Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

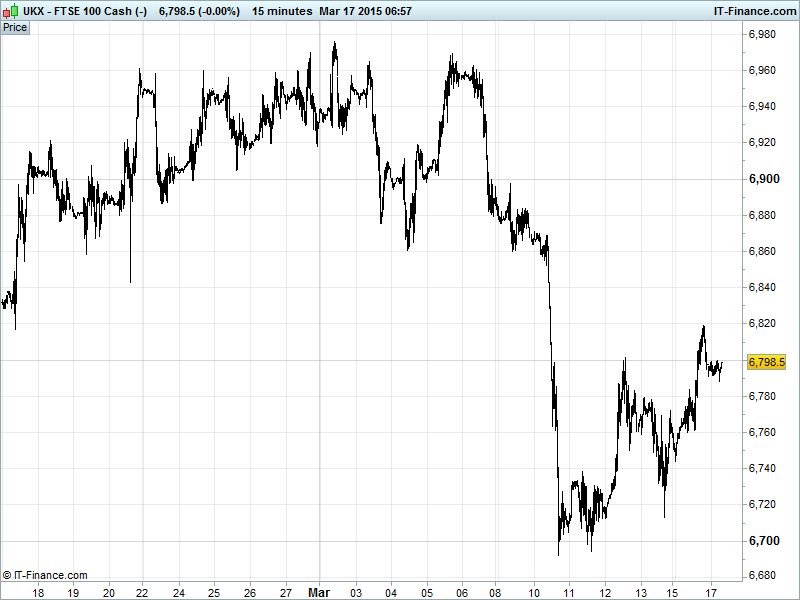

UK 100 called to open +6pts at 6802, still grinding higher after last week’s losses ad settling into an upwards channel resembling that through February and helped by mining stocks after Chinese economic stimulus plans emerged yesterday. Currently trading around yesterday’s resistance level 6800 which could become support today upon a decisive break upwards. Bulls looking towards 6850 while bears eyeing a drop back towards 6692 support.

The mildly positive open comes after mining and retail stocks took the index higher yesterday. The former benefitting from the news that China, a large market for commodities, is likely to implement economic stimulus measures to facilitate an economic recovery if need be. Closer to home, the DAX hit a new record high and the CAC was near a seven year peak while the ECB made €9.75B worth of bond purchases last week, below the suggested €15B average indicated by many analysts. President Mario Draghi spoke and said indicators suggest a sustained recovery is taking hold, adding that a lower oil price, ECB stimulus and structural reforms are all helping the economy. Elsewhere, the EU’s Juncker said options remain on the table to make Greece’s debt obligations more bearable. All this seeming amiable stuff to investors.

US bourses closed higher yesterday with a pullback in the strength of the USD, which is giving back ground following a recent surge whose effects were felt worldwide. US Treasury Secretary Lew said the US would be ready to extend sanctions on Russia if it fails to comply with the terms of ceasefire agreements with Ukraine.

The US Fed's 2-day meeting starts Today, with many expecting dovish chatter – indications of which are more likely to be a lack of certain words rather than inclusion of them. If you’re not familiar with the word, remain patient. You may still hear it mentioned given surprisingly disappointing US economic data yesterday.

Asian markets are doing well with Chinese stocks hitting a seven year high after reassurances yesterday that the government are virtually guaranteeing an economic recovery, giving many commodity prices a boost (except for oil…) and much of the same to equities. The Nikkei hit its highest level in 15 years, again, as the BoJ pledged to continue super-QE (Abenomics) until stable 2% inflation was maintained, keeping an eye on risk and adjusting policy as appropriate. Australian consumer confidence was up despite less than impressive recent data, with the RBA deciding to defer a decision on rates – looking towards a cut in April if at all.

In focus today are Eurozone CPI and Zew Surveys with US Housing data later on, all showing mixed expectations.

US light crude ($43.7) hovered around its lowest level since March 2009 amid continued forecasts of a supply glut, with the USD strength also weighing in on the price. Analysts expect a rise of over 4 million barrels in US crude oil inventories for the week ending 13 March, which would be a 10th weekly increase in a row. All eyes will be on the IEA report on Wednesday. Meanwhile, Brent ($54.8) edged up a little overnight from March lows of $54.7.

Gold ($1154) still trading sideways in a $5 range this morning having declined a little overnight. Investors are waiting for the Fed meeting to give them direction – a strong dollar is pushing down demand from foreign safe haven investors, those in Europe preferring low yield bonds in the current climate. A Fed decision to delay a US rate hike could up demand on the back of a weaker dollar, but this remains to be suggested.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan Leading Index, Coincident Index Improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Sainsbury's sales dip for fifth straight quarter

- Kier secures place on 2 bln stg framework, wins 130 mln worth of new contracts

- Gem Diamonds full – year revenue rises 27 pct

- IG Group Q3 revenue down 5.1 pct due to Swiss franc movements

- Bowleven completes Etinde farm-out transaction, gets initial proceeds of $165 mln

- Just Eat confident on year ahead, sees revenue above 200 mln stg

- French Connection posts smaller full-year loss

- Onesavings Bank FY underlying pretax profit more than doubles

- Antofagasta says protests, ruling cast doubt over Pelambres future