-to-positive and internet name Yahoo!’s Q1 results beating estimates, thanks to surging sales at Chinese e-commerce giant Alibaba.

After the US close, however, several names suffered in after-hours trading with shares down on disappointing Q1 results. IBM was hurt by declining hardware sales, Google by declining advertising revenues. Another tough day for tech. Amex beat expectations, but shares down on more caution towards debt. Weaker Housing data earlier in the day also lingered in terms of US Consumer Confidence.

In Asia-Pacific overnight, equities still bid, although bourses only just edging higher. Data from Australia showed New Motor Vehicle Sales and Business confidence weakening. In Japan, Consumer confidence missed expectations and dropped back almost a point and a stronger JPY held equities back a bit.

In Ukraine, things get no better with the news of more deaths of pro-Russian separatists however, Ukrainian progress may have slowed and Washington does not anticipate a breakthrough with Russia in Geneva.

This morning, German PPI has delivered another blow to the ECB with a negative figure for March, highlighting the risk of dis-inflation, however, EU New car registrations have jumped over 10% in March, accelerating no February’s 8%.

In focus today, amid a light calendar to close the shortened Easter trading week, we have US Jobless Claims seen back up above 300K but continuing claims flat at 2.78m. The Philly Fed Business outlook is expected to nudge up from 9 to 10, although stateside data from earlier in the week highlights the risk of a deterioration.

Results are still in full flow and today it is the turn of Morgan Stanley and Goldman Sachs after Bank of America beat expectations yesterday. Other big names reporting include Honeywell, Baker Hughes, Dupont, Schlumberger, General Electric, Phillip Morris and Pepsico.

UK Results today include. Diageo (DGE.L) 9-month organic sales +0.3% vs. +2% expected, Q3 organic sales - 1.3% vs. +1.8% expected, weaker performance in Asia, currency volatility negatively impacting operations. Taylor Wimpey (TW..L) Strong Q1 with continuing improvement across all regions, order book volume +13% to 8,139 homes from last year, average selling price +22%, confident in delivering 200-300 basis points of operating margin in 2014. Mulberry (MUL.L) Warns that underlying profit for the year would be marginally below current expectations, the fourth in two years. Pretax profit now expected around £14m.

In commodities; Gold back below its $1300 hover point of the last 2 days, neither being driven by risk appetite nor safehaven seeking after the recent sell-off from $1330. Oil prices seen Brent climb to 6-week highs >$110/bl on the Ukraine crisis and potential supply disruption. US Light Crude trading up at $104/bl despite big US inventory builds yesterday.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- AU New Motor Vehicle Sales Deteriorated

- AU NAB Business Confidence Deteriorated

- JP Consumer Confidence Miss, deteriorated

- JP Nationwide Dept Store Sales Improved

- DE PPI Miss, deteriorated

See Live Macro calendar for all details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- United Utilities to submit new business plan after Ofwat feedback

- Taylor Wimpey says strong sales continue in first quarter

- Cobham sells remaining non-core business

- Mulberry to lower prices after new profit warning

- Providence Resources to start seismic survey on Irish site

- Gemfields secures $15 mln working capital facility

- Skyepharma says receives 82 acceptances on open offer

- Shell finds gas in new area offshore Malaysia

- Lloyds Bank says investors swap bonds for $98 million

- Diageo third-quarter sales fall on Asian weakness